Authors

Summary

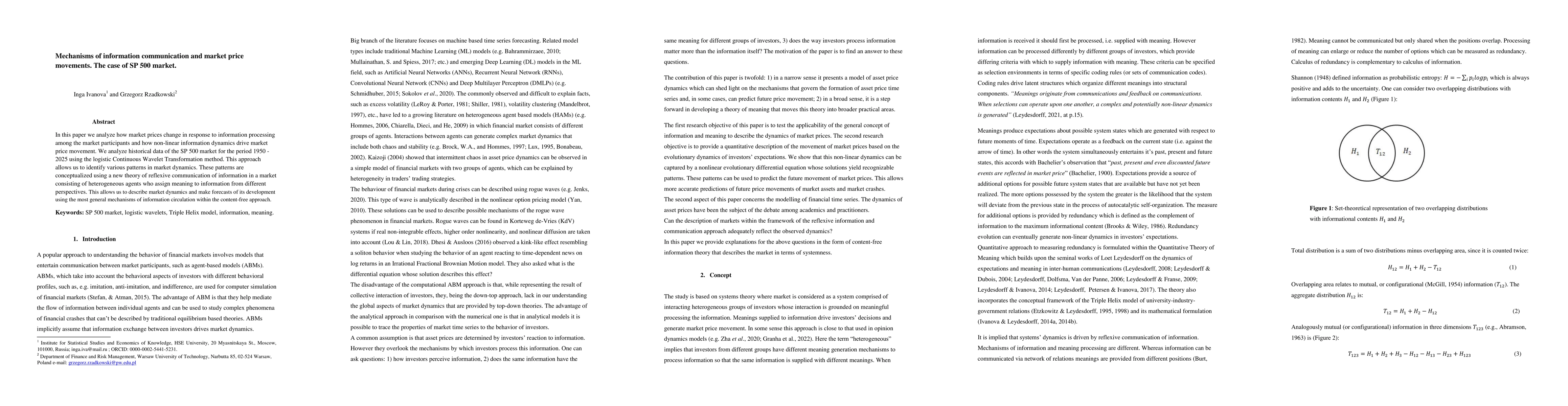

In this paper we analyze how market prices change in response to information processing among the market participants and how non-linear information dynamics drive market price movement. We analyze historical data of the SP 500 market for the period 1950 -2025 using the logistic Continuous Wavelet Transformation method. This approach allows us to identify various patterns in market dynamics. These patterns are conceptualized using a new theory of reflexive communication of information in a market consisting of heterogeneous agents who assign meaning to information from different perspectives. This allows us to describe market dynamics and make forecasts of its development using the most general mechanisms of information circulation within the content-free approach.

AI Key Findings

Generated Jun 08, 2025

Methodology

The research employs the logistic Continuous Wavelet Transformation method to analyze historical SP 500 market data from 1950 to 2025, identifying patterns in market dynamics through a reflexive communication of information theory among heterogeneous agents.

Key Results

- Market price changes are shown to be driven by non-linear information dynamics.

- Various patterns in market dynamics are identified using the logistic Continuous Wavelet Transformation method.

- A new theory of reflexive communication of information in markets is conceptualized.

Significance

This research is important as it contributes to understanding market price movements and provides a framework for forecasting market development based on information circulation mechanisms.

Technical Contribution

The application of the logistic Continuous Wavelet Transformation method to historical SP 500 data for identifying patterns in market dynamics and proposing a new theory of reflexive information communication.

Novelty

This work introduces a novel theory of reflexive information communication in markets and demonstrates its application using the logistic Continuous Wavelet Transformation method, providing a unique approach to understanding market price movements.

Limitations

- The study is limited to the SP 500 market, so findings may not generalize to other markets.

- Reliance on historical data may not fully capture future market complexities.

Future Work

- Further research could apply the proposed theory to other financial markets for validation.

- Investigating the impact of real-time data and high-frequency trading on market dynamics.

Paper Details

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersNo citations found for this paper.

Comments (0)