Yitong Duan

9 papers on arXiv

Academic Profile

Statistics

Similar Authors

Papers on arXiv

Towards Generalizable Reinforcement Learning for Trade Execution

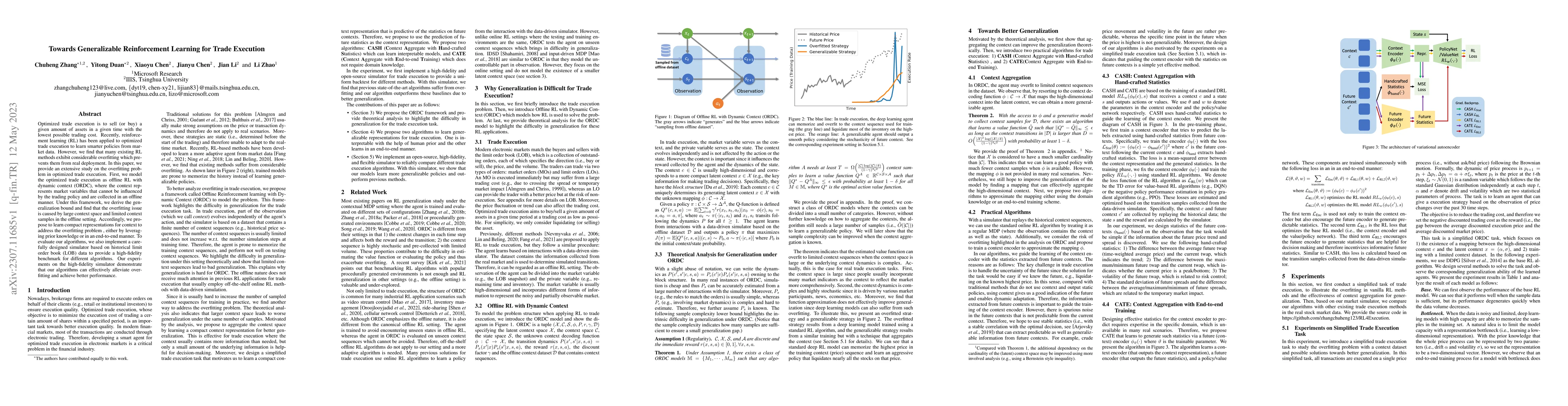

Optimized trade execution is to sell (or buy) a given amount of assets in a given time with the lowest possible trading cost. Recently, reinforcement learning (RL) has been applied to optimized trad...

FactorGCL: A Hypergraph-Based Factor Model with Temporal Residual Contrastive Learning for Stock Returns Prediction

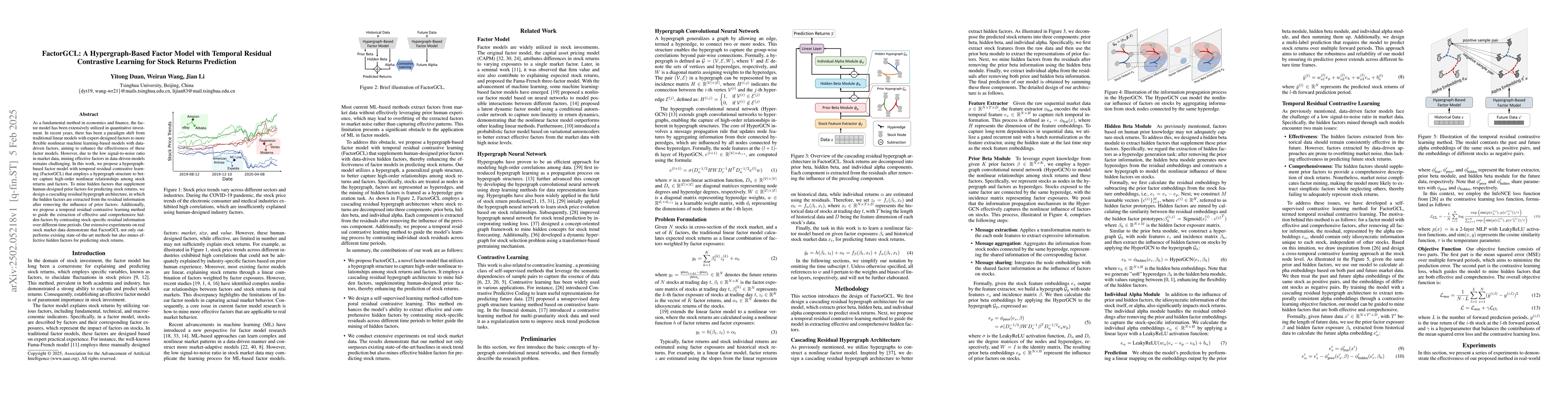

As a fundamental method in economics and finance, the factor model has been extensively utilized in quantitative investment. In recent years, there has been a paradigm shift from traditional linear mo...

No Free Lunch: Rethinking Internal Feedback for LLM Reasoning

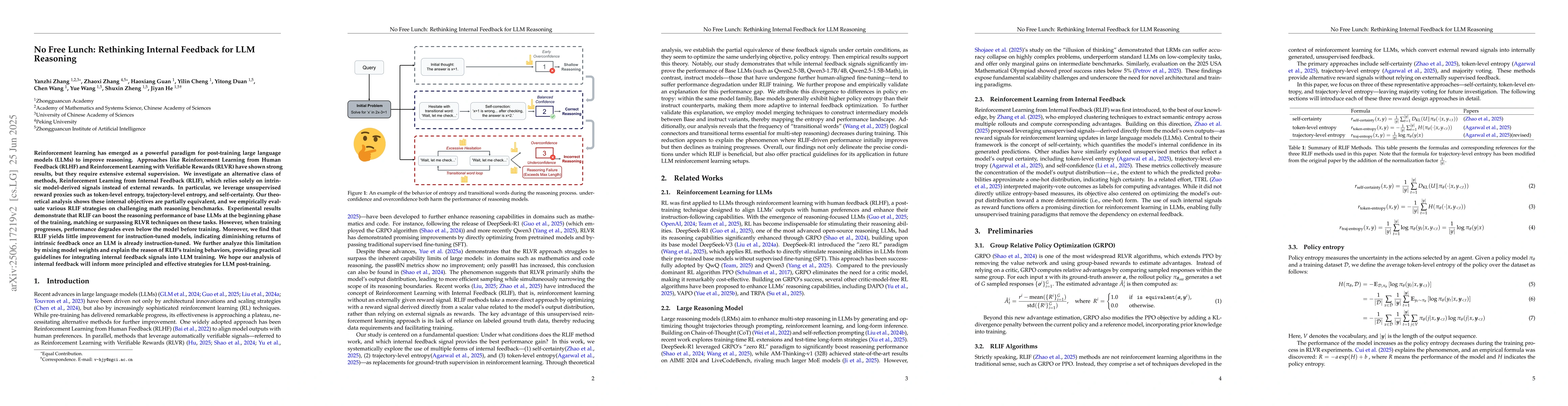

Reinforcement learning has emerged as a powerful paradigm for post-training large language models (LLMs) to improve reasoning. Approaches like Reinforcement Learning from Human Feedback (RLHF) and Rei...

Navigating the Alpha Jungle: An LLM-Powered MCTS Framework for Formulaic Factor Mining

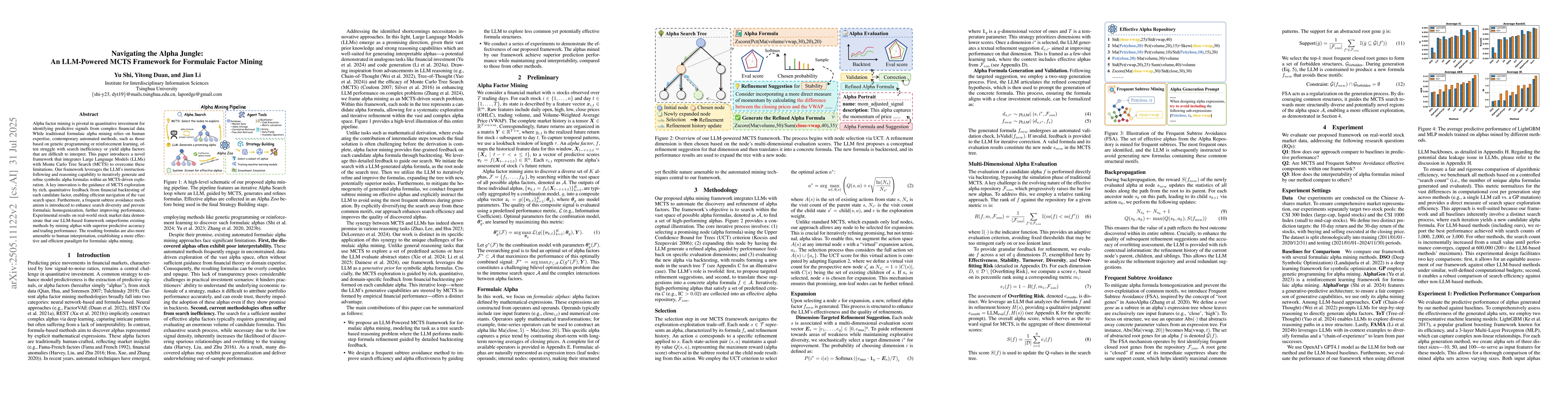

Alpha factor mining is pivotal in quantitative investment for identifying predictive signals from complex financial data. While traditional formulaic alpha mining relies on human expertise, contempora...

Population-Evolve: a Parallel Sampling and Evolutionary Method for LLM Math Reasoning

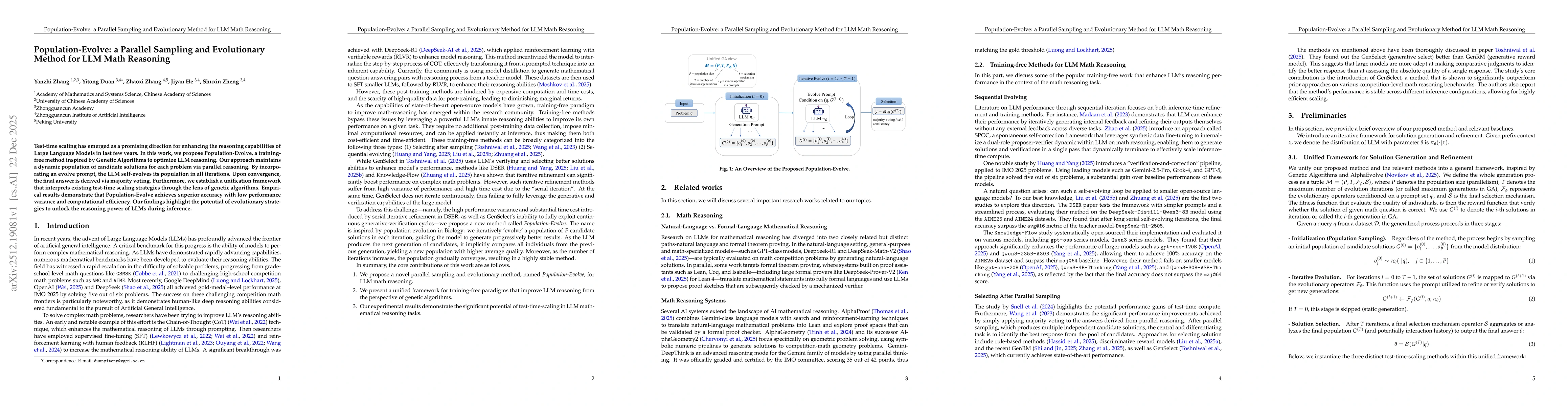

Test-time scaling has emerged as a promising direction for enhancing the reasoning capabilities of Large Language Models in last few years. In this work, we propose Population-Evolve, a training-free ...

One Tool Is Enough: Reinforcement Learning for Repository-Level LLM Agents

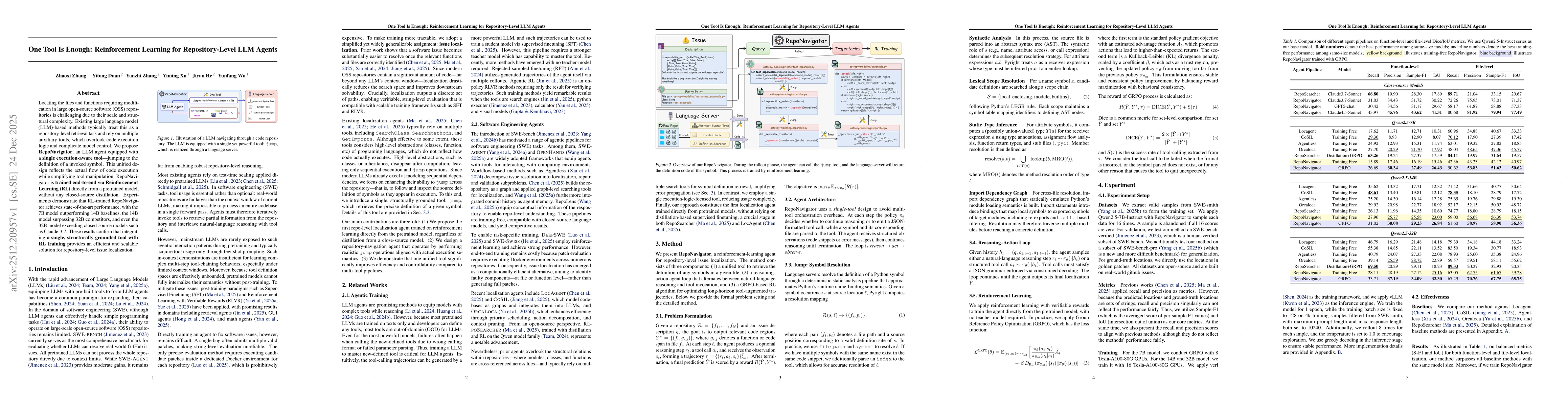

Locating the files and functions requiring modification in large open-source software (OSS) repositories is challenging due to their scale and structural complexity. Existing large language model (LLM...

The World Leaks the Future: Harness Evolution for Future Prediction Agents

Many consequential decisions must be made before the relevant outcome is known. Such problems are commonly framed as \emph{future prediction}, where an LLM agent must form a prediction for an unresolv...

FutureWorld: A Live Environment for Training Predictive Agents with Real-World Outcome Rewards

Live future prediction refers to the task of making predictions about real-world events before they unfold. This task is increasingly studied using large language model-based agent systems, and it is ...

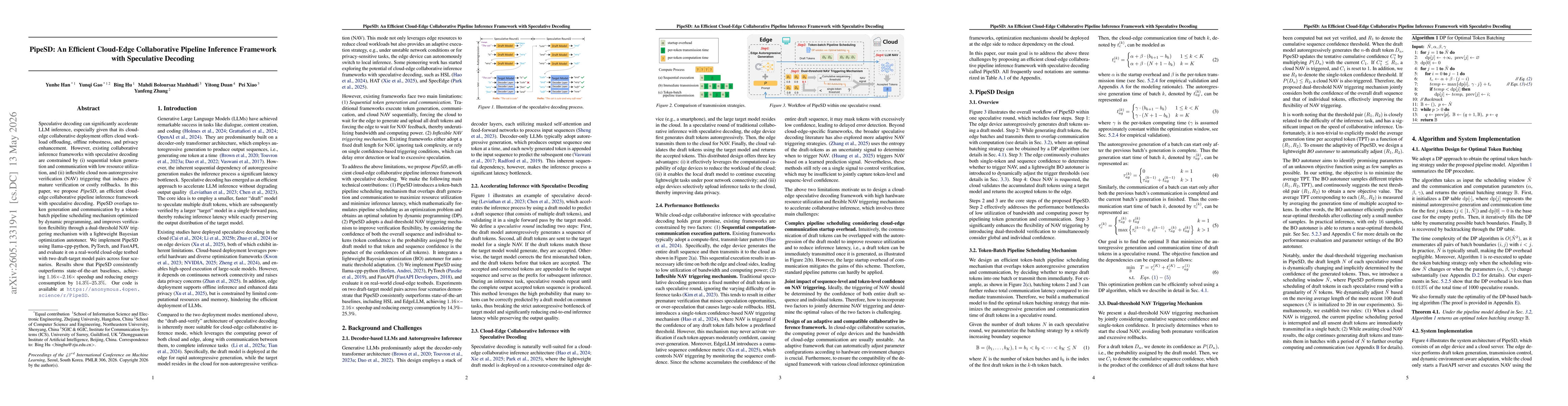

PipeSD: An Efficient Cloud-Edge Collaborative Pipeline Inference Framework with Speculative Decoding

Speculative decoding can significantly accelerate LLM inference, especially given that its cloud-edge collaborative deployment offers cloud workload offloading, offline robustness, and privacy enhance...