Risk-Sensitive Reinforcement Learning: Near-Optimal Risk-Sample Tradeoff in Regret

Publication

Metrics

AI Quick Summary

This paper proposes two efficient model-free algorithms, Risk-Sensitive Value Iteration (RSVI) and Risk-Sensitive Q-learning (RSQ), for optimizing rewards in risk-sensitive reinforcement learning under exponential utility. The algorithms achieve near-optimal regret bounds, demonstrating the fundamental tradeoff between risk sensitivity and sample efficiency.

Paper Preview

Abstract

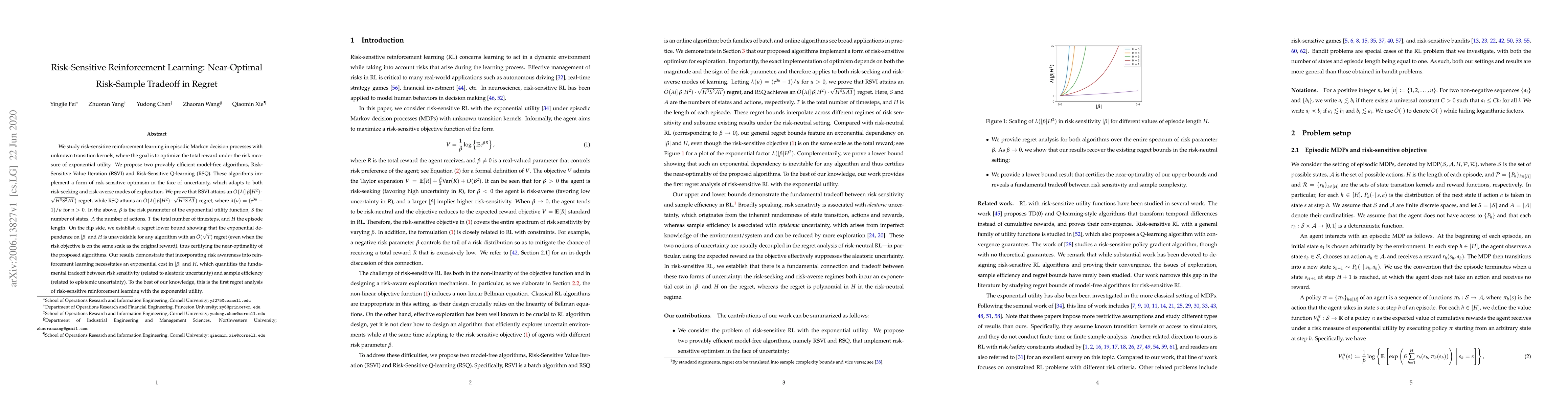

We study risk-sensitive reinforcement learning in episodic Markov decision processes with unknown transition kernels, where the goal is to optimize the total reward under the risk measure of exponential utility. We propose two provably efficient model-free algorithms, Risk-Sensitive Value Iteration (RSVI) and Risk-Sensitive Q-learning (RSQ). These algorithms implement a form of risk-sensitive optimism in the face of uncertainty, which adapts to both risk-seeking and risk-averse modes of exploration. We prove that RSVI attains an $\tilde{O}\big(\lambda(|\beta| H^2) \cdot \sqrt{H^{3} S^{2}AT} \big)$ regret, while RSQ attains an $\tilde{O}\big(\lambda(|\beta| H^2) \cdot \sqrt{H^{4} SAT} \big)$ regret, where $\lambda(u) = (e^{3u}-1)/u$ for $u>0$. In the above, $\beta$ is the risk parameter of the exponential utility function, $S$ the number of states, $A$ the number of actions, $T$ the total number of timesteps, and $H$ the episode length. On the flip side, we establish a regret lower bound showing that the exponential dependence on $|\beta|$ and $H$ is unavoidable for any algorithm with an $\tilde{O}(\sqrt{T})$ regret (even when the risk objective is on the same scale as the original reward), thus certifying the near-optimality of the proposed algorithms. Our results demonstrate that incorporating risk awareness into reinforcement learning necessitates an exponential cost in $|\beta|$ and $H$, which quantifies the fundamental tradeoff between risk sensitivity (related to aleatoric uncertainty) and sample efficiency (related to epistemic uncertainty). To the best of our knowledge, this is the first regret analysis of risk-sensitive reinforcement learning with the exponential utility.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0