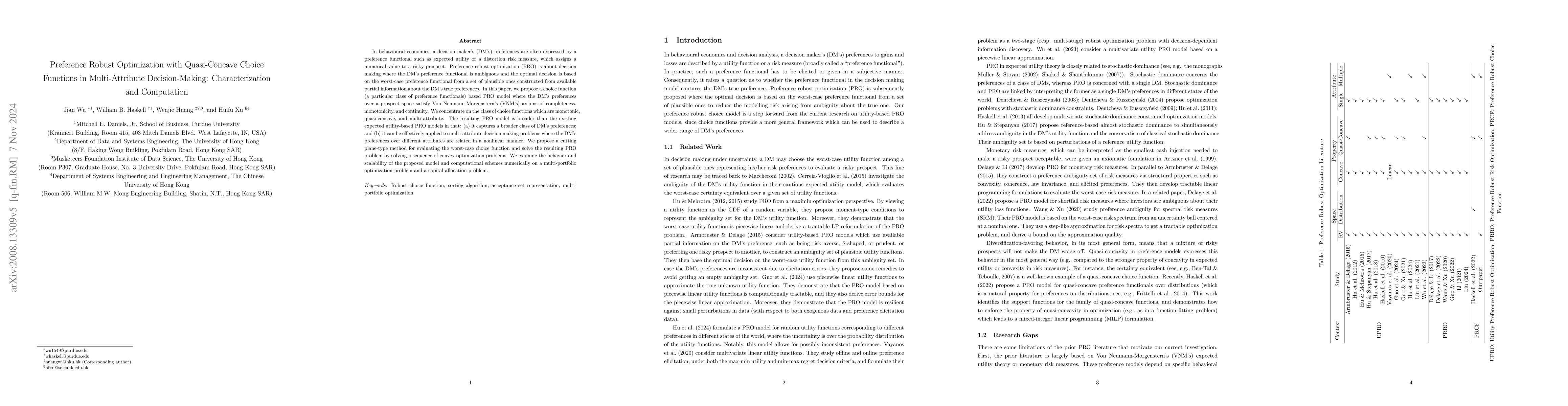

Preference Robust Optimization with Quasi-Concave Choice Functions for Multi-Attribute Prospects

Publication

Metrics

AI Quick Summary

This paper extends preference robust choice models to accommodate quasi-concave choice functions for multi-attribute prospects, addressing the non-convexity through a sorting-based algorithm. It solves preference robust optimization problems via a sequence of convex optimization problems, demonstrating its application in portfolio and capital allocation.

Paper Preview

Abstract

Preference robust choice models concern decision-making problems where the decision maker's (DM) utility/risk preferences are ambiguous and the evaluation is based on the worst-case utility function/risk measure from a set of plausible utility functions/risk measures. The current preference robust choice models are mostly built upon von Neumann-Morgenstern expected utility theory, the theory of convex risk measures, or Yaari's dual theory of choice, all of which assume the DM's preferences satisfy some specified axioms. In this paper, we extend the preference robust approach to a broader class of choice functions which satisfy monotonicity and quasi-concavity in the space of multi-attribute random prospects. While our new model is non-parametric and significantly extends the coverage of decision-making problems, it also brings new computational challenges due to the non-convexity of the optimization formulations, which arises from the non-concavity of the class of quasi-concave choice functions. To tackle these challenges, we develop a sorting-based algorithm that efficiently evaluates the robust choice function (RCF) by solving a sequence of linear programming problems. Then, we show how to solve preference robust optimization (PRO) problems by solving a sequence of convex optimization problems. We test our robust choice model and computational scheme on a single-attribute portfolio optimization problem and a multi-attribute capital allocation problem.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Paper Details

PDF Preview

Key Terms

Related Papers

No references found for this paper.

Discussion 0