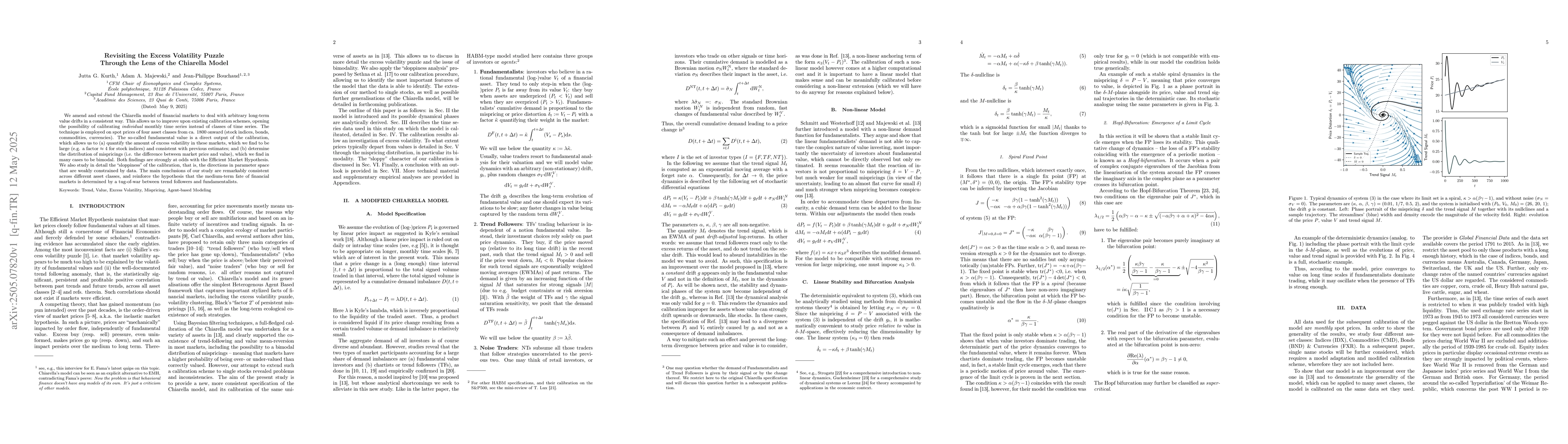

Summary

We amend and extend the Chiarella model of financial markets to deal with arbitrary long-term value drifts in a consistent way. This allows us to improve upon existing calibration schemes, opening the possibility of calibrating individual monthly time series instead of classes of time series. The technique is employed on spot prices of four asset classes from ca. 1800 onward (stock indices, bonds, commodities, currencies). The so-called fundamental value is a direct output of the calibration, which allows us to (a) quantify the amount of excess volatility in these markets, which we find to be large (e.g. a factor $\approx$ 4 for stock indices) and consistent with previous estimates; and (b) determine the distribution of mispricings (i.e. the difference between market price and value), which we find in many cases to be bimodal. Both findings are strongly at odds with the Efficient Market Hypothesis. We also study in detail the 'sloppiness' of the calibration, that is, the directions in parameter space that are weakly constrained by data. The main conclusions of our study are remarkably consistent across different asset classes, and reinforce the hypothesis that the medium-term fate of financial markets is determined by a tug-of-war between trend followers and fundamentalists.

AI Key Findings

Generated Jun 08, 2025

Methodology

The Chiarella model is amended and extended to handle long-term value drifts consistently, enabling calibration of individual monthly time series for various asset classes including stock indices, bonds, commodities, and currencies.

Key Results

- Excess volatility found to be large (e.g., a factor ~4 for stock indices), consistent with previous estimates.

- Mispricing distribution revealed to be bimodal in many cases, contradicting the Efficient Market Hypothesis.

- Tug-of-war between trend followers and fundamentalists identified as a key determinant of medium-term market fate.

Significance

This research quantifies excess volatility and mispricing distribution across multiple asset classes, challenging the Efficient Market Hypothesis and providing insights into market dynamics driven by trend followers and fundamentalists.

Technical Contribution

Development of an improved calibration technique for the Chiarella model, allowing for individual time series calibration and direct computation of fundamental value.

Novelty

This work extends previous applications of the Chiarella model by enabling more precise calibration and providing novel insights into the bimodal distribution of mispricings across diverse asset classes.

Limitations

- The study does not address potential impacts of regulatory changes or structural market shifts over the long period analyzed (ca. 1800 onward).

- Calibration sloppiness, or weakly constrained parameter space directions, might introduce uncertainties in the findings.

Future Work

- Investigate the effects of regulatory changes and structural market shifts on the identified market dynamics.

- Explore the implications of the findings for portfolio management and risk assessment strategies.

Paper Details

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Similar Papers

Found 4 papers| Title | Authors | Year | Actions |

|---|

Comments (0)