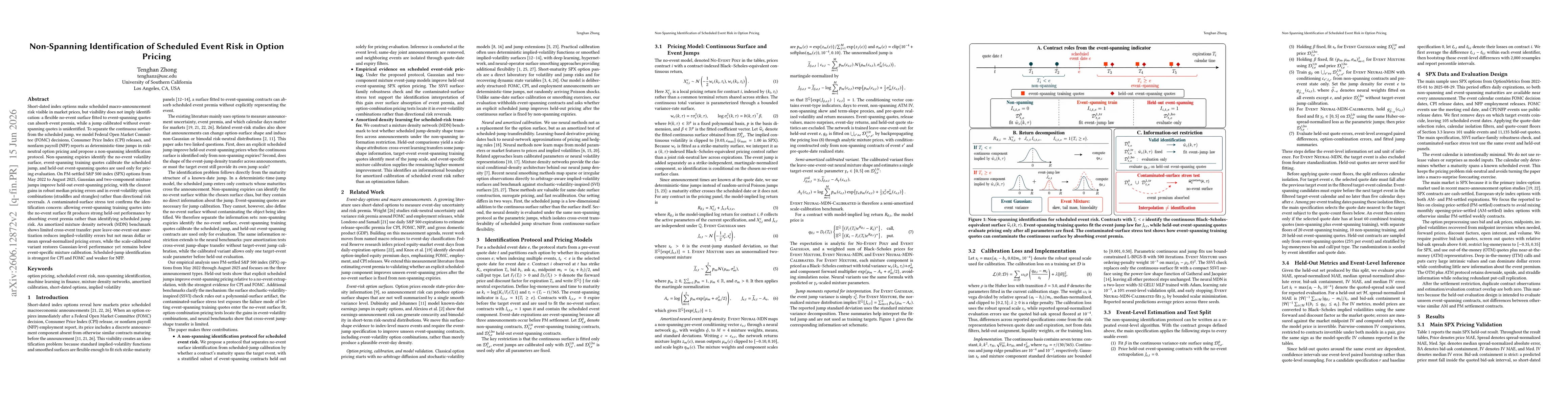

The study adopts a non-spanning identification protocol that separates no-event surface fitting (using non-spanning expiries) from scheduled-jump calibration (using event-spanning training quotes), with held-out event-spanning quotes reserved for pricing evaluation; it models deterministic-time jumps for FOMC, CPI, and NFP, and compares Gaussian and two-component mixture jump specifications, plus an amortized mixture density network (MDN) benchmark under an event-level inference framework. Surface robustness is tested using an SSVI-like check and a contaminated-surface stress test to verify identification; cross-event transfer is evaluated via pure leave-one-event-out and calibrated variants of Event Neural-MDN, with held-out pricing as the ultimate evaluation metric.

Non-Spanning Identification of Scheduled Event Risk in Option Pricing

Publication

Metrics

Quick Answers

What methodology did the authors use?

The study adopts a non-spanning identification protocol that separates no-event surface fitting (using non-spanning expiries) from scheduled-jump calibration (using event-spanning training quotes), with held-out event-spanning quotes reserved for pricing evaluation; it models deterministic-time jumps for FOMC, CPI, and NFP, and compares Gaussian and two-component mixture jump specifications, plus an amortized mixture density network (MDN) benchmark under an event-level inference framework.... More in Methodology →

What are the key results?

Event-jump models (Gaussian and two-component mixtures) improve held-out event-spanning SPX option pricing, especially in event-volatility combinations like ATM straddles and 25-delta strangles. — Contaminated-surface stress tests show that allowing event-spanning training quotes into the no-events surface fit absorbs event premia, undermining identification of the scheduled jump. More in Key Results →

Why is this work significant?

The paper provides a concrete identification protocol that disentangles scheduled-event risk from flexible no-event surfaces, clarifying when event jumps can be identified and how cross-event transferability behaves; it highlights the risk of contaminating no-event surfaces and demonstrates how calibrated cross-event models can partially recover jump risk. More in Significance →

What are the main limitations?

Identification strength varies by event type, with NFP showing weaker identifiable jump components due to data characteristics. — Cross-event transfer remains limited, suggesting that jump shapes are largely event-specific and challenging to generalize without target-event calibration. More in Limitations →

Paper Preview

Abstract

Short-dated index options make scheduled macro-announcement risk visible in market prices, but identification is nontrivial: a flexible no-event surface fitted to event-spanning quotes can absorb event premia, while a jump calibrated without event-spanning quotes is unidentified. We therefore model Federal Open Market Committee (FOMC) decisions, Consumer Price Index (CPI) releases, and nonfarm payroll (NFP) reports as deterministic-time jumps in risk-neutral option pricing and propose a non-spanning identification protocol. Non-spanning expiries identify the no-event volatility surface, event-spanning training quotes calibrate the scheduled jump, and held-out event-spanning quotes are used only for pricing evaluation. On PM-settled S\&P 500 index (SPX) options from May 2022 to August 2025, Gaussian and two-component mixture jumps improve held-out event-spanning pricing, with the clearest gains in robust median pricing errors and in event-volatility option combinations (straddles and strangles) rather than directional risk reversals. A contaminated-surface stress test confirms the identification concern: allowing event-spanning training quotes into the no-event surface fit produces strong held-out performance by absorbing event premia rather than identifying scheduled jump risk. An amortized mixture density network (MDN) benchmark shows limited cross-event transfer: pure leave-one-event-out amortization reduces implied-volatility errors but not mean dollar or mean spread-normalized pricing errors, while the scale-calibrated variant restores Gaussian-level performance yet remains below event-specific mixture calibration. Scheduled-jump identification is strongest for CPI and FOMC and weaker for NFP.

Key Findings, in focus

Seven facets of this paper, analysed and brought into focus by AI.

The paper provides a concrete identification protocol that disentangles scheduled-event risk from flexible no-event surfaces, clarifying when event jumps can be identified and how cross-event transferability behaves; it highlights the risk of contaminating no-event surfaces and demonstrates how calibrated cross-event models can partially recover jump risk.

- Event-jump models (Gaussian and two-component mixtures) improve held-out event-spanning SPX option pricing, especially in event-volatility combinations like ATM straddles and 25-delta strangles.

- Contaminated-surface stress tests show that allowing event-spanning training quotes into the no-events surface fit absorbs event premia, undermining identification of the scheduled jump.

- Cross-event transfer is limited: pure leave-one-event-out amortization reduces IV errors but not mean pricing errors; a scale-calibrated variant restores Gaussian-level performance yet remains below event-specific mixture calibration.

- Event-jump identification is strongest for CPI and FOMC, weaker for NFP, consistent with the data-driven lower-bound scale identification estimates.

The paper provides a concrete identification protocol that disentangles scheduled-event risk from flexible no-event surfaces, clarifying when event jumps can be identified and how cross-event transferability behaves; it highlights the risk of contaminating no-event surfaces and demonstrates how calibrated cross-event models can partially recover jump risk.

Proposal of a non-spanning identification protocol that fixes the no-event surface with non-spanning expiries before calibrating scheduled jumps using event-spanning quotes; formal event-level inference separating training and evaluation sets; empirical demonstration that Gaussian and two-component mixture jumps improve held-out pricing for event-spanning contracts; introduction of an amortized MDN benchmark to study cross-event transfer of jump-shape densities.

Introduces a strict separation between no-event surface identification and scheduled-jump calibration to identify scheduled-event risk, demonstrates the limits of cross-event transfer for jump shapes, and provides an empirical validation showing limited cross-event transfer with a calibrated neural network approach, emphasizing CPI/FOMC prominence over NFP.

- Identification strength varies by event type, with NFP showing weaker identifiable jump components due to data characteristics.

- Cross-event transfer remains limited, suggesting that jump shapes are largely event-specific and challenging to generalize without target-event calibration.

- Results are based on PM-settled SPX options in a specific window (May 2022–Aug 2025) and may be sensitive to regime changes or market structure shifts.

- MDN-based cross-event transfers show only partial improvements, indicating room for alternative transfer-learning architectures or richer event taxonomy.

- Test whether the identified boundary persists intraday or across broader market segments (other indices, futures, or different maturities).

- Investigate earlier target-event scale identifiability under higher-frequency data or richer event panels to enhance transferability.

- Explore more flexible amortization schemes or hierarchical mixtures to improve cross-event density transfer while preserving identification.

- Examine cross-market and richer-event panels to assess whether target-event scale becomes identifiable sooner and to study more complex event interactions.

Discussion 0