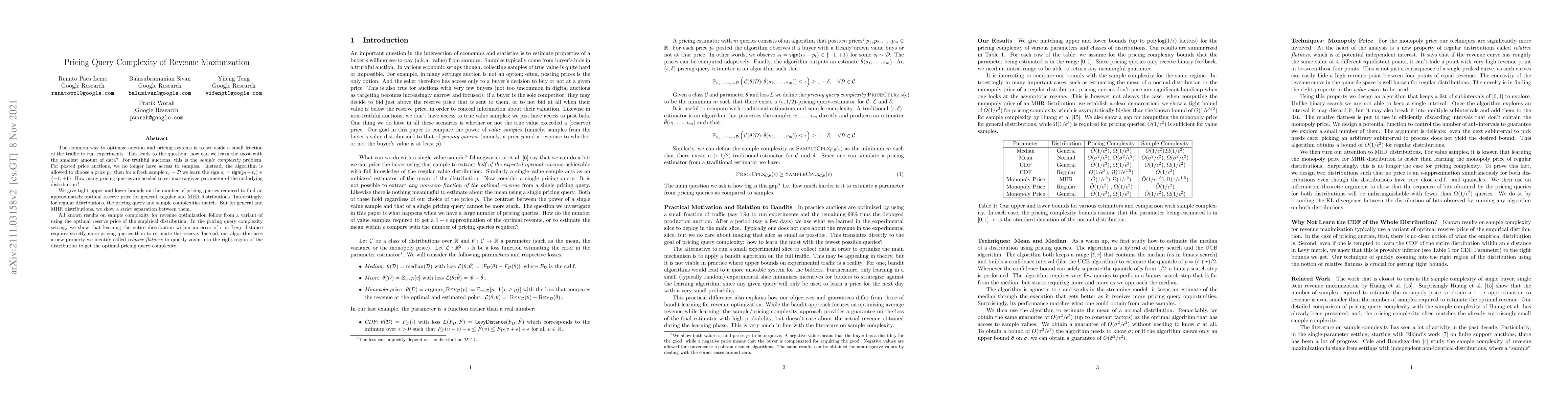

The common way to optimize auction and pricing systems is to set aside a

small fraction of the traffic to run experiments. This leads to the question:

how can we learn the most with the smallest amount of data? For truthful

auctions, this is the \emph{sample complexity} problem. For posted price

auctions, we no longer have access to samples. Instead, the algorithm is

allowed to choose a price $p_t$; then for a fresh sample $v_t \sim \mathcal{D}$

we learn the sign $s_t = sign(p_t - v_t) \in \{-1,+1\}$. How many pricing

queries are needed to estimate a given parameter of the underlying

distribution?

We give tight upper and lower bounds on the number of pricing queries

required to find an approximately optimal reserve price for general, regular

and MHR distributions. Interestingly, for regular distributions, the pricing

query and sample complexities match. But for general and MHR distributions, we

show a strict separation between them.

All known results on sample complexity for revenue optimization follow from a

variant of using the optimal reserve price of the empirical distribution. In

the pricing query complexity setting, we show that learning the entire

distribution within an error of $\epsilon$ in Levy distance requires strictly

more pricing queries than to estimate the reserve. Instead, our algorithm uses

a new property we identify called \emph{relative flatness} to quickly zoom into

the right region of the distribution to get the optimal pricing query

complexity.

Discussion 0