Summary

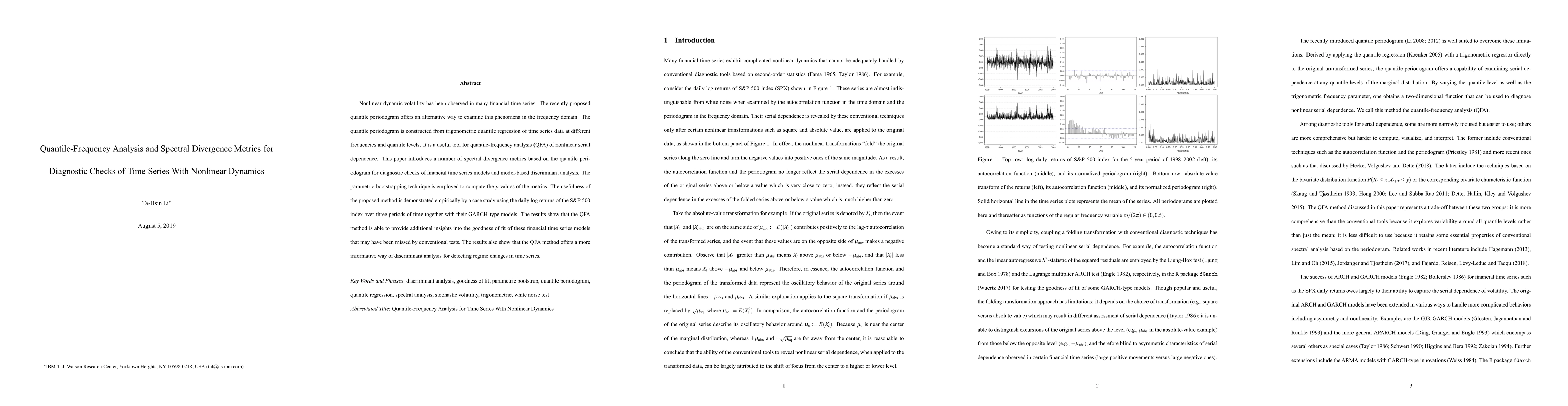

Nonlinear dynamic volatility has been observed in many financial time series. The recently proposed quantile periodogram offers an alternative way to examine this phenomena in the frequency domain. The quantile periodogram is constructed from trigonometric quantile regression of time series data at different frequencies and quantile levels. It is a useful tool for quantile-frequency analysis (QFA) of nonlinear serial dependence. This paper introduces a number of spectral divergence metrics based on the quantile periodogram for diagnostic checks of financial time series models and model-based discriminant analysis. The parametric bootstrapping technique is employed to compute the $p$-values of the metrics. The usefulness of the proposed method is demonstrated empirically by a case study using the daily log returns of the S\&P 500 index over three periods of time together with their GARCH-type models. The results show that the QFA method is able to provide additional insights into the goodness of fit of these financial time series models that may have been missed by conventional tests. The results also show that the QFA method offers a more informative way of discriminant analysis for detecting regime changes in time series.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, and significance.

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papersMultilayer Quantile Graph for Multivariate Time Series Analysis and Dimensionality Reduction

Pedro Ribeiro, Vanessa Freitas Silva, Maria Eduarda Silva et al.

| Title | Authors | Year | Actions |

|---|

Comments (0)