01

MethodologyHow they did it

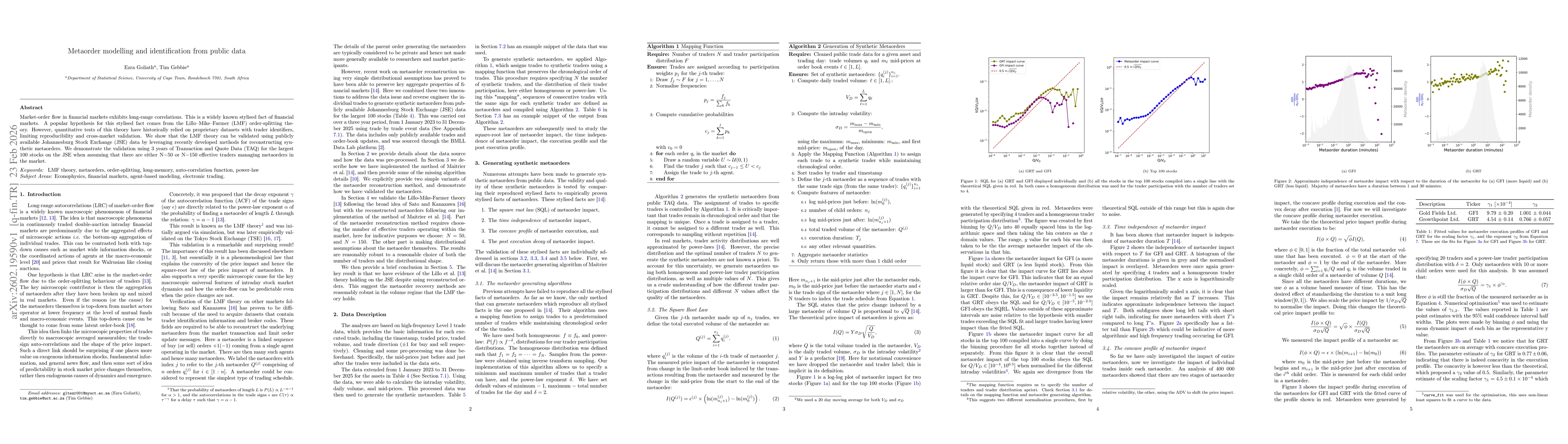

Synthetic metaorders were generated from public Johannesburg Stock Exchange TAQ data using the reconstruction algorithms of Maitrier et al., assuming a specified number of effective traders and a trader‑participation distribution; the resulting metaorders were then used to test the Lillo‑Mike‑Farmer (LMF) theory.

Discussion 0