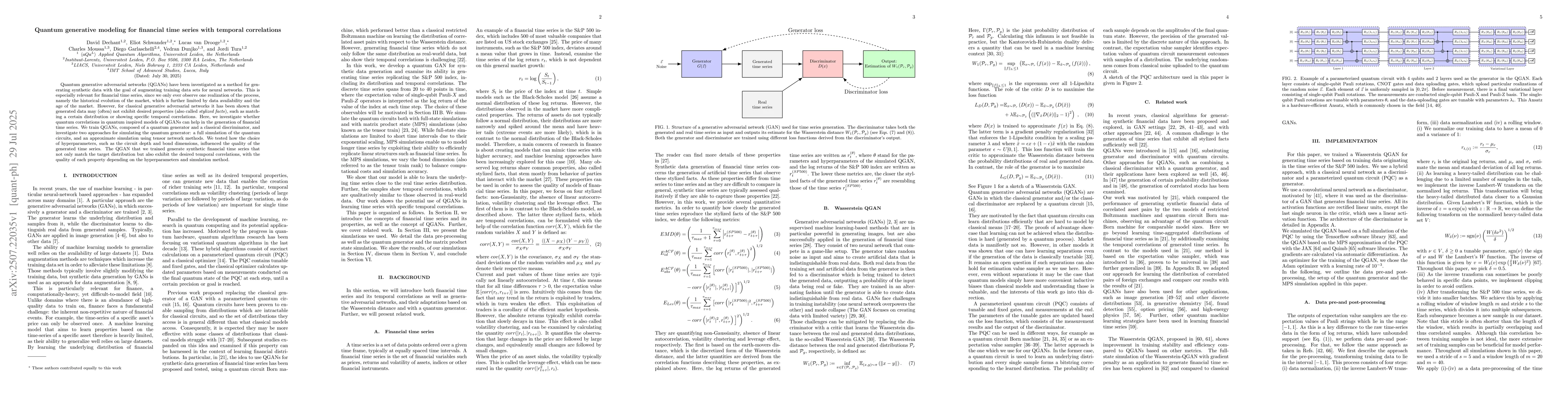

Quantum generative adversarial networks (QGANs) have been investigated as a

method for generating synthetic data with the goal of augmenting training data

sets for neural networks. This is especially relevant for financial time

series, since we only ever observe one realization of the process, namely the

historical evolution of the market, which is further limited by data

availability and the age of the market. However, for classical generative

adversarial networks it has been shown that generated data may (often) not

exhibit desired properties (also called stylized facts), such as matching a

certain distribution or showing specific temporal correlations. Here, we

investigate whether quantum correlations in quantum inspired models of QGANs

can help in the generation of financial time series. We train QGANs, composed

of a quantum generator and a classical discriminator, and investigate two

approaches for simulating the quantum generator: a full simulation of the

quantum circuits, and an approximate simulation using tensor network methods.

We tested how the choice of hyperparameters, such as the circuit depth and bond

dimensions, influenced the quality of the generated time series. The QGAN that

we trained generate synthetic financial time series that not only match the

target distribution but also exhibit the desired temporal correlations, with

the quality of each property depending on the hyperparameters and simulation

method.

Discussion 0