Mortality and Healthcare: a Stochastic Control Analysis under Epstein-Zin Preferences

Publication

Metrics

AI Quick Summary

This paper develops a stochastic control model under Epstein-Zin preferences to optimize consumption, investment, and healthcare spending, showing how healthcare can reduce mortality growth. The model's unique utility formulation on a controllable random horizon leads to a new comparison result for utility value processes, and it closely matches real mortality data in the US and UK.

Paper Preview

Abstract

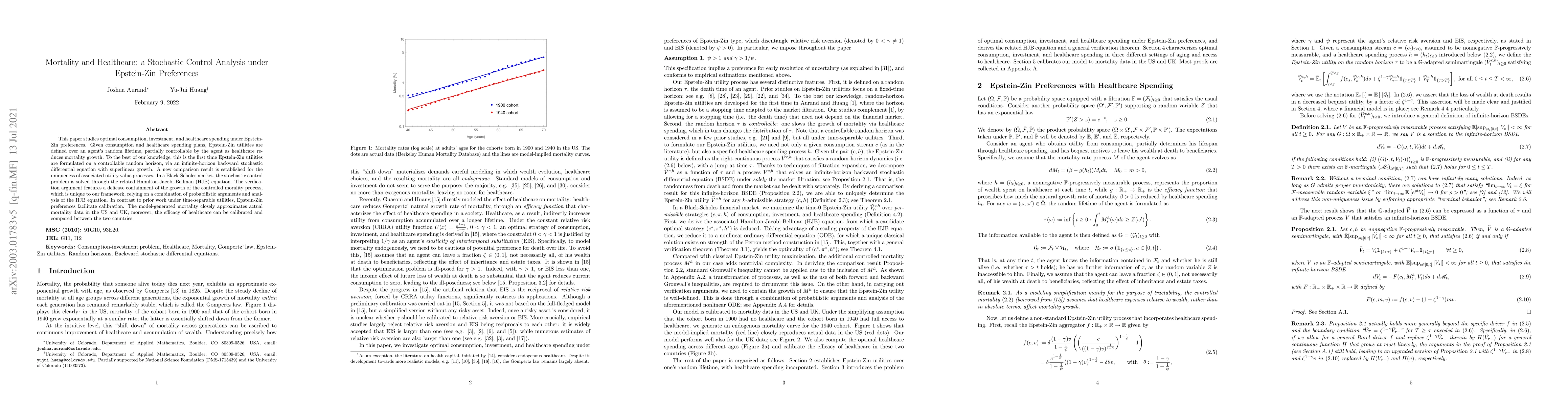

This paper studies optimal consumption, investment, and healthcare spending under Epstein-Zin preferences. Given consumption and healthcare spending plans, Epstein-Zin utilities are defined over an agent's random lifetime, partially controllable by the agent as healthcare reduces mortality growth. To the best of our knowledge, this is the first time Epstein-Zin utilities are formulated on a controllable random horizon, via an infinite-horizon backward stochastic differential equation with superlinear growth. A new comparison result is established for the uniqueness of associated utility value processes. In a Black-Scholes market, the stochastic control problem is solved through the related Hamilton-Jacobi-Bellman (HJB) equation. The verification argument features a delicate containment of the growth of the controlled morality process, which is unique to our framework, relying on a combination of probabilistic arguments and analysis of the HJB equation. In contrast to prior work under time-separable utilities, Epstein-Zin preferences facilitate calibration. The model-generated mortality closely approximates actual mortality data in the US and UK; moreover, the efficacy of healthcare can be calibrated and compared between the two countries.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0