Publication

Metrics

AI Quick Summary

Pair-copula Bayesian networks (PCBNs) combine pair-copula constructions with directed acyclic graphs for flexible multivariate modeling. The paper introduces algorithms for random sampling, likelihood inference, and model selection, demonstrating their effectiveness through a simulation study on financial return data.

Paper Preview

Abstract

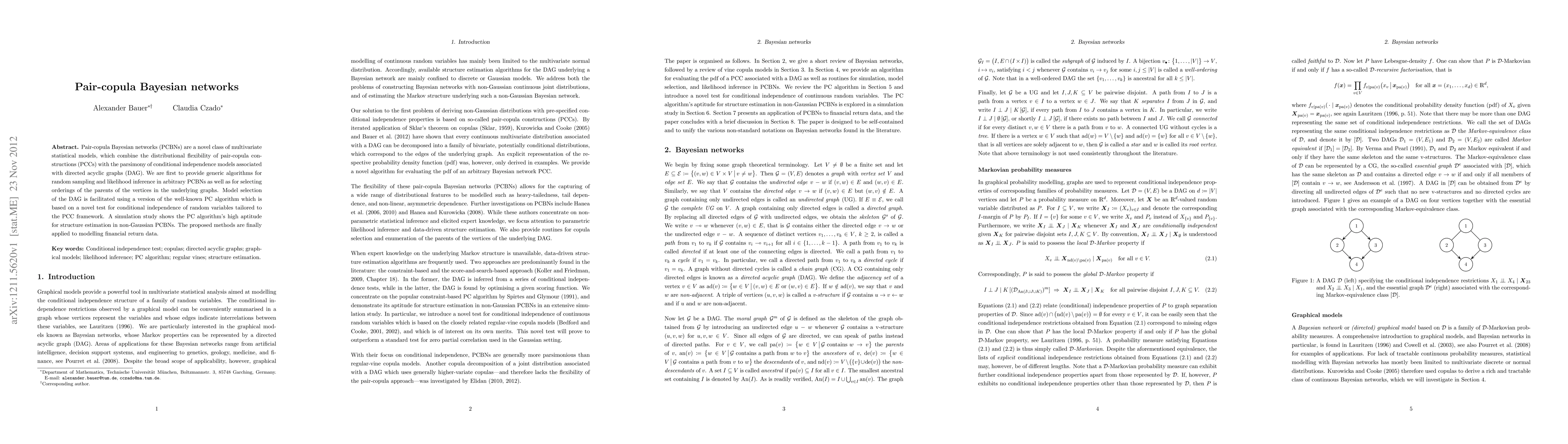

Pair-copula Bayesian networks (PCBNs) are a novel class of multivariate statistical models, which combine the distributional flexibility of pair-copula constructions (PCCs) with the parsimony of conditional independence models associated with directed acyclic graphs (DAG). We are first to provide generic algorithms for random sampling and likelihood inference in arbitrary PCBNs as well as for selecting orderings of the parents of the vertices in the underlying graphs. Model selection of the DAG is facilitated using a version of the well-known PC algorithm which is based on a novel test for conditional independence of random variables tailored to the PCC framework. A simulation study shows the PC algorithm's high aptitude for structure estimation in non-Gaussian PCBNs. The proposed methods are finally applied to modelling financial return data.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0