Summary

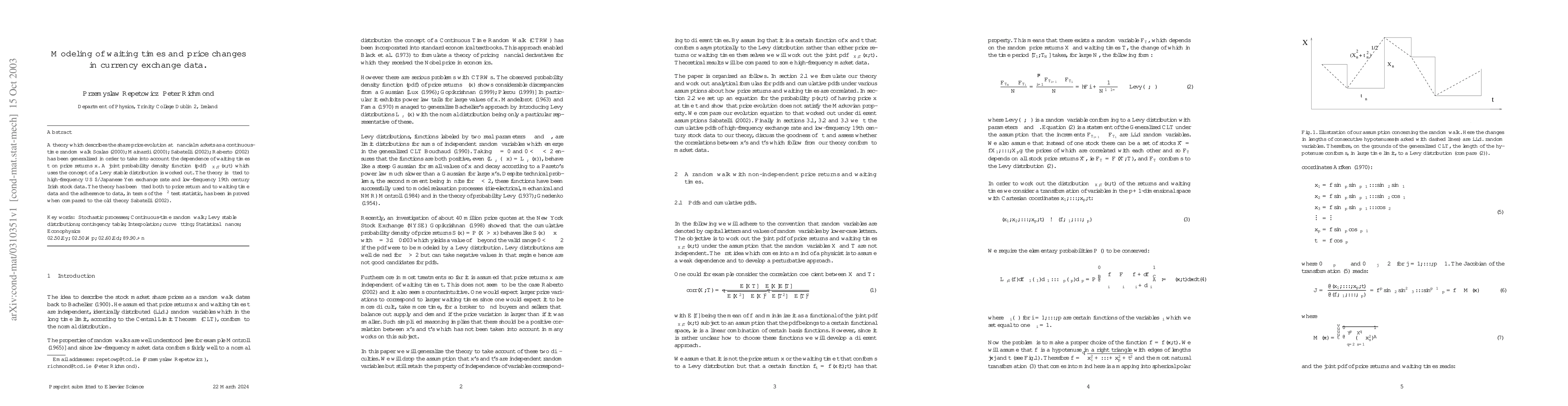

A theory which describes the share price evolution at financial markets as a continuous-time random walk has been generalized in order to take into account the dependence of waiting times t on price returns x. A joint probability density function (pdf) which uses the concept of a L\'{e}vy stable distribution is worked out. The theory is fitted to high-frequency US$/Japanese Yen exchange rate and low-frequency 19th century Irish stock data. The theory has been fitted both to price return and to waiting time data and the adherence to data, in terms of the chi-squared test statistic, has been improved when compared to the old theory.

AI Key Findings

Generated Sep 06, 2025

Methodology

A theory describing share price evolution as a continuous-time random walk was generalized to account for dependence of waiting times on price returns.

Key Results

- The joint probability density function uses the concept of L\'{e}vy stable distribution.

- The theory is fitted to high-frequency US$/Japanese Yen exchange rate and low-frequency 19th century Irish stock data.

- Adherence to data improves when compared to the old theory in terms of the chi-squared test statistic.

Significance

This research is important as it provides a new understanding of waiting times and price changes in currency exchange data.

Technical Contribution

The development of a joint probability density function using L\'{e}vy stable distribution.

Novelty

The study generalizes the theory to account for dependence of waiting times on price returns, providing a new understanding of currency exchange data.

Limitations

- The study only uses two datasets: high-frequency US$/Japanese Yen exchange rate and low-frequency 19th century Irish stock data.

- The theory may not be applicable to all types of financial markets or data.

Future Work

- Applying the theory to other types of financial markets or data

- Investigating the relationship between waiting times and price changes in different asset classes

Paper Details

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

| Title | Authors | Year | Actions |

|---|

Comments (0)