Publication

Metrics

AI Quick Summary

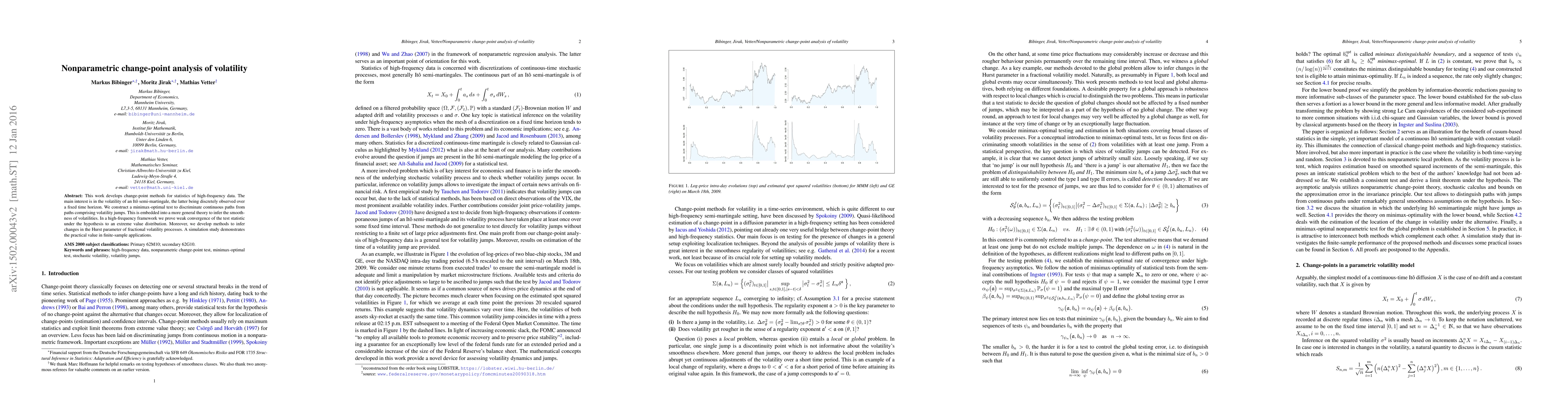

This paper develops nonparametric change-point methods for analyzing volatility in high-frequency data, constructing a minimax-optimal test to detect volatility jumps and changes in the Hurst parameter. Simulation results show practical applicability in real-world scenarios.

Paper Preview

Abstract

This work develops change-point methods for statistics of high-frequency data. The main interest is in the volatility of an It\^{o} semi-martingale, the latter being discretely observed over a fixed time horizon. We construct a minimax-optimal test to discriminate continuous paths from paths comprising volatility jumps. This is embedded into a more general theory to infer the smoothness of volatilities. In a high-frequency framework we prove weak convergence of the test statistic under the hypothesis to an extreme value distribution. Moreover, we develop methods to infer changes in the Hurst parameter of fractional volatility processes. A simulation study demonstrates the practical value in finite-sample applications.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0