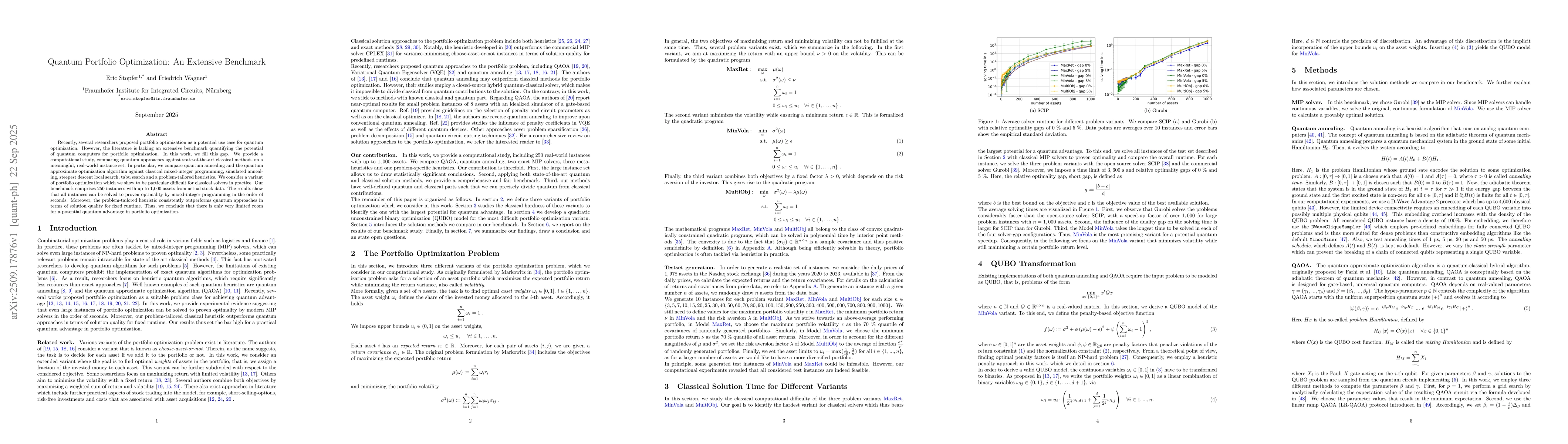

Recently, several researchers proposed portfolio optimization as a potential

use case for quantum optimization. However, the literature is lacking an

extensive benchmark quantifying the potential of quantum computers for

portfolio optimization. In this work, we fill this gap. We provide a

computational study, comparing quantum approaches against state-of-the-art

classical methods on a meaningful, real-world instance set. In particular, we

compare quantum annealing and the quantum approximate optimization algorithm

against classical mixed-integer programming, simulated annealing, steepest

descent local search, tabu search and a problem-tailored heuristics. We

consider a variant of portfolio optimization which we show to be particular

difficult for classical solvers in practice. Our benchmark comprises 250

instances with up to 1,000 assets from actual stock data. The results show that

all instances can be solved to proven optimality by mixed-integer programming

in the order of seconds. Moreover, the problem-tailored heuristic consistently

outperforms quantum approaches in terms of solution quality for fixed runtime.

Thus, we conclude that there is only very limited room for a potential quantum

advantage in portfolio optimization.

Discussion 0