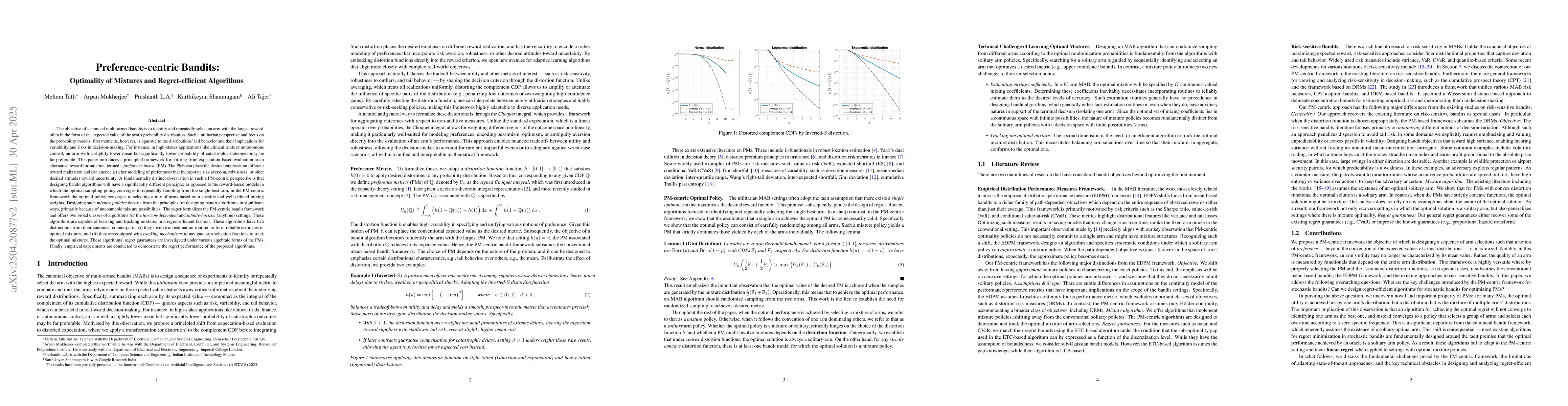

The objective of canonical multi-armed bandits is to identify and repeatedly

select an arm with the largest reward, often in the form of the expected value

of the arm's probability distribution. Such a utilitarian perspective and focus

on the probability models' first moments, however, is agnostic to the

distributions' tail behavior and their implications for variability and risks

in decision-making. This paper introduces a principled framework for shifting

from expectation-based evaluation to an alternative reward formulation, termed

a preference metric (PM). The PMs can place the desired emphasis on different

reward realization and can encode a richer modeling of preferences that

incorporate risk aversion, robustness, or other desired attitudes toward

uncertainty. A fundamentally distinct observation in such a PM-centric

perspective is that designing bandit algorithms will have a significantly

different principle: as opposed to the reward-based models in which the optimal

sampling policy converges to repeatedly sampling from the single best arm, in

the PM-centric framework the optimal policy converges to selecting a mix of

arms based on specific mixing weights. Designing such mixture policies departs

from the principles for designing bandit algorithms in significant ways,

primarily because of uncountable mixture possibilities. The paper formalizes

the PM-centric framework and presents two algorithm classes (horizon-dependent

and anytime) that learn and track mixtures in a regret-efficient fashion. These

algorithms have two distinctions from their canonical counterparts: (i) they

involve an estimation routine to form reliable estimates of optimal mixtures,

and (ii) they are equipped with tracking mechanisms to navigate arm selection

fractions to track the optimal mixtures. These algorithms' regret guarantees

are investigated under various algebraic forms of the PMs.

Discussion 0