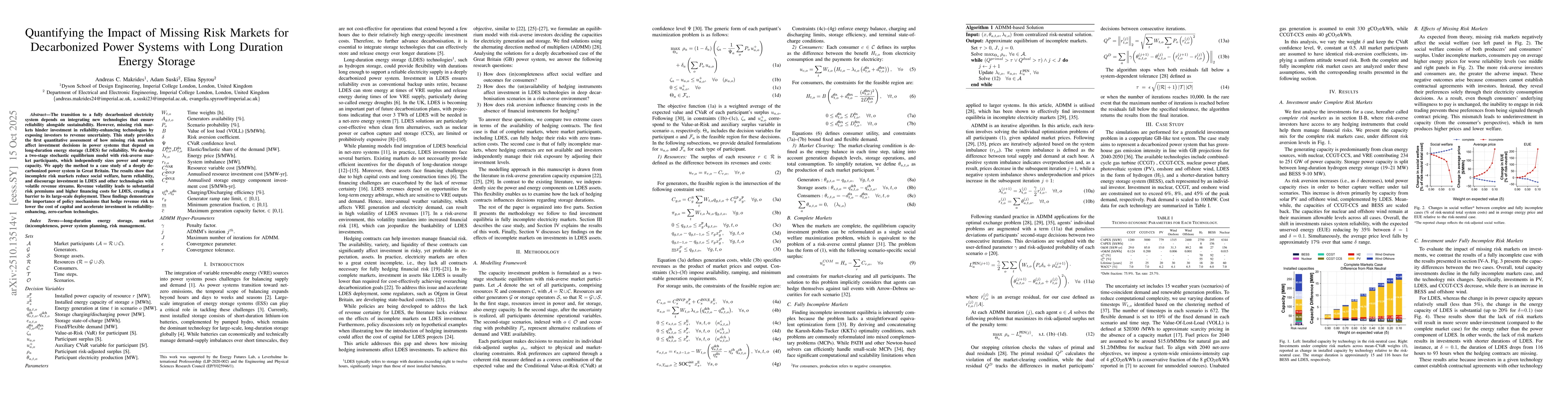

The transition to a fully decarbonised electricity system depends on

integrating new technologies that ensure reliability alongside sustainability.

However, missing risk markets hinder investment in reliability-enhancing

technologies by exposing investors to revenue uncertainty. This study provides

the first quantitative assessment of how missing risk markets affect investment

decisions in power systems that depend on long-duration energy storage (LDES)

for reliability. We develop a two-stage stochastic equilibrium model with

risk-averse market participants, which independently sizes power and energy

capacity. We apply the method to a case study of a deeply decarbonised power

system in Great Britain. The results show that incomplete risk markets reduce

social welfare, harm reliability, and discourage investment in LDES and other

technologies with volatile revenue streams. Revenue volatility leads to

substantial risk premiums and higher financing costs for LDES, creating a

barrier to its large-scale deployment. These findings demonstrate the

importance of policy mechanisms that hedge revenue risk to lower the cost of

capital and accelerate investment in reliability-enhancing, zero-carbon

technologies

Discussion 0