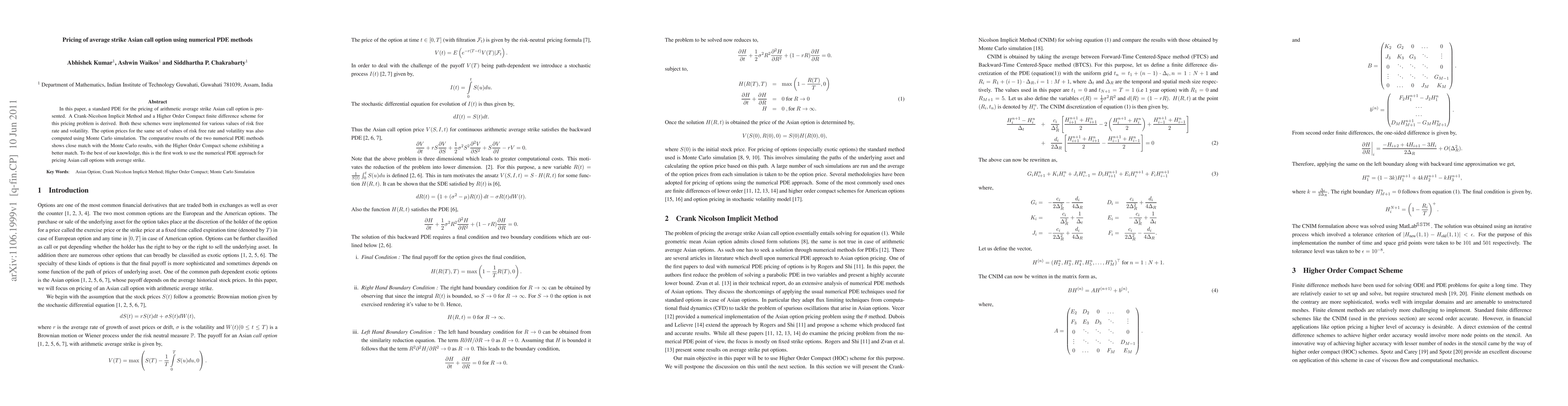

In this paper, a standard PDE for the pricing of arithmetic average strike

Asian call option is presented. A Crank-Nicolson Implicit Method and a Higher

Order Compact finite difference scheme for this pricing problem is derived.

Both these schemes were implemented for various values of risk free rate and

volatility. The option prices for the same set of values of risk free rate and

volatility was also computed using Monte Carlo simulation. The comparative

results of the two numerical PDE methods shows close match with the Monte Carlo

results, with the Higher Order Compact scheme exhibiting a better match. To the

best of our knowledge, this is the first work to use the numerical PDE approach

for pricing Asian call options with average strike.

Discussion 0