01

MethodologyHow they did it

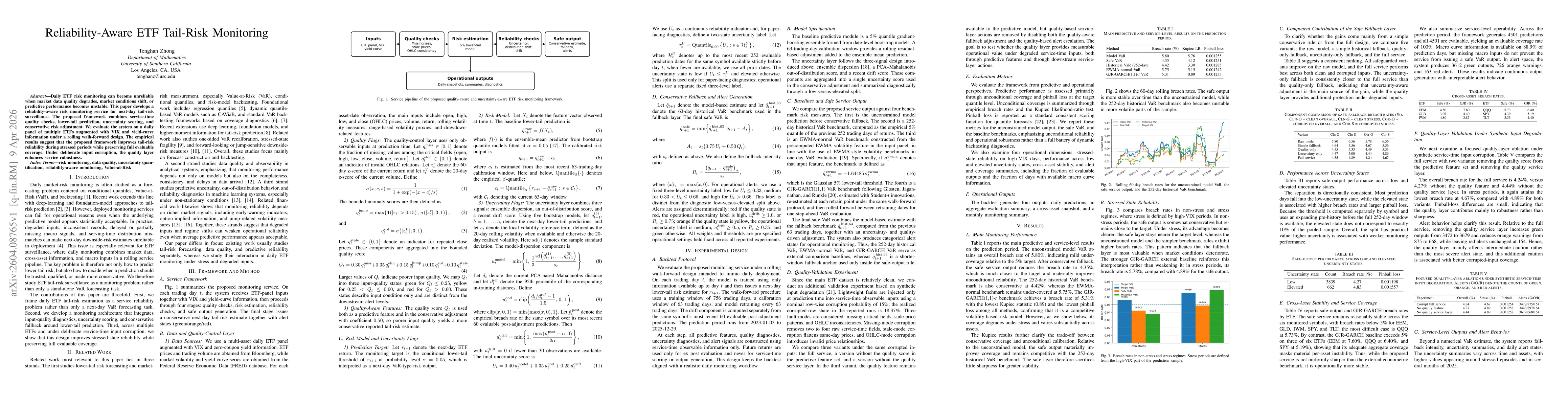

Daily ETF tail‑risk monitoring framework that integrates service‑time quality checks, lower‑tail prediction via a 5% quantile gradient‑boosting ensemble, uncertainty scoring (ensemble dispersion, OOD Mahalanobis, drift), and a conservative fallback adjustment calibrated on a 63‑day window, evaluated with a rolling walk‑forward design.

Discussion 0