Publication

Metrics

AI Quick Summary

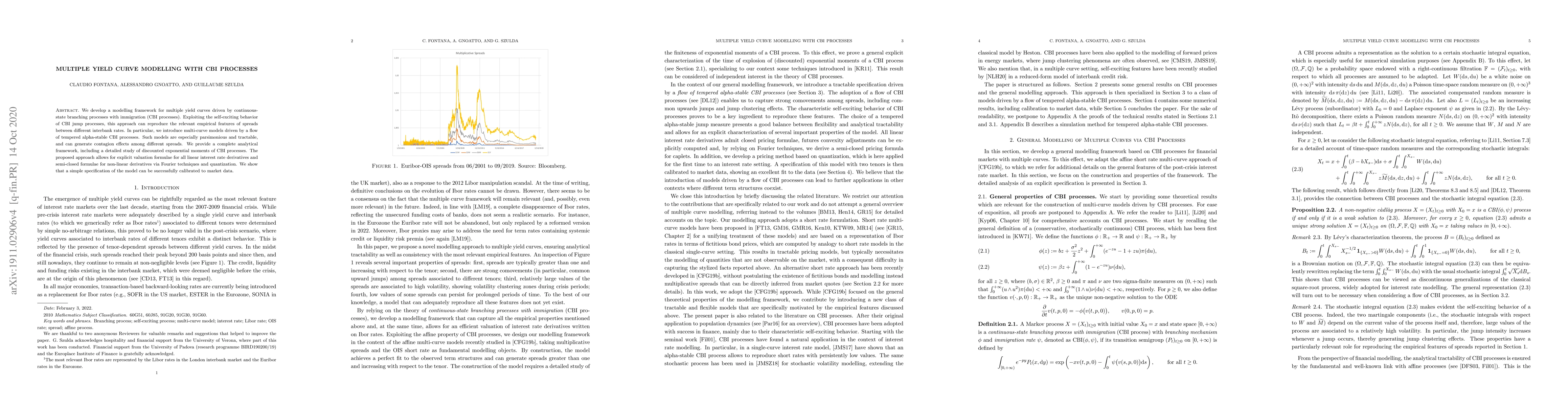

This paper develops a modelling framework for multiple yield curves using continuous-state branching processes with immigration (CBI processes), capturing empirical features of interbank rates and generating contagion effects. The analytical framework includes valuation formulae for linear and non-linear interest rate derivatives, and the model is successfully calibrated to market data.

Paper Preview

Abstract

We develop a modelling framework for multiple yield curves driven by continuous-state branching processes with immigration (CBI processes). Exploiting the self-exciting behavior of CBI jump processes, this approach can reproduce the relevant empirical features of spreads between different interbank rates. In particular, we introduce multi-curve models driven by a flow of tempered alpha-stable CBI processes. Such models are especially parsimonious and tractable, and can generate contagion effects among different spreads. We provide a complete analytical framework, including a detailed study of discounted exponential moments of CBI processes. The proposed approach allows for explicit valuation formulae for all linear interest rate derivatives and semi-closed formulae for non-linear derivatives via Fourier techniques and quantization. We show that a simple specification of the model can be successfully calibrated to market data.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0