Neuroevolution Neural Architecture Search for Evolving RNNs in Stock Return Prediction and Portfolio Trading

Publication

Metrics

AI Quick Summary

This paper proposes using neuroevolution to evolve recurrent neural networks (RNNs) for stock return predictions, employing the EXAMM algorithm. The evolved RNNs outperform traditional indices in portfolio trading based on daily long-short strategies, showing higher returns during both bear and bull markets.

Paper Preview

Abstract

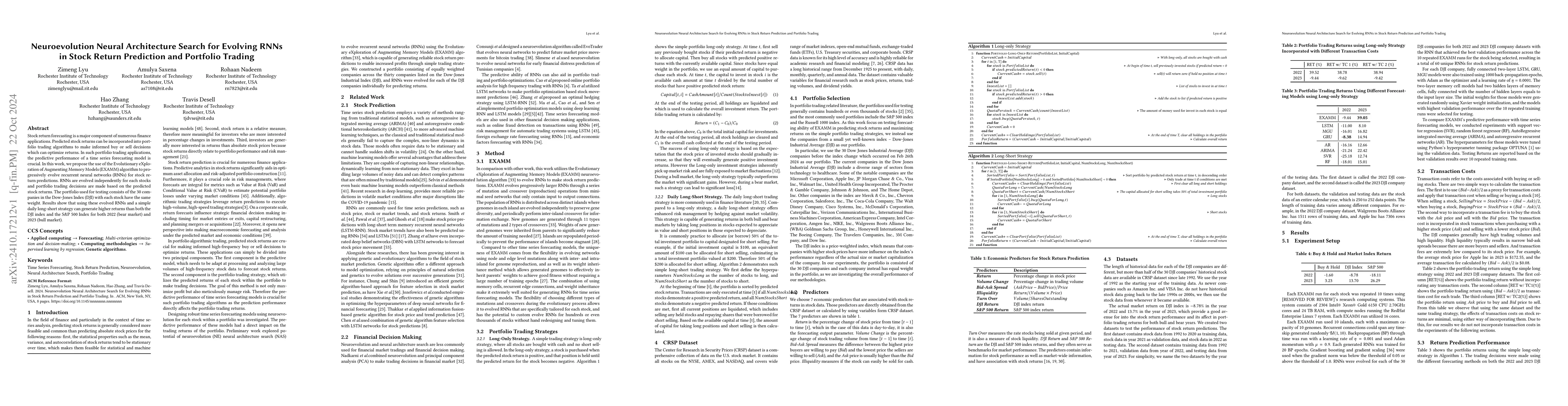

Stock return forecasting is a major component of numerous finance applications. Predicted stock returns can be incorporated into portfolio trading algorithms to make informed buy or sell decisions which can optimize returns. In such portfolio trading applications, the predictive performance of a time series forecasting model is crucial. In this work, we propose the use of the Evolutionary eXploration of Augmenting Memory Models (EXAMM) algorithm to progressively evolve recurrent neural networks (RNNs) for stock return predictions. RNNs are evolved independently for each stocks and portfolio trading decisions are made based on the predicted stock returns. The portfolio used for testing consists of the 30 companies in the Dow-Jones Index (DJI) with each stock have the same weight. Results show that using these evolved RNNs and a simple daily long-short strategy can generate higher returns than both the DJI index and the S&P 500 Index for both 2022 (bear market) and 2023 (bull market).

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0