Publication

Metrics

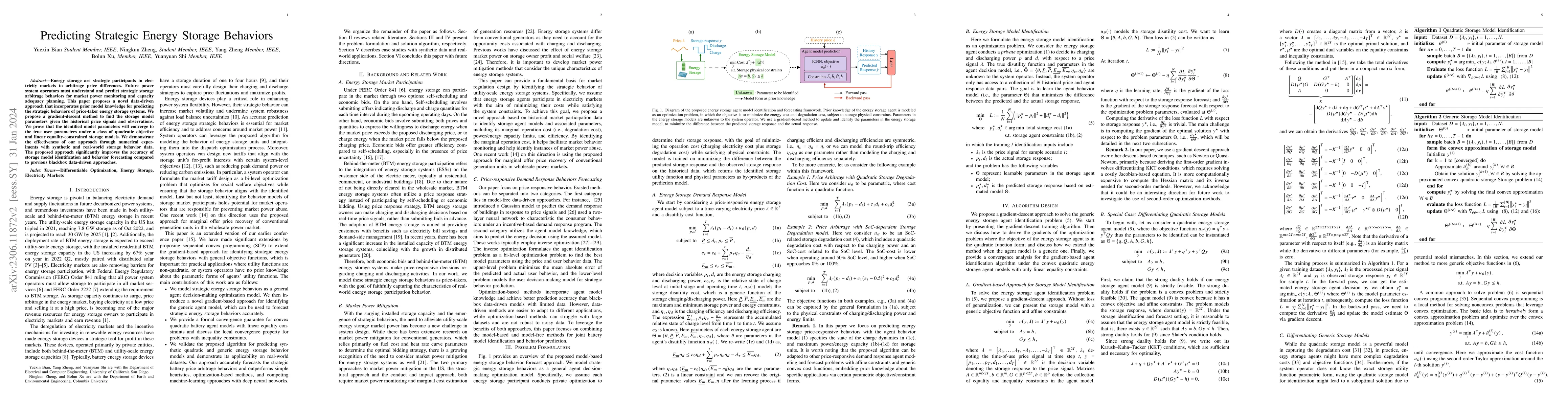

AI Quick Summary

This paper introduces a novel data-driven method for predicting the strategic behaviors of price-taker energy storage systems in electricity markets. The approach uses gradient descent to identify storage model parameters from historical price signals, demonstrating improved accuracy over previous methods through both synthetic and real-world data experiments.

Paper Preview

Abstract

Energy storage are strategic participants in electricity markets to arbitrage price differences. Future power system operators must understand and predict strategic storage arbitrage behaviors for market power monitoring and capacity adequacy planning. This paper proposes a novel data-driven approach that incorporates prior model knowledge for predicting the strategic behaviors of price-taker energy storage systems. We propose a gradient-descent method to find the storage model parameters given the historical price signals and observations. We prove that the identified model parameters will converge to the true user parameters under a class of quadratic objective and linear equality-constrained storage models. We demonstrate the effectiveness of our approach through numerical experiments with synthetic and real-world storage behavior data. The proposed approach significantly improves the accuracy of storage model identification and behavior forecasting compared to previous blackbox data-driven approaches.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0