Non-stationary Risk-sensitive Reinforcement Learning: Near-optimal Dynamic Regret, Adaptive Detection, and Separation Design

Publication

Metrics

AI Quick Summary

This paper proposes algorithms for risk-sensitive reinforcement learning in non-stationary Markov decision processes, establishing near-optimal dynamic regret bounds. It introduces adaptive detection mechanisms for non-stationary environments and demonstrates separation design for risk control and non-stationarity handling.

Paper Preview

Abstract

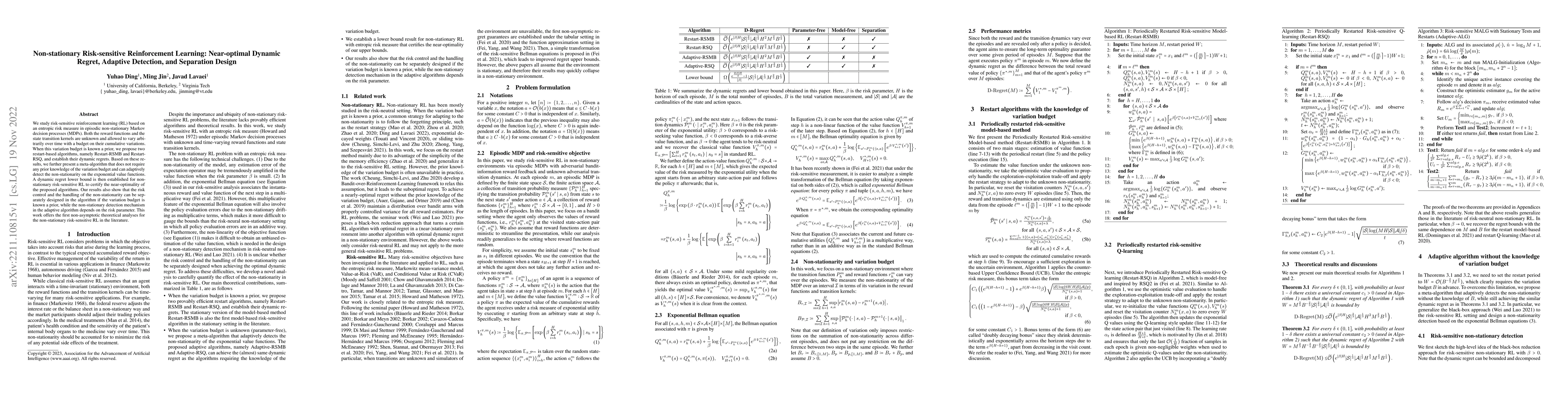

We study risk-sensitive reinforcement learning (RL) based on an entropic risk measure in episodic non-stationary Markov decision processes (MDPs). Both the reward functions and the state transition kernels are unknown and allowed to vary arbitrarily over time with a budget on their cumulative variations. When this variation budget is known a prior, we propose two restart-based algorithms, namely Restart-RSMB and Restart-RSQ, and establish their dynamic regrets. Based on these results, we further present a meta-algorithm that does not require any prior knowledge of the variation budget and can adaptively detect the non-stationarity on the exponential value functions. A dynamic regret lower bound is then established for non-stationary risk-sensitive RL to certify the near-optimality of the proposed algorithms. Our results also show that the risk control and the handling of the non-stationarity can be separately designed in the algorithm if the variation budget is known a prior, while the non-stationary detection mechanism in the adaptive algorithm depends on the risk parameter. This work offers the first non-asymptotic theoretical analyses for the non-stationary risk-sensitive RL in the literature.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0