R-estimators in GARCH models; asymptotics, applications and bootstrapping

Publication

Metrics

AI Quick Summary

A new class of estimators called R-estimators for GARCH models offers improved performance with asymptotic normality under stronger assumptions on error distributions. The estimators outperform traditional methods through fast algorithms and weighted bootstrap approximations.

Paper Preview

Abstract

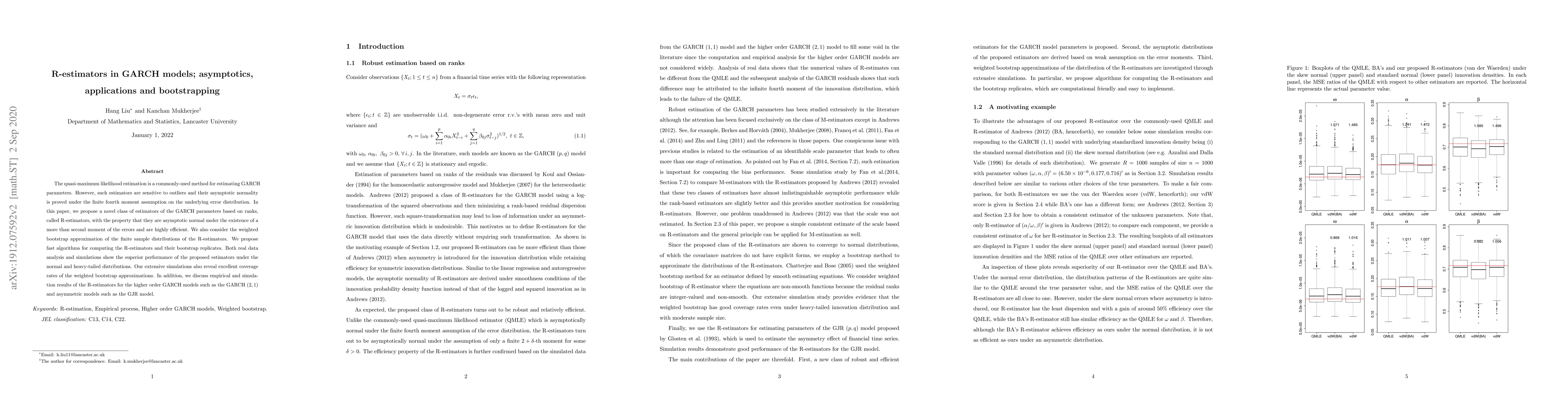

The quasi-maximum likelihood estimation is a commonly-used method for estimating GARCH parameters. However, such estimators are sensitive to outliers and their asymptotic normality is proved under the finite fourth moment assumption on the underlying error distribution. In this paper, we propose a novel class of estimators of the GARCH parameters based on ranks, called R-estimators, with the property that they are asymptotic normal under the existence of a more than second moment of the errors and are highly efficient. We also consider the weighted bootstrap approximation of the finite sample distributions of the R-estimators. We propose fast algorithms for computing the R-estimators and their bootstrap replicates. Both real data analysis and simulations show the superior performance of the proposed estimators under the normal and heavy-tailed distributions. Our extensive simulations also reveal excellent coverage rates of the weighted bootstrap approximations. In addition, we discuss empirical and simulation results of the R-estimators for the higher order GARCH models such as the GARCH~($2, 1$) and asymmetric models such as the GJR model.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0