Academic Profile

Statistics

Similar Authors

Papers on arXiv

Stationary and ergodic time series can be constructed using an s-vine decomposition based on sets of bivariate copula functions. The extension of such processes to infinite copula sequences is consi...

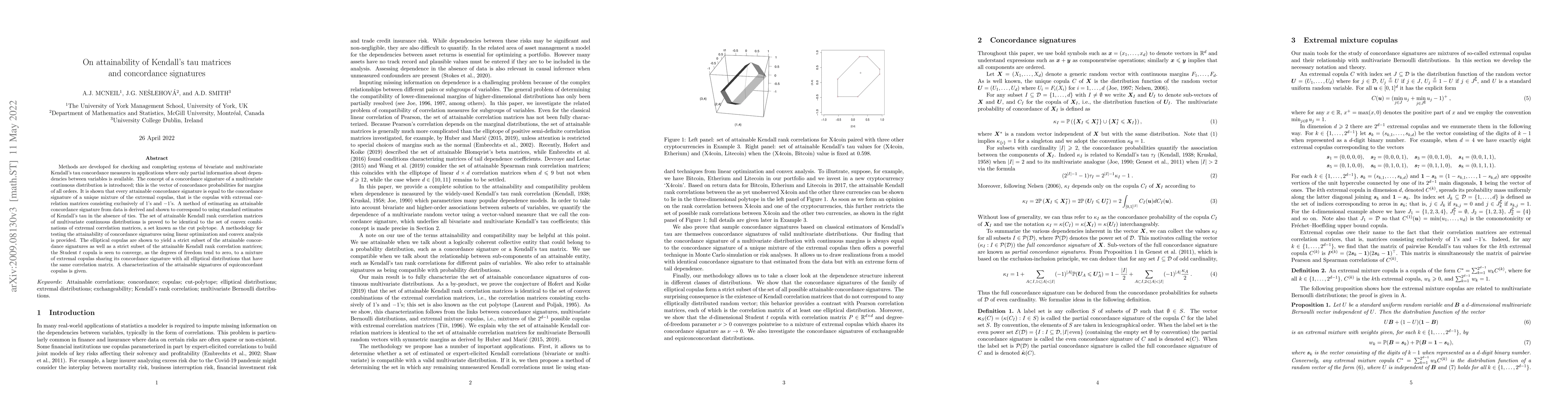

Methods are developed for checking and completing systems of bivariate and multivariate Kendall's tau concordance measures in applications where only partial information about dependencies between v...

An approach to modelling volatile financial return series using stationary d-vine copula processes combined with Lebesgue-measure-preserving transformations known as v-transforms is proposed. By dev...

An approach to the modelling of volatile time series using a class of uniformity-preserving transforms for uniform random variables is proposed. V-transforms describe the relationship between quanti...

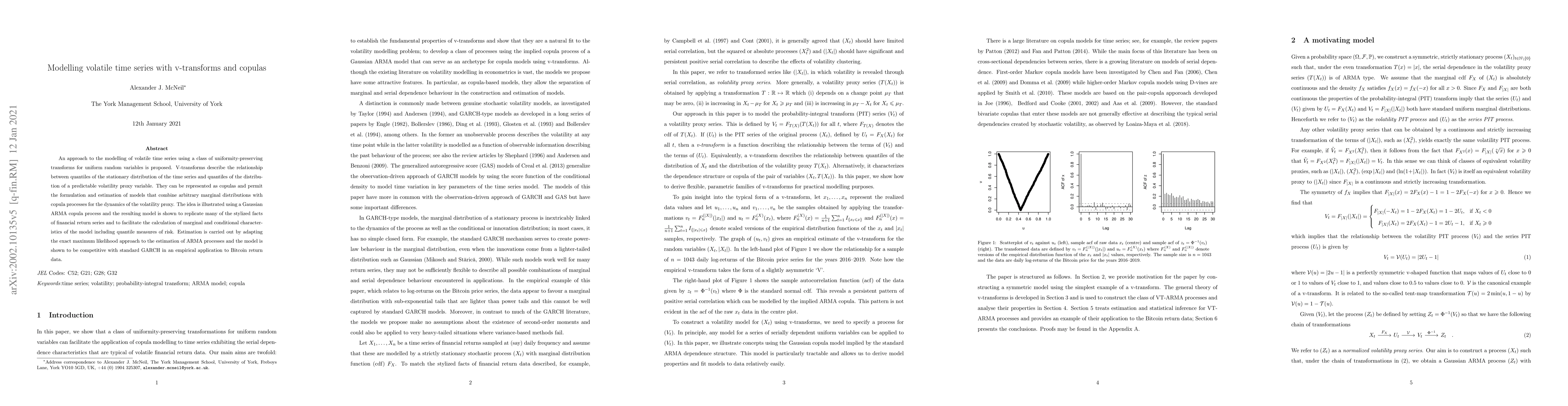

The bivariate copulas that describe the dependencies and partial dependencies of lagged variables in strictly stationary, first-order GARCH-type processes are investigated. It is shown that the copula...

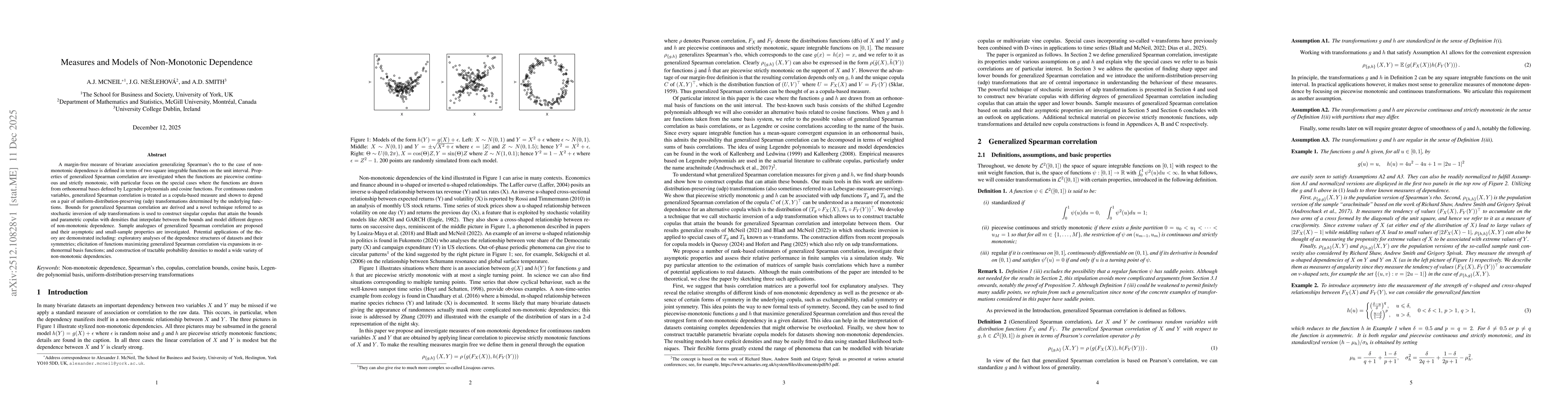

A margin-free measure of bivariate association generalizing Spearman's rho to the case of non-monotonic dependence is defined in terms of two square integrable functions on the unit interval. Properti...