Academic Profile

Statistics

Similar Authors

Papers on arXiv

Algorithms for bandit convex optimization and online learning often rely on constructing noisy gradient estimates, which are then used in appropriately adjusted first-order algorithms, replacing act...

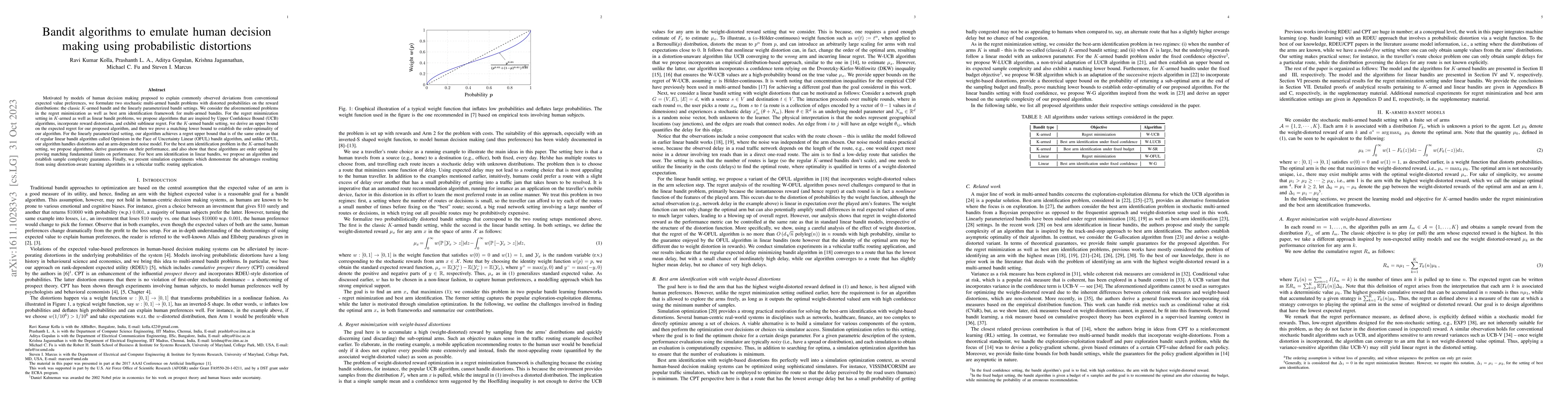

Motivated by models of human decision making proposed to explain commonly observed deviations from conventional expected value preferences, we formulate two stochastic multi-armed bandit problems wi...

We consider the problems of estimation and optimization of utility-based shortfall risk (UBSR), which is a popular risk measure in finance. In the context of UBSR estimation, we derive a non-asympto...

We consider the problem of control in the setting of reinforcement learning (RL), where model information is not available. Policy gradient algorithms are a popular solution approach for this proble...

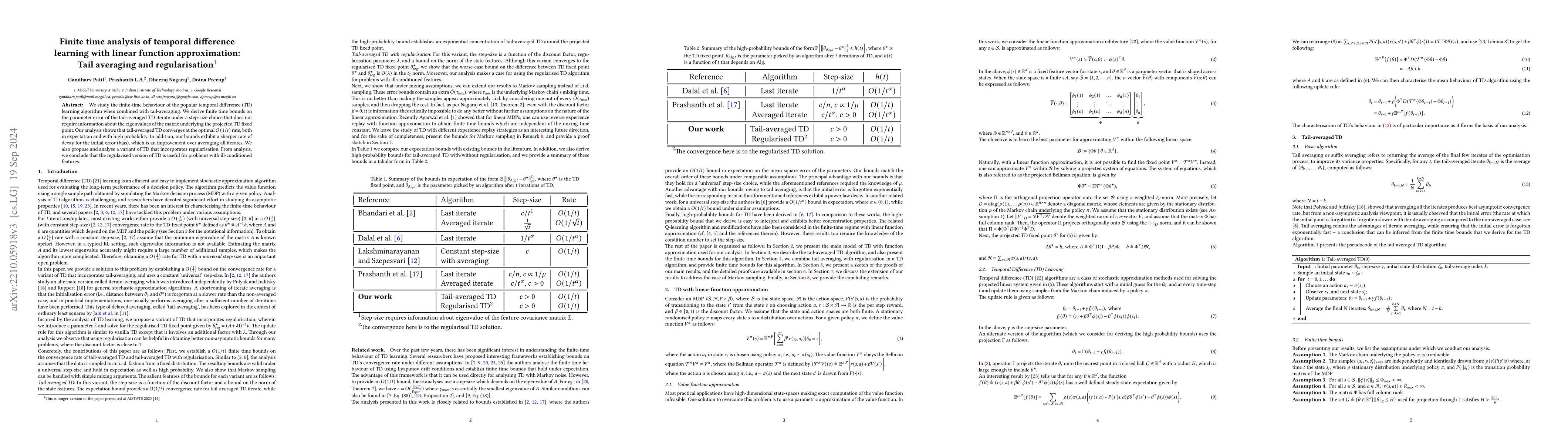

We study the finite-time behaviour of the popular temporal difference (TD) learning algorithm when combined with tail-averaging. We derive finite time bounds on the parameter error of the tail-avera...

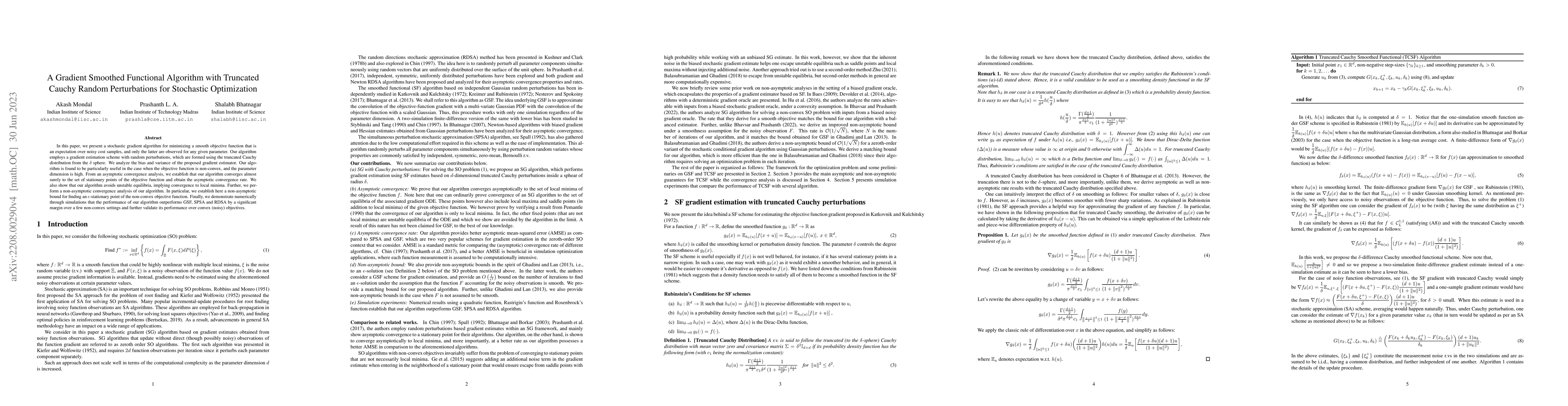

In this paper, we present a stochastic gradient algorithm for minimizing a smooth objective function that is an expectation over noisy cost samples, and only the latter are observed for any given pa...

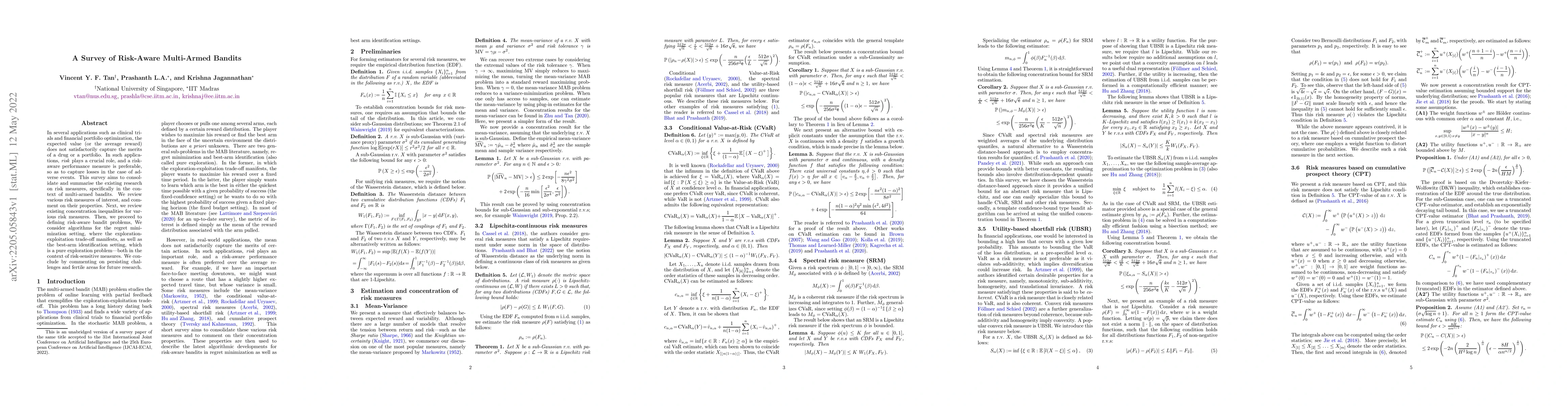

In several applications such as clinical trials and financial portfolio optimization, the expected value (or the average reward) does not satisfactorily capture the merits of a drug or a portfolio. ...

We consider the problem of estimating a spectral risk measure (SRM) from i.i.d. samples, and propose a novel method that is based on numerical integration. We show that our SRM estimate concentrates...

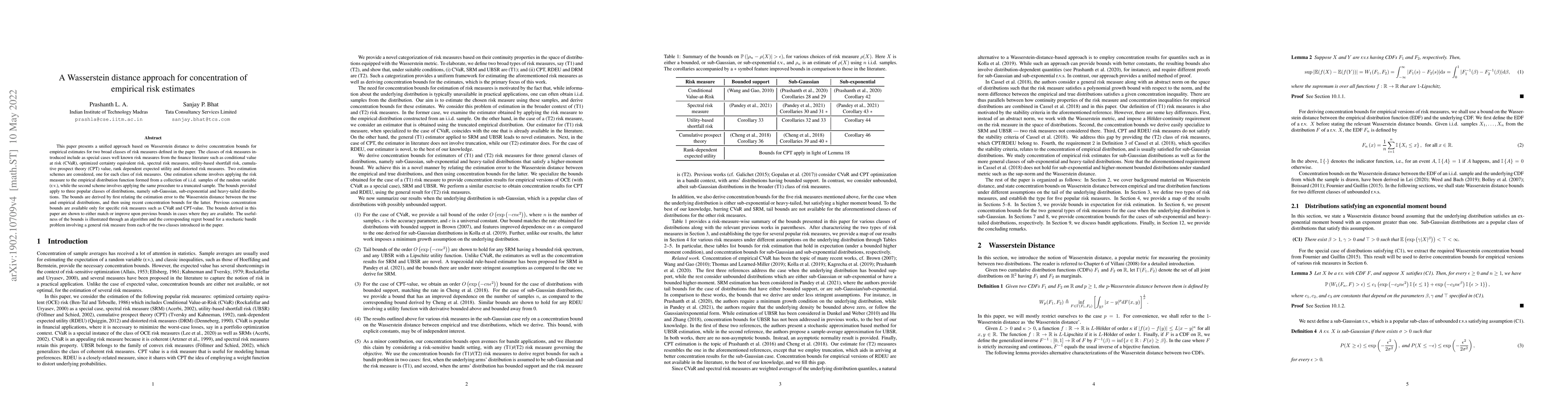

This paper presents a unified approach based on Wasserstein distance to derive concentration bounds for empirical estimates for two broad classes of risk measures defined in the paper. The classes o...

The objective in a traditional reinforcement learning (RL) problem is to find a policy that optimizes the expected value of a performance metric such as the infinite-horizon cumulative discounted or...

We consider the problem of estimating the asymptotic variance of a function defined on a Markov chain, an important step for statistical inference of the stationary mean. We design the first recursive...

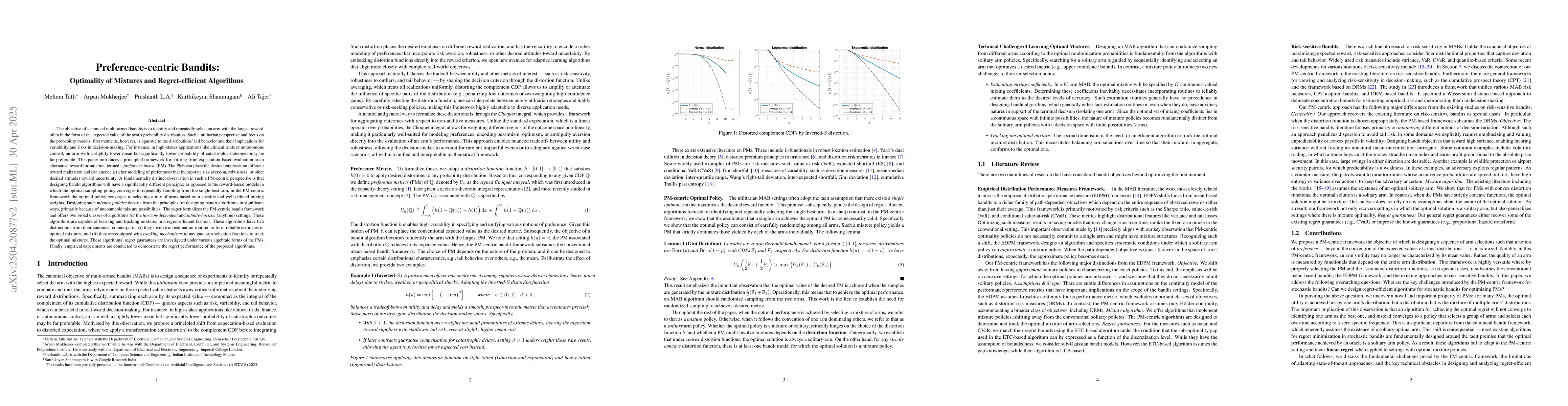

This paper introduces a general framework for risk-sensitive bandits that integrates the notions of risk-sensitive objectives by adopting a rich class of distortion riskmetrics. The introduced framewo...

The objective of canonical multi-armed bandits is to identify and repeatedly select an arm with the largest reward, often in the form of the expected value of the arm's probability distribution. Such ...

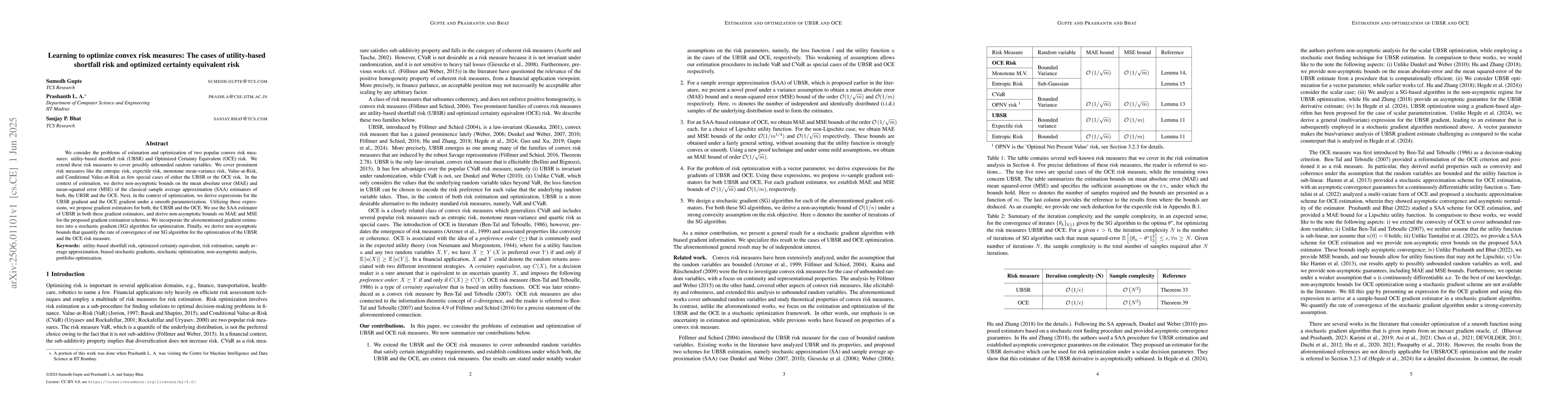

We consider the problems of estimation and optimization of two popular convex risk measures: utility-based shortfall risk (UBSR) and Optimized Certainty Equivalent (OCE) risk. We extend these risk mea...

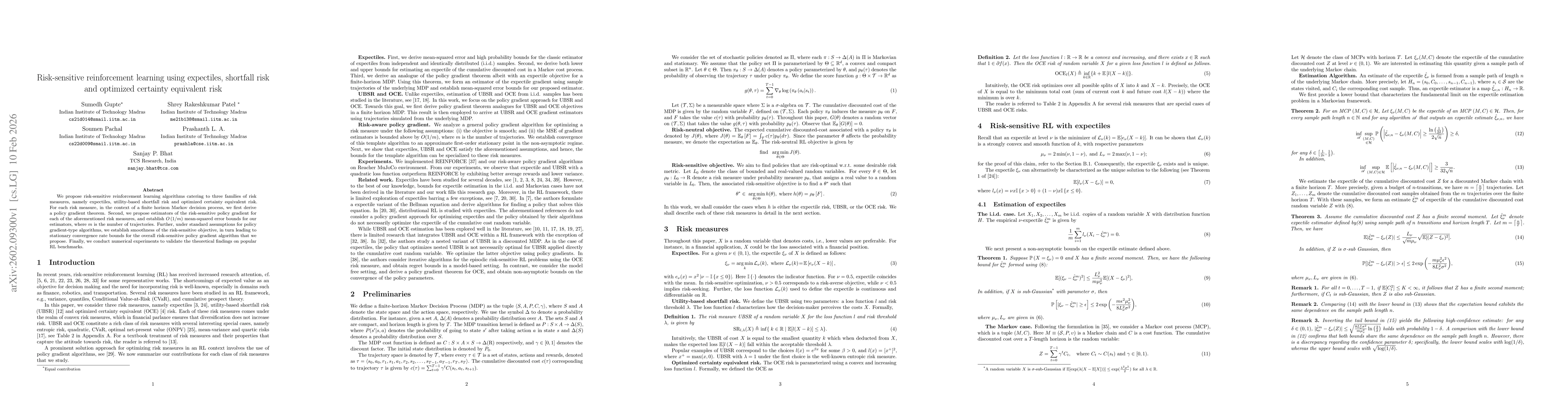

We propose risk-sensitive reinforcement learning algorithms catering to three families of risk measures, namely expectiles, utility-based shortfall risk and optimized certainty equivalent risk. For ea...

We present a family of generalized Hessian estimators of the objective using random direction stochastic approximation (RDSA) by utilizing only noisy function measurements. The form of each estimator ...