Authors

Summary

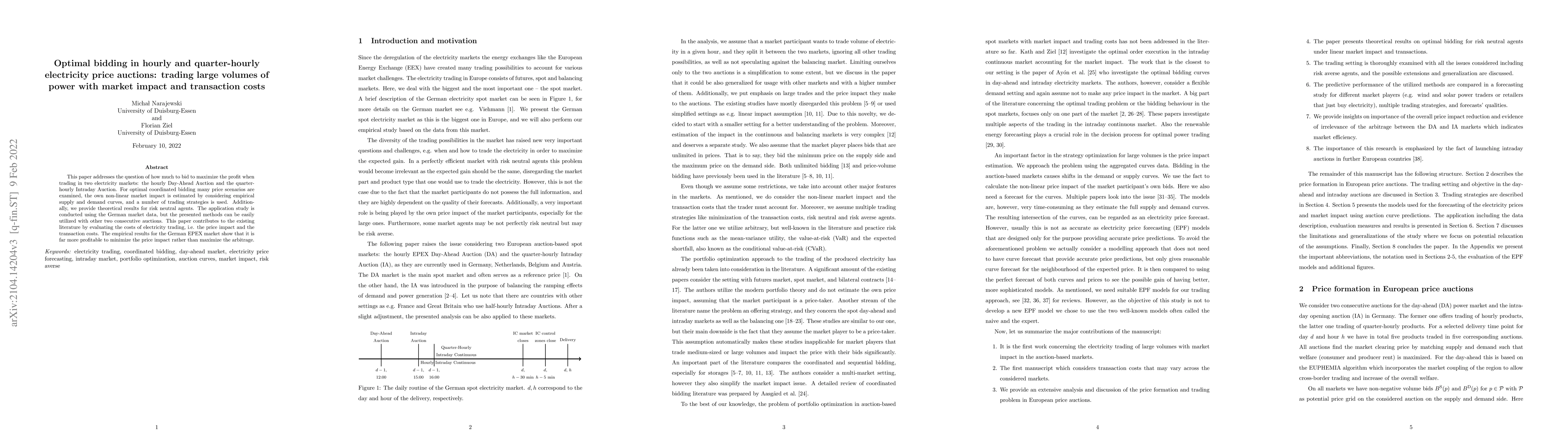

This paper addresses the question of how much to bid to maximize the profit when trading in two electricity markets: the hourly Day-Ahead Auction and the quarter-hourly Intraday Auction. For optimal coordinated bidding many price scenarios are examined, the own non-linear market impact is estimated by considering empirical supply and demand curves, and a number of trading strategies is used. Additionally, we provide theoretical results for risk neutral agents. The application study is conducted using the German market data, but the presented methods can be easily utilized with other two consecutive auctions. This paper contributes to the existing literature by evaluating the costs of electricity trading, i.e. the price impact and the transaction costs. The empirical results for the German EPEX market show that it is far more profitable to minimize the price impact rather than maximize the arbitrage.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersModelling the Hourly Consumption of Electricity during Period of Power Crisis

Samuel Asante Gyamerah, Henry Ofoe Agbi-Kaiser, Keziah Ewura Adjoa Amankwah et al.

Deep Learning-Based Electricity Price Forecast for Virtual Bidding in Wholesale Electricity Market

Xuesong Wang, Caisheng Wang, Sharaf K. Magableh et al.

| Title | Authors | Year | Actions |

|---|

Comments (0)