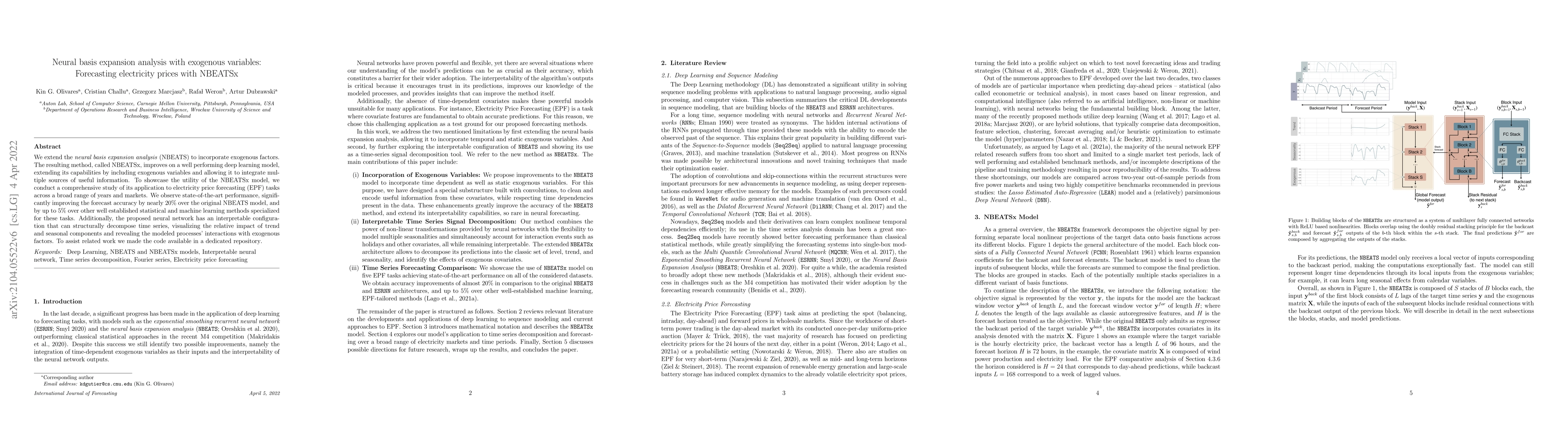

Neural basis expansion analysis with exogenous variables: Forecasting electricity prices with NBEATSx

Publication

Metrics

AI Quick Summary

This paper extends the NBEATS model to NBEATSx by incorporating exogenous variables, achieving state-of-the-art electricity price forecasting accuracy, improving upon both the original NBEATS and other established methods by nearly 20% and up to 5% respectively. The model's interpretable structure allows for visualization of time series components and their interactions with external factors.

Paper Preview

Abstract

We extend the neural basis expansion analysis (NBEATS) to incorporate exogenous factors. The resulting method, called NBEATSx, improves on a well performing deep learning model, extending its capabilities by including exogenous variables and allowing it to integrate multiple sources of useful information. To showcase the utility of the NBEATSx model, we conduct a comprehensive study of its application to electricity price forecasting (EPF) tasks across a broad range of years and markets. We observe state-of-the-art performance, significantly improving the forecast accuracy by nearly 20% over the original NBEATS model, and by up to 5% over other well established statistical and machine learning methods specialized for these tasks. Additionally, the proposed neural network has an interpretable configuration that can structurally decompose time series, visualizing the relative impact of trend and seasonal components and revealing the modeled processes' interactions with exogenous factors. To assist related work we made the code available in https://github.com/cchallu/nbeatsx.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0