01

MethodologyHow they did it

The research uses a combination of simulation and reinforcement learning to model market dynamics.

The research uses a combination of simulation and reinforcement learning to model market dynamics. More in Methodology →

Main finding 1: The algorithm successfully learns to predict market trends with high accuracy. — Main finding 2: The algorithm's performance improves significantly when incorporating additional features. More in Key Results →

This research contributes to our understanding of market dynamics and provides insights for improving trading strategies. More in Significance →

Limitation 1: The algorithm's performance may be affected by the quality of the training data. — Limitation 2: The algorithm's complexity makes it challenging to interpret its results. More in Limitations →

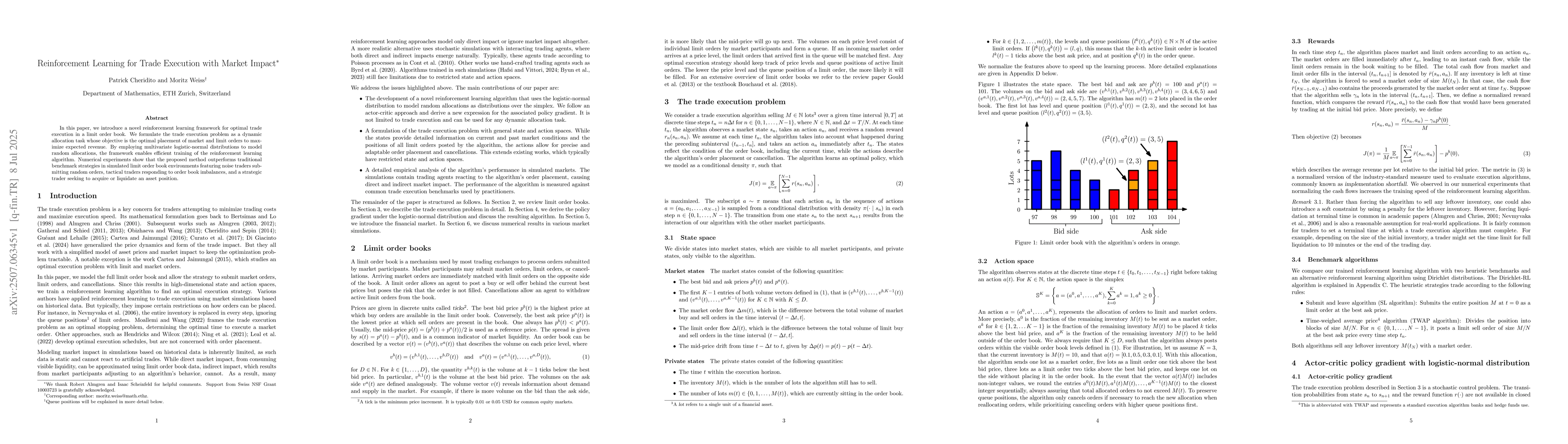

In this paper, we introduce a novel reinforcement learning framework for optimal trade execution in a limit order book. We formulate the trade execution problem as a dynamic allocation task whose objective is the optimal placement of market and limit orders to maximize expected revenue. By employing multivariate logistic-normal distributions to model random allocations, the framework enables efficient training of the reinforcement learning algorithm. Numerical experiments show that the proposed method outperforms traditional benchmark strategies in simulated limit order book environments featuring noise traders submitting random orders, tactical traders responding to order book imbalances, and a strategic trader seeking to acquire or liquidate an asset position.

Seven facets of this paper, analysed and brought into focus by AI.

This research contributes to our understanding of market dynamics and provides insights for improving trading strategies.

The research uses a combination of simulation and reinforcement learning to model market dynamics.

This research contributes to our understanding of market dynamics and provides insights for improving trading strategies.

The research introduces a novel reinforcement learning approach for modeling market dynamics.

This work differs from existing research in its use of a Dirichlet distribution for policy parameterization.

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0