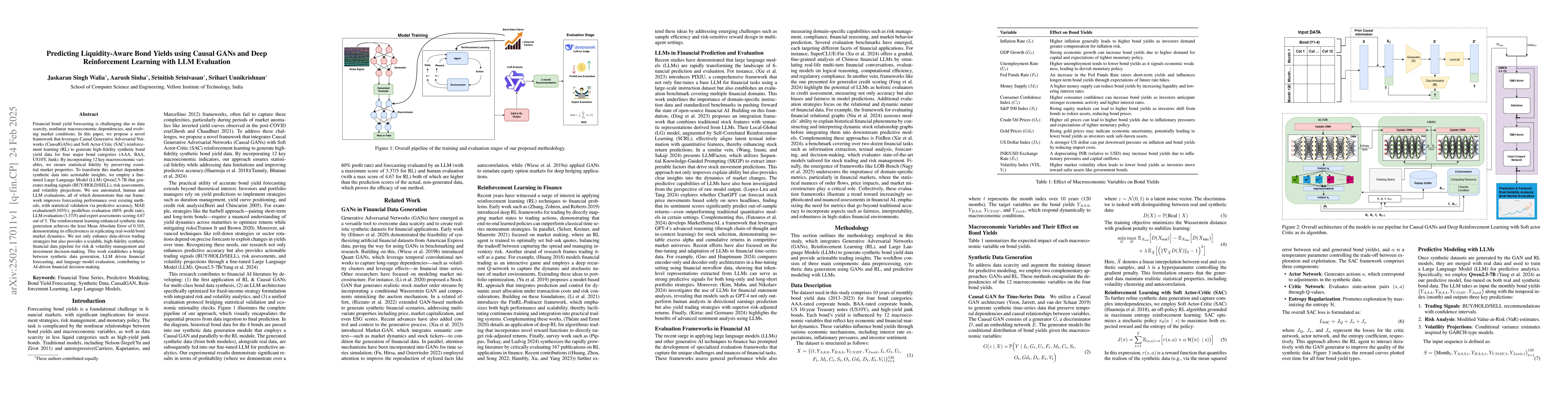

Financial bond yield forecasting is challenging due to data scarcity,

nonlinear macroeconomic dependencies, and evolving market conditions. In this

paper, we propose a novel framework that leverages Causal Generative

Adversarial Networks (CausalGANs) and Soft Actor-Critic (SAC) reinforcement

learning (RL) to generate high-fidelity synthetic bond yield data for four

major bond categories (AAA, BAA, US10Y, Junk). By incorporating 12 key

macroeconomic variables, we ensure statistical fidelity by preserving essential

market properties. To transform this market dependent synthetic data into

actionable insights, we employ a finetuned Large Language Model (LLM)

Qwen2.5-7B that generates trading signals (BUY/HOLD/SELL), risk assessments,

and volatility projections. We use automated, human and LLM evaluations, all of

which demonstrate that our framework improves forecasting performance over

existing methods, with statistical validation via predictive accuracy, MAE

evaluation(0.103%), profit/loss evaluation (60% profit rate), LLM evaluation

(3.37/5) and expert assessments scoring 4.67 out of 5. The reinforcement

learning-enhanced synthetic data generation achieves the least Mean Absolute

Error of 0.103, demonstrating its effectiveness in replicating real-world bond

market dynamics. We not only enhance data-driven trading strategies but also

provides a scalable, high-fidelity synthetic financial data pipeline for risk &

volatility management and investment decision-making. This work establishes a

bridge between synthetic data generation, LLM driven financial forecasting, and

language model evaluation, contributing to AI-driven financial decision-making.

Discussion 0