Academic Profile

Statistics

Similar Authors

Papers on arXiv

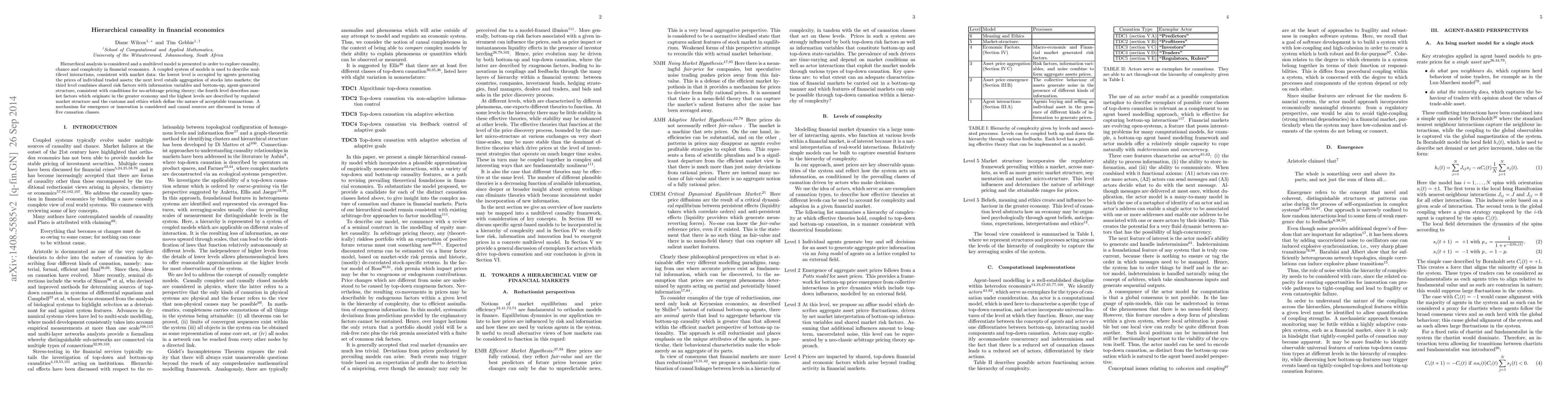

Hierarchical analysis is considered and a multilevel model is presented in order to explore causality, chance and complexity in financial economics. A coupled system of models is used to describe mu...

The clarion call for causal reduction in the study of capital markets is intensifying. However, in self-referencing and open systems such as capital markets, the idea of unidirectional causation (if...

We extend a Discrete Time Random Walk (DTRW) numerical scheme to simulate the anomalous diffusion of financial market orders in a simulated order book. Here using random walks with Sibuya waiting ti...

Blackjack or "21" is a popular card-based game of chance and skill. The objective of the game is to win by obtaining a hand total higher than the dealer's without exceeding 21. The ideal blackjack s...

We consider the dynamics and the interactions of multiple reinforcement learning optimal execution trading agents interacting with a reactive Agent-Based Model (ABM) of a financial market in event t...

We consider the learning dynamics of a single reinforcement learning optimal execution trading agent when it interacts with an event driven agent-based financial market model. Trading takes place as...

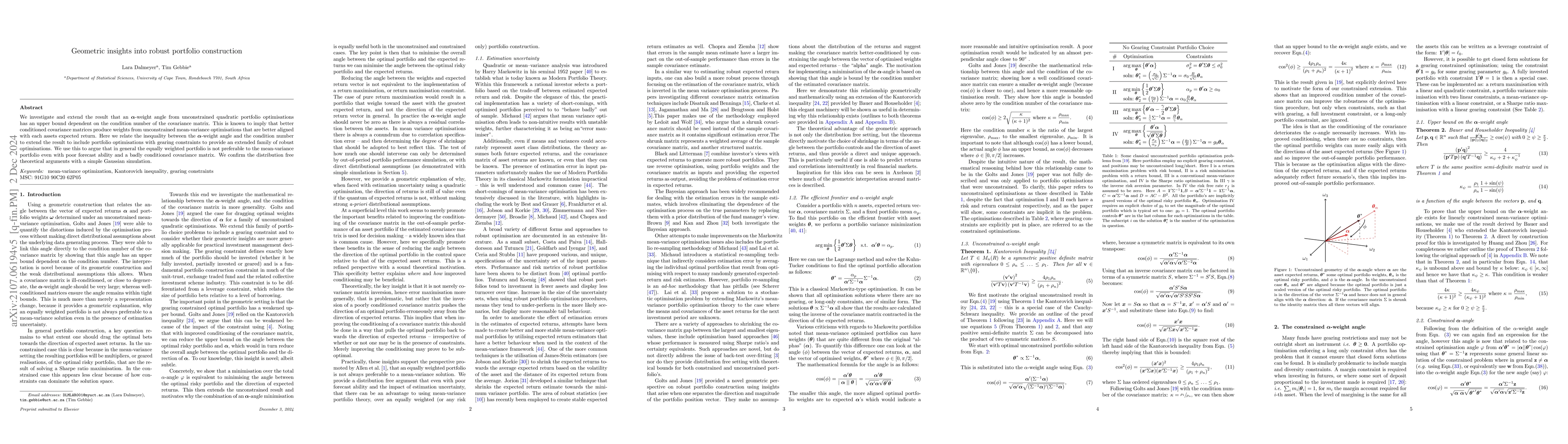

We investigate and extend the results of Golts and Jones (2009) that an $\alpha$-weight angle resulting from unconstrained quadratic portfolio optimisations has an upper bound dependent on the condi...

Mean-variance portfolio decisions that combine prediction and optimisation have been shown to have poor empirical performance. Here, we consider the performance of various shrinkage methods by their...

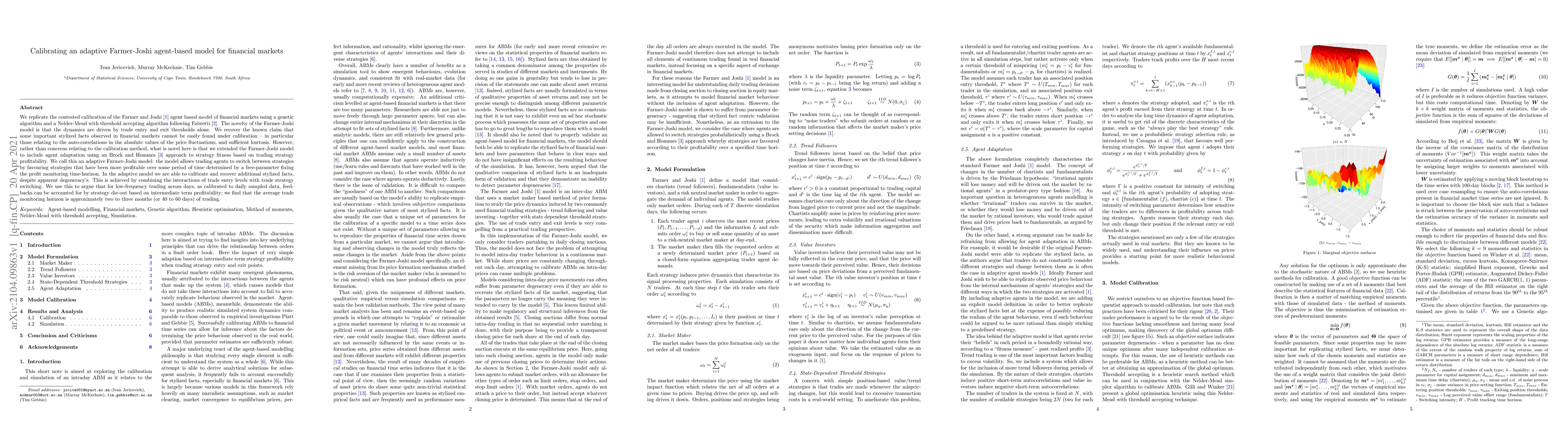

We replicate the contested calibration of the Farmer and Joshi agent based model of financial markets using a genetic algorithm and a Nelder-Mead with threshold accepting algorithm following Fabrett...

We deploy and demonstrate the CoinTossX low-latency, high-throughput, open-source matching engine with orders sent using the Julia and Python languages. We show how this can be deployed for small-sc...

Time and the choice of measurement time scales is fundamental to how we choose to represent information and data in finance. This choice implies both the units and the aggregation scales for the res...

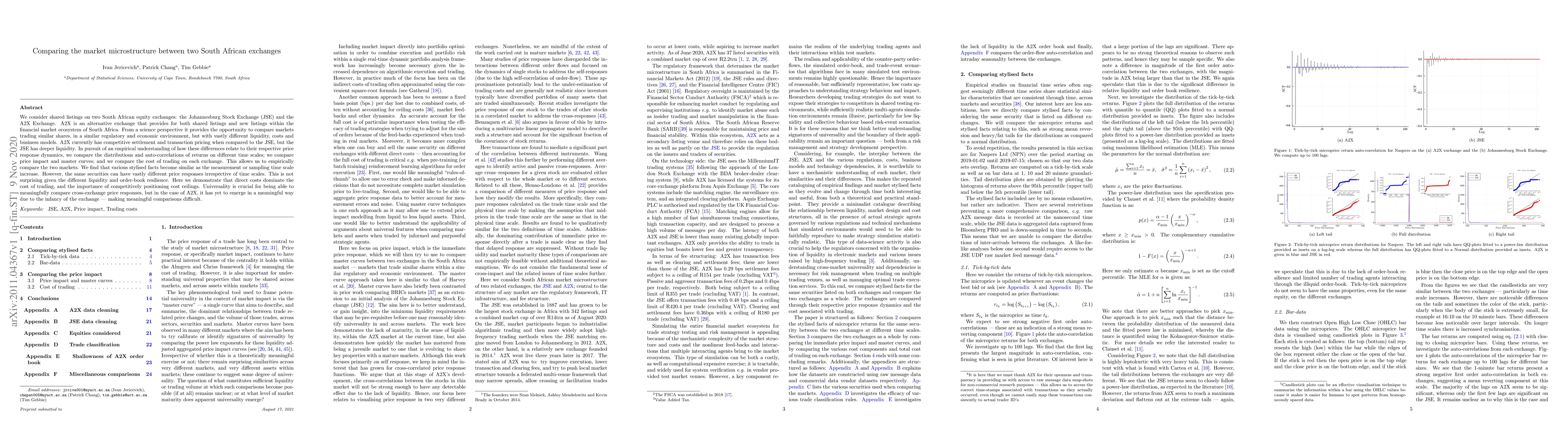

We consider shared listings on two South African equity exchanges: the Johannesburg Stock Exchange (JSE) and the A2X Exchange. A2X is an alternative exchange that provides for both shared listings a...

We consider the viability of a modularised mechanistic online machine learning framework to learn signals in low-frequency financial time series data. The framework is proved on daily sampled closin...

The artificial segmentation of an investment management process into a workflow with silos of offline human operators can restrict silos from collectively and adaptively pursuing a unified optimal i...

We revisit and demonstrate the Epps effect using two well-known non-parametric covariance estimators; the Malliavin and Mancino (MM), and Hayashi and Yoshida (HY) estimators. We show the existence o...

We implement a systematic asset allocation model using the Historical Simulation with Flexible Probabilities (HS-FP) framework developed by Meucci. The HS-FP framework is a flexible non-parametric e...

We consider the problem of fast time-series data clustering. Building on previous work modeling the correlation-based Hamiltonian of spin variables we present an updated fast non-expensive Agglomera...

We use an adversarial expert based online learning algorithm to learn the optimal parameters required to maximise wealth trading zero-cost portfolio strategies. The learning algorithm is used to det...

We map stock market interactions to spin models to recover their hierarchical structure using a simulated annealing based Super-Paramagnetic Clustering (SPC) algorithm. This is directly compared to ...

We consider financial market regime detection from the perspective of deep representation learning of the causal information geometry underpinning traded asset systems using a hierarchical correlation...

We use random walks to simulate the fluid limit of two coupled diffusive limit order books to model correlation emergence. The model implements the arrival, cancellation and diffusion of orders couple...

Backtests on historical data are the basis for practical evaluations of portfolio selection rules, but their reliability is often limited by reliance on a single sample path. This can lead to high est...

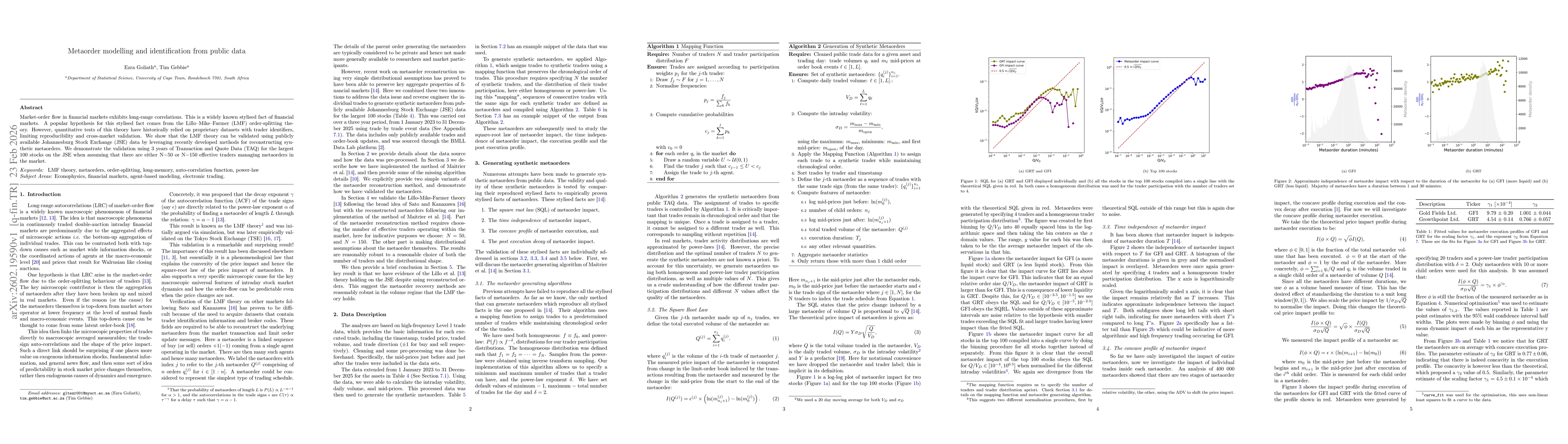

Market-order flow in financial markets exhibits long-range correlations. This is a widely known stylised fact of financial markets. A popular hypothesis for this stylised fact comes from the Lillo-Mik...

Financial markets are often modelled as if time were unique and continuous across assets and markets. Financial markets are however asynchronous, order flow is event-driven, and waiting times between ...

It is well known that LLM guardrails and trained persona dynamics can produce a reality gap: the distance between the world a LLM is permitted or shaped to describe, and the world in which users must ...

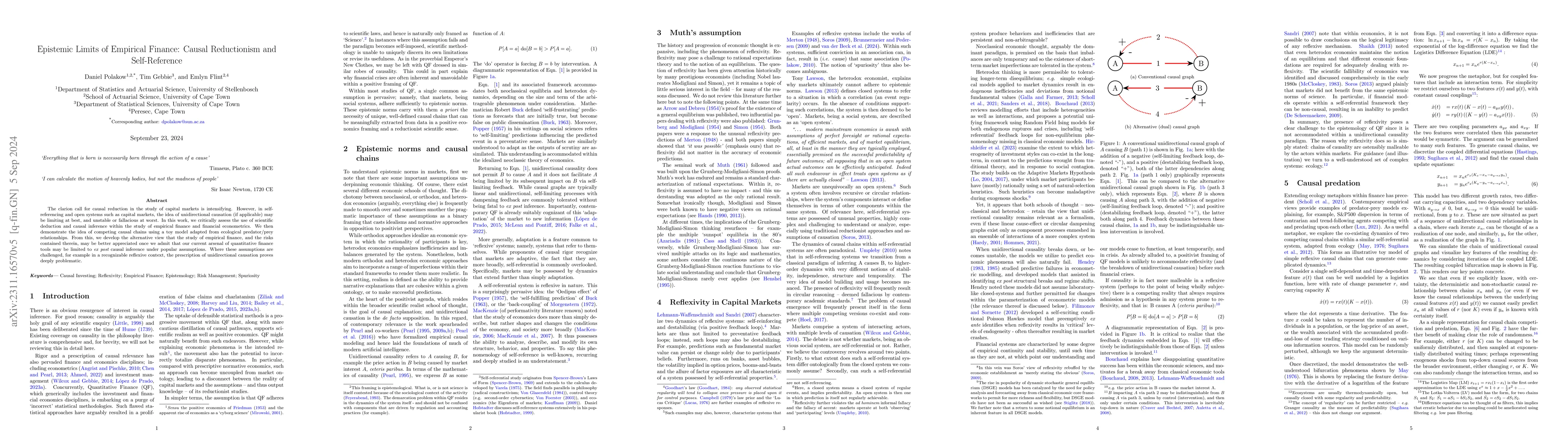

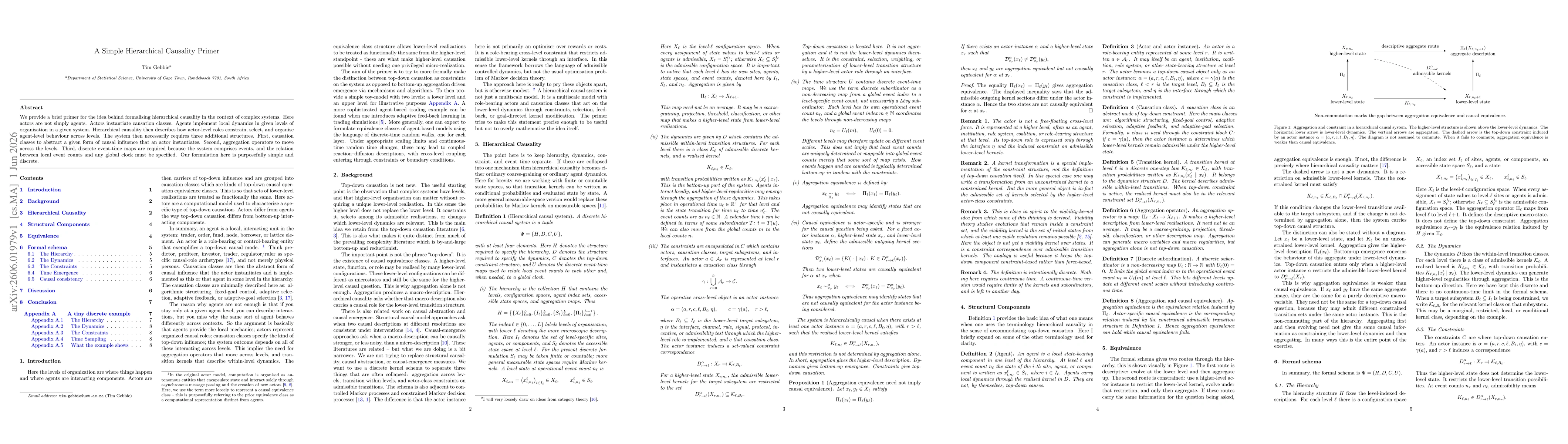

We provide a brief primer for the idea behind formalising hierarchical causality in the context of complex systems. Here actors are not simply agents. Actors instantiate causation classes. Agents impl...

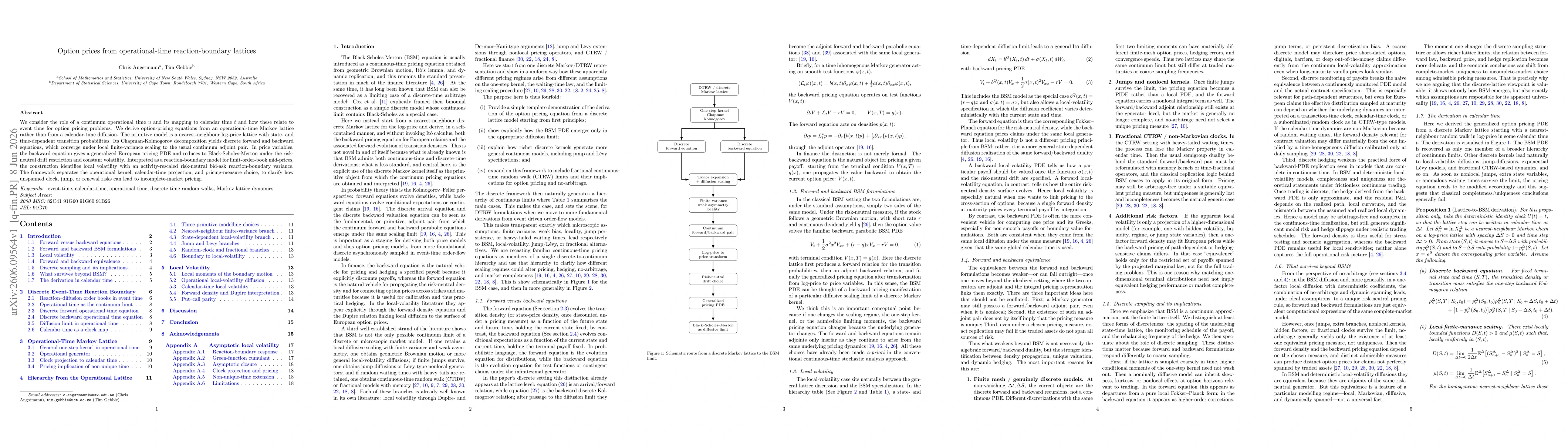

We consider the role of a continuum operational time u and its mapping to calendar time t and how these relate to event time for option pricing problems. We derive option-pricing equations from an ope...

We give a unified analytic account of correlation emergence and the Epps effect in two coupled limit order books. The model starts from a discrete random-walk description of order flow with creation, ...

Starting with a coupled discrete reaction--diffusion formulation for the lit and latent order books with non-uniformly sampled event times and meta-order source terms we show how two familiar market-m...

We derive an operational-time variance kernel for a latent-order-book reaction boundary and use it to separate three objects usually collapsed in calendar-time volatility models: a structural boundary...

We propose a Gabor--Epps uncertainty principle for practical trading. The key idea is that high-frequency correlation is not observed in clock time alone, but is resolved through market activity, orde...