Financial derivative pricing is a significant challenge in finance, involving

the valuation of instruments like options based on underlying assets. While

some cases have simple solutions, many require complex classical computational

methods like Monte Carlo simulations and numerical techniques. However, as

derivative complexities increase, these methods face limitations in

computational power. Cases involving Non-Vanilla Basket pricing, American

Options, and derivative portfolio risk analysis need extensive computations in

higher-dimensional spaces, posing challenges for classical computers.

Quantum computing presents a promising avenue by harnessing quantum

superposition and entanglement, allowing the handling of high-dimensional

spaces effectively. In this paper, we introduce a self-contained and

all-encompassing quantum algorithm that operates without reliance on oracles or

presumptions. More specifically, we develop an effective stochastic method for

simulating exponentially many potential asset paths in quantum parallel,

leading to a highly accurate final distribution of stock prices. Furthermore,

we demonstrate how this algorithm can be extended to price more complex options

and analyze risk within derivative portfolios.

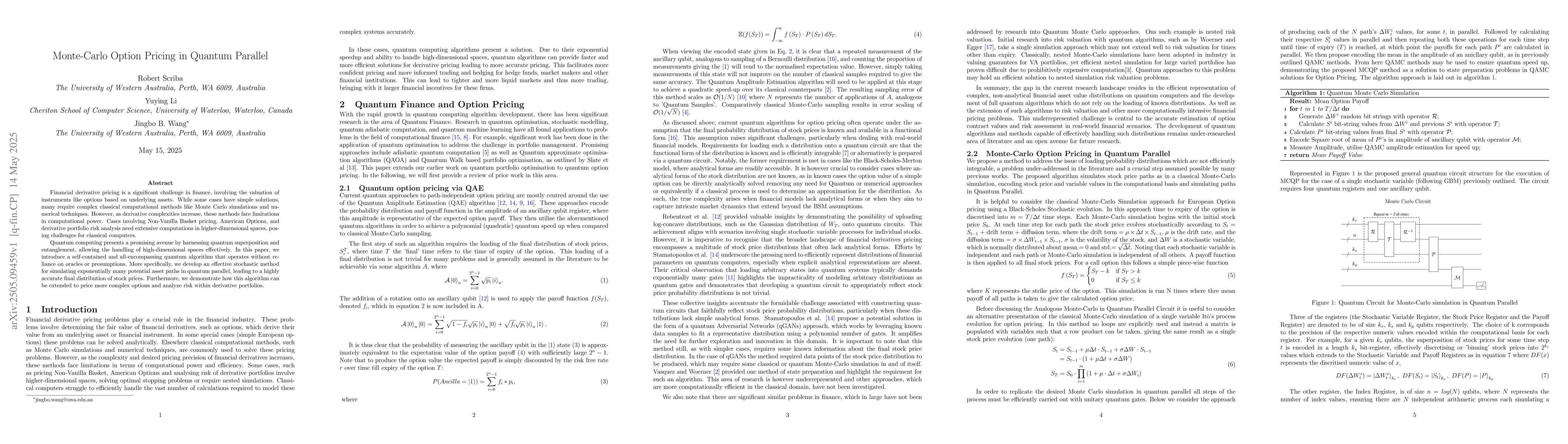

Discussion 0