Authors

Summary

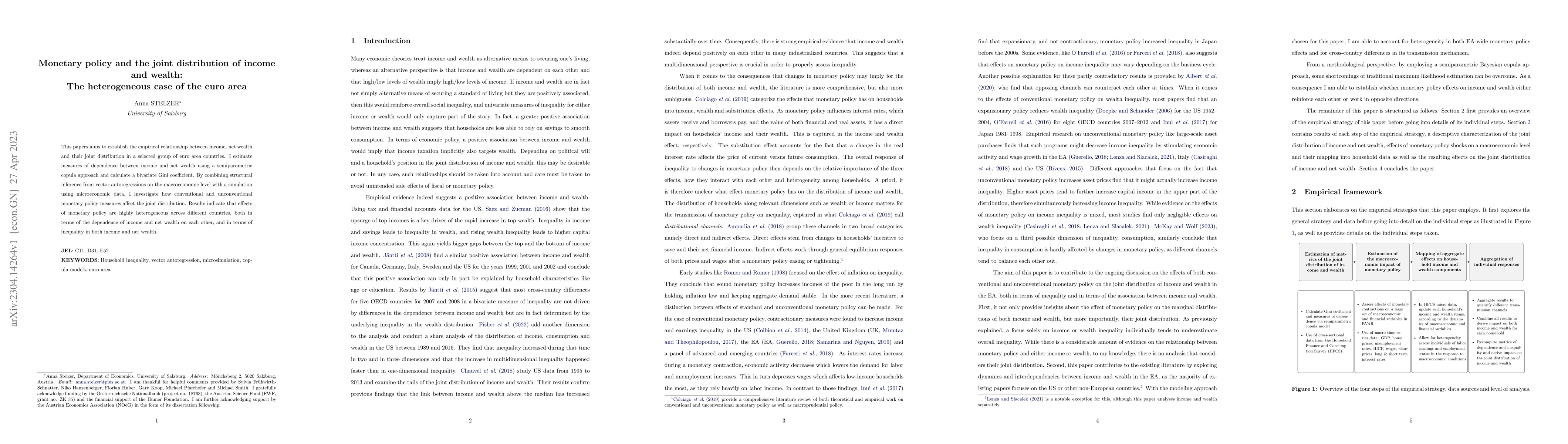

This papers aims to establish the empirical relationship between income, net wealth and their joint distribution in a selected group of euro area countries. I estimate measures of dependence between income and net wealth using a semiparametric copula approach and calculate a bivariate Gini coefficient. By combining structural inference from vector autoregressions on the macroeconomic level with a simulation using microeconomic data, I investigate how conventional and unconventional monetary policy measures affect the joint distribution. Results indicate that effects of monetary policy are highly heterogeneous across different countries, both in terms of the dependence of income and net wealth on each other, and in terms of inequality in both income and net wealth.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersThe Transmission of Monetary Policy via Common Cycles in the Euro Area

Jan Prüser, Lukas Berend

Large datasets for the Euro Area and its member countries and the dynamic effects of the common monetary policy

Matteo Barigozzi, Claudio Lissona, Lorenzo Tonni

No citations found for this paper.

Comments (0)