Academic Profile

Statistics

Similar Authors

Papers on arXiv

We present a fast and robust calibration method for stochastic volatility models that admit Fourier-analytic transform-based pricing via characteristic functions. The design is structure-preserving: w...

We introduce a proxy-reliance-controlled conformal recalibration framework for one-sided Value-at-Risk (VaR), and study a question that existing state-aware methods do not usually isolate: how strongl...

Short-horizon risk control matters for hedging and capital allocation. Yet existing Value-at-Risk studies rarely address standardized option books or the next-day valuation frictions that arise in der...

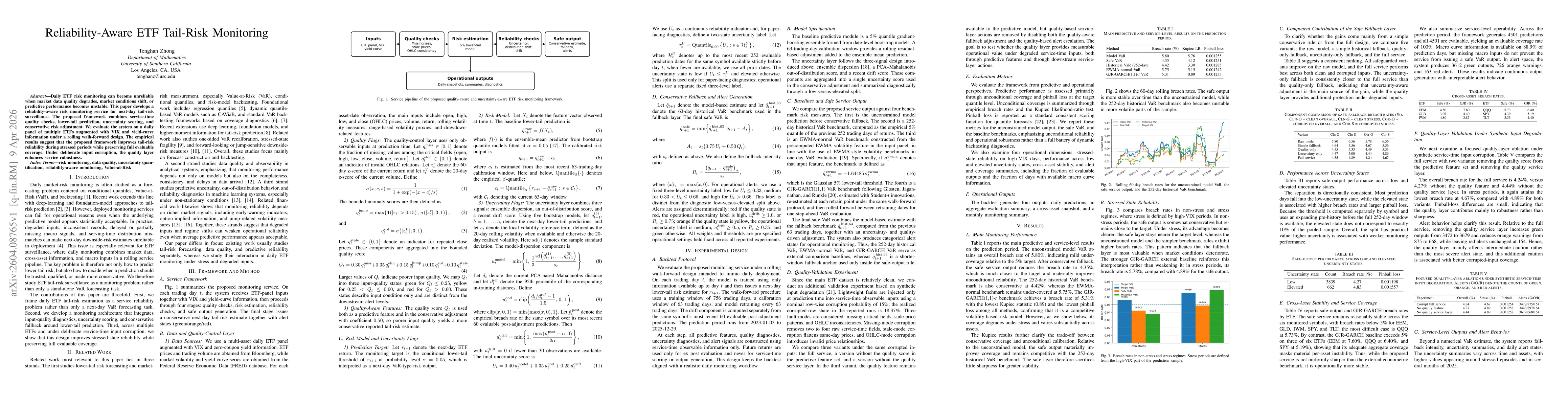

Daily ETF risk monitoring can become unreliable when market data quality degrades, market conditions shift, or predictive performance becomes unstable. This paper develops a reliability-aware risk mon...

Volatility forecasting becomes challenging when market conditions change and model performance varies across regimes. Motivated by this instability, we develop a regime-aware specialist routing framew...

We study a finite-inventory risk-sensitive market making problem in which a dealer controls bid and ask quotes, faces Brownian midprice risk, and receives liquidity-taking orders through point process...

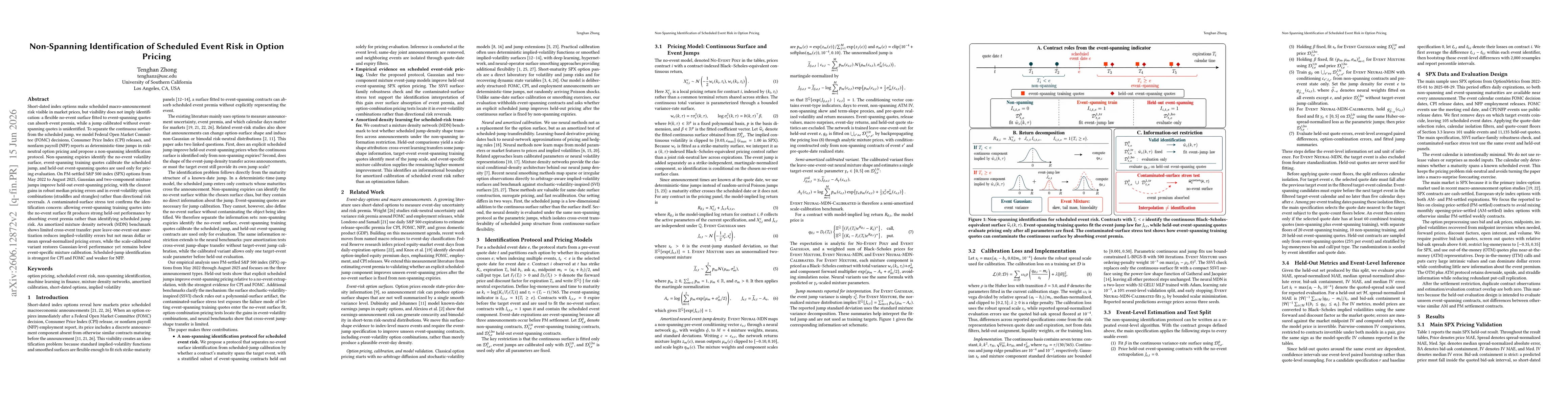

Short-dated index options make scheduled macro-announcement risk visible in market prices, but identification is nontrivial: a flexible no-event surface fitted to event-spanning quotes can absorb even...