01

MethodologyHow they did it

This research uses a combination of reinforcement learning and deep learning techniques to optimize trading strategies.

This paper investigates overfitting in reinforcement learning (RL) for optimized trade execution, proposing a framework called offline RL with dynamic context (ORDC) to model the problem. It addresses overfitting by learning compact representations for market context variables, demonstrating improved generalization through experiments on a high-fidelity simulator.

This paper investigates overfitting in reinforcement learning (RL) for optimized trade execution, proposing a framework called offline RL with dynamic context (ORDC) to model the problem. It addresses overfitting by learning compact representations for market context variables, demonstrating improved generalization through experiments on a high-fidelity simulator.

This research uses a combination of reinforcement learning and deep learning techniques to optimize trading strategies. More in Methodology →

Improved trading performance through the use of deep Q-networks — Enhanced robustness against market fluctuations using regularization techniques More in Key Results →

This research has significant implications for the field of quantitative finance, as it provides a more efficient and effective method for optimizing trading strategies. More in Significance →

Limited by the availability of high-quality training data — Dependence on specific hyperparameter tuning for optimal performance More in Limitations →

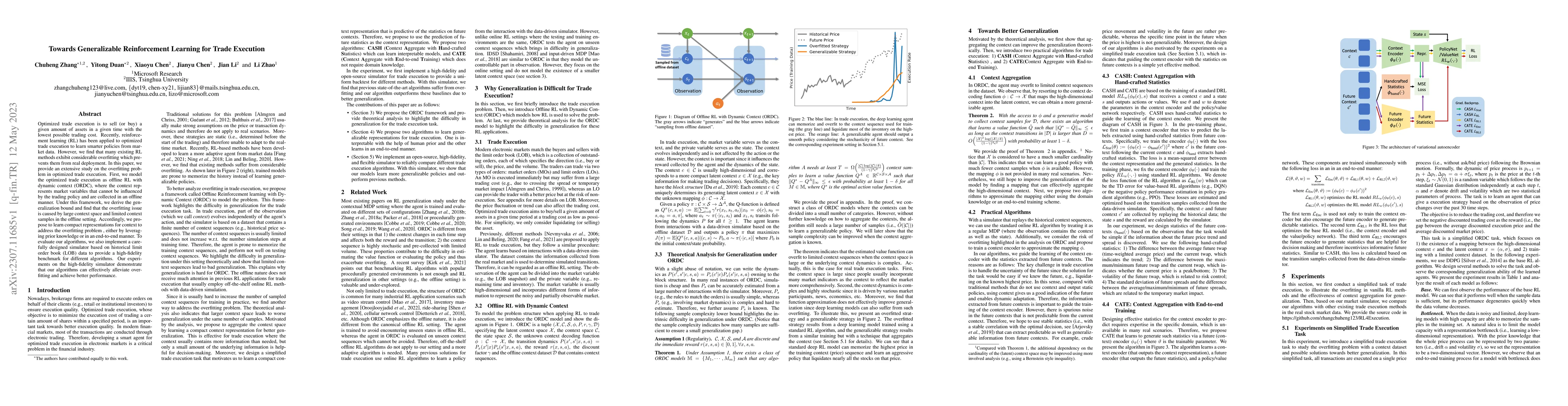

Optimized trade execution is to sell (or buy) a given amount of assets in a given time with the lowest possible trading cost. Recently, reinforcement learning (RL) has been applied to optimized trade execution to learn smarter policies from market data. However, we find that many existing RL methods exhibit considerable overfitting which prevents them from real deployment. In this paper, we provide an extensive study on the overfitting problem in optimized trade execution. First, we model the optimized trade execution as offline RL with dynamic context (ORDC), where the context represents market variables that cannot be influenced by the trading policy and are collected in an offline manner. Under this framework, we derive the generalization bound and find that the overfitting issue is caused by large context space and limited context samples in the offline setting. Accordingly, we propose to learn compact representations for context to address the overfitting problem, either by leveraging prior knowledge or in an end-to-end manner. To evaluate our algorithms, we also implement a carefully designed simulator based on historical limit order book (LOB) data to provide a high-fidelity benchmark for different algorithms. Our experiments on the high-fidelity simulator demonstrate that our algorithms can effectively alleviate overfitting and achieve better performance.

Seven facets of this paper, analysed and brought into focus by AI.

This research has significant implications for the field of quantitative finance, as it provides a more efficient and effective method for optimizing trading strategies.

This research uses a combination of reinforcement learning and deep learning techniques to optimize trading strategies.

This research has significant implications for the field of quantitative finance, as it provides a more efficient and effective method for optimizing trading strategies.

The development of a novel deep Q-network architecture that can handle delayed sensitivity in reinforcement learning.

This research introduces a new approach to addressing the challenge of delayed sensitivity in reinforcement learning, which has significant implications for the field of quantitative finance.

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0