On Optimizing the Conditional Value-at-Risk of a Maximum Cost for Risk-Averse Safety Analysis

Publication

Metrics

AI Quick Summary

Researchers develop a new method to analyze safety in complex systems by minimizing the severity of potential failures, providing a more nuanced approach than existing risk assessment frameworks.

Paper Preview

Abstract

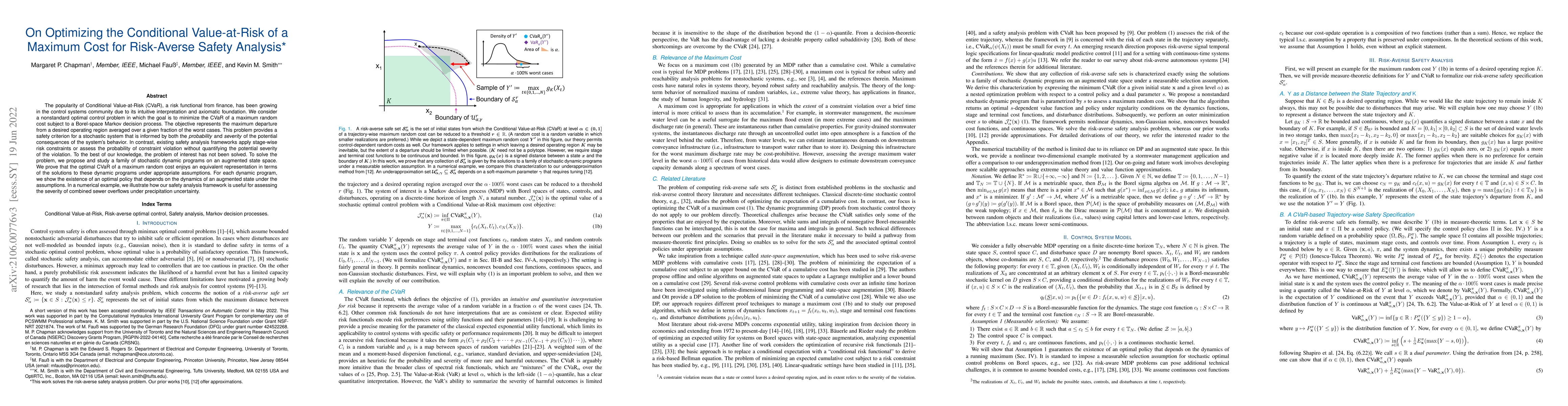

The popularity of Conditional Value-at-Risk (CVaR), a risk functional from finance, has been growing in the control systems community due to its intuitive interpretation and axiomatic foundation. We consider a nonstandard optimal control problem in which the goal is to minimize the CVaR of a maximum random cost subject to a Borel-space Markov decision process. The objective represents the maximum departure from a desired operating region averaged over a given fraction of the worst cases. This problem provides a safety criterion for a stochastic system that is informed by both the probability and severity of the potential consequences of the system's behavior. In contrast, existing safety analysis frameworks apply stage-wise risk constraints or assess the probability of constraint violation without quantifying the potential severity of the violation. To the best of our knowledge, the problem of interest has not been solved. To solve the problem, we propose and study a family of stochastic dynamic programs on an augmented state space. We prove that the optimal CVaR of a maximum random cost enjoys an equivalent representation in terms of the solutions to these dynamic programs under appropriate assumptions. For each dynamic program, we show the existence of an optimal policy that depends on the dynamics of an augmented state under the assumptions. In a numerical example, we illustrate how our safety analysis framework is useful for assessing the severity of combined sewer overflows under precipitation uncertainty.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0