Social financial technology focuses on trust, sustainability, and social

responsibility, which require advanced technologies to address complex

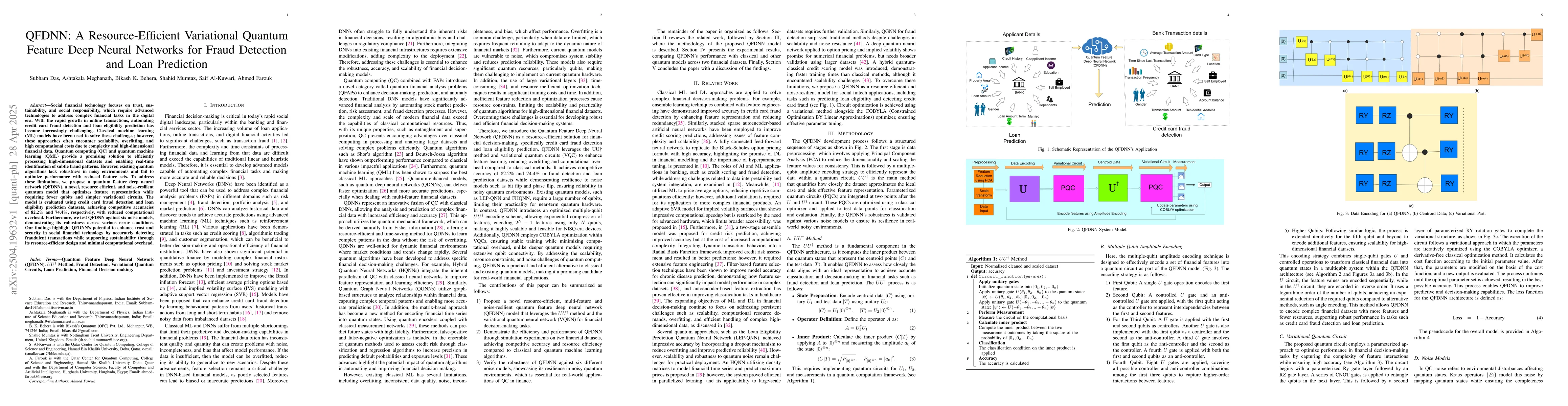

financial tasks in the digital era. With the rapid growth in online

transactions, automating credit card fraud detection and loan eligibility

prediction has become increasingly challenging. Classical machine learning (ML)

models have been used to solve these challenges; however, these approaches

often encounter scalability, overfitting, and high computational costs due to

complexity and high-dimensional financial data. Quantum computing (QC) and

quantum machine learning (QML) provide a promising solution to efficiently

processing high-dimensional datasets and enabling real-time identification of

subtle fraud patterns. However, existing quantum algorithms lack robustness in

noisy environments and fail to optimize performance with reduced feature sets.

To address these limitations, we propose a quantum feature deep neural network

(QFDNN), a novel, resource efficient, and noise-resilient quantum model that

optimizes feature representation while requiring fewer qubits and simpler

variational circuits. The model is evaluated using credit card fraud detection

and loan eligibility prediction datasets, achieving competitive accuracies of

82.2% and 74.4%, respectively, with reduced computational overhead.

Furthermore, we test QFDNN against six noise models, demonstrating its

robustness across various error conditions. Our findings highlight QFDNN

potential to enhance trust and security in social financial technology by

accurately detecting fraudulent transactions while supporting sustainability

through its resource-efficient design and minimal computational overhead.

Discussion 0