Academic Profile

Statistics

Similar Authors

Papers on arXiv

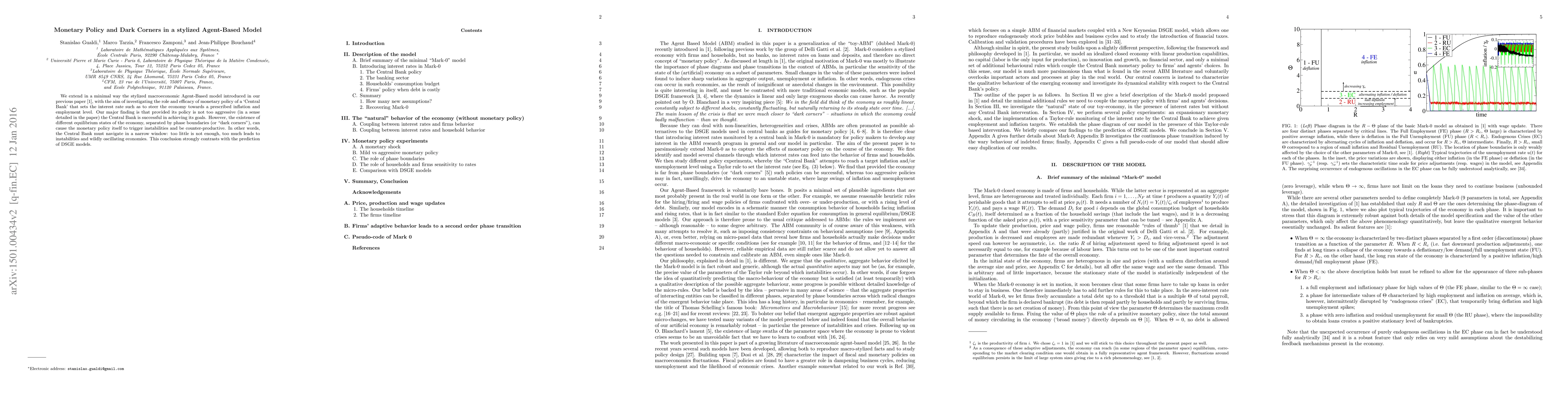

We extend in a minimal way the stylized model introduced in in "Tipping Points in Macroeconomic Agent Based Models" [JEDC 50, 29-61 (2015)], with the aim of investigating the role and efficacy of mo...

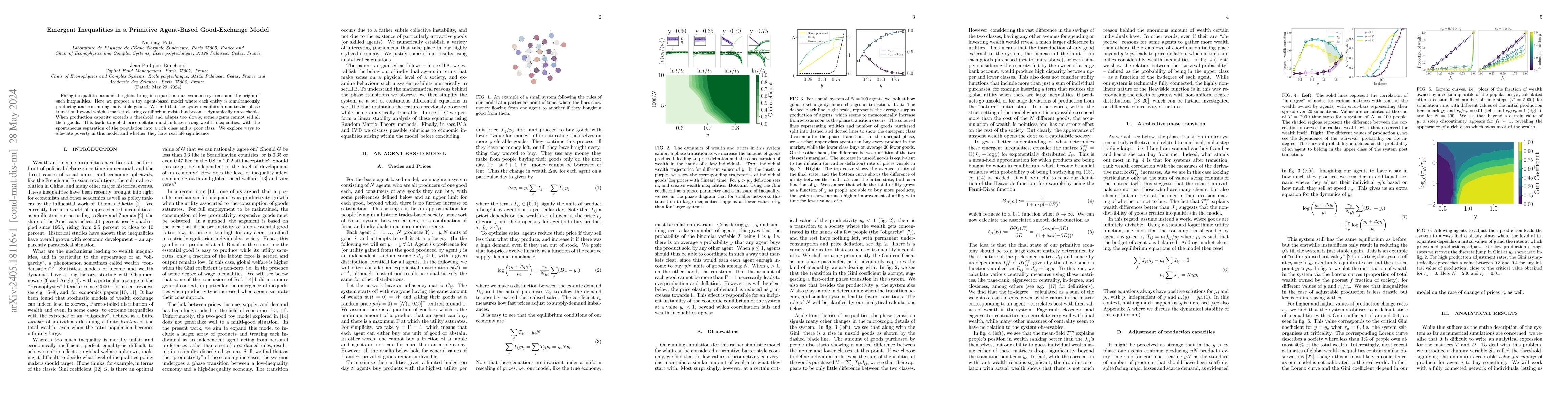

Rising inequalities around the globe bring into question our economic systems and the origin of such inequalities. Here we propose a toy agent-based model where each entity is simultaneously produci...

Many active funds hold concentrated portfolios. Flow-driven trading in these securities causes price pressure, which pushes up the funds' existing positions resulting in realized returns. We decompo...

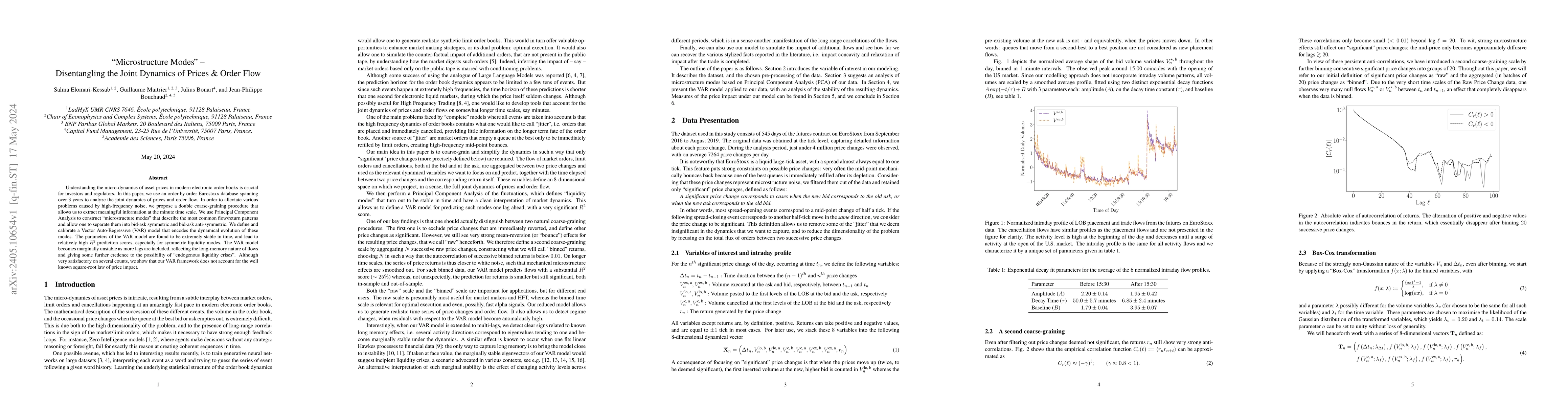

Understanding the micro-dynamics of asset prices in modern electronic order books is crucial for investors and regulators. In this paper, we use an order by order Eurostoxx database spanning over 3 ...

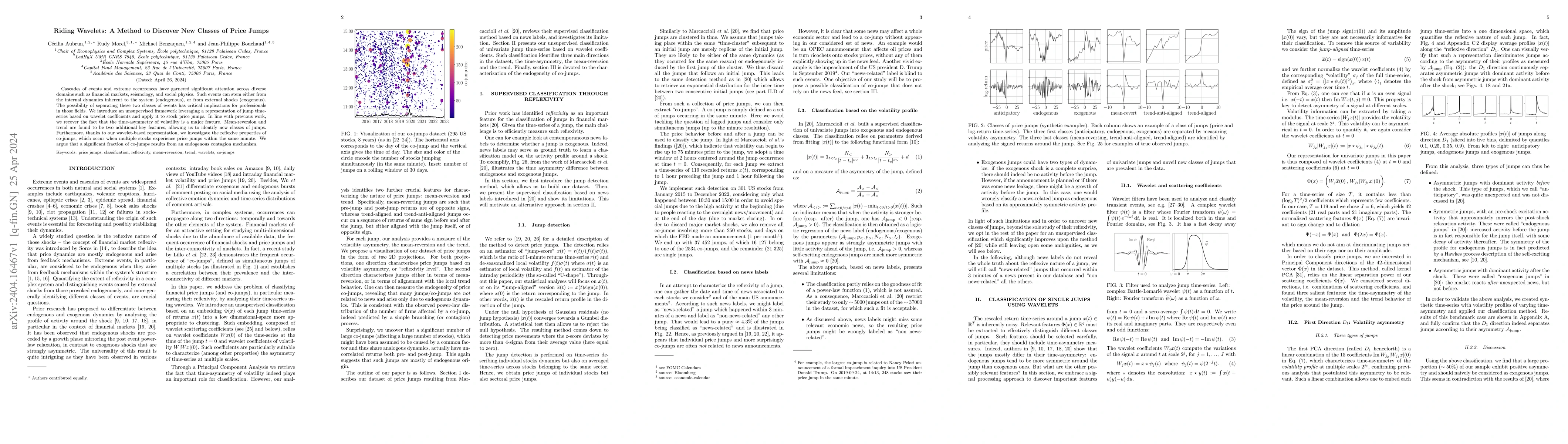

Cascades of events and extreme occurrences have garnered significant attention across diverse domains such as financial markets, seismology, and social physics. Such events can stem either from the ...

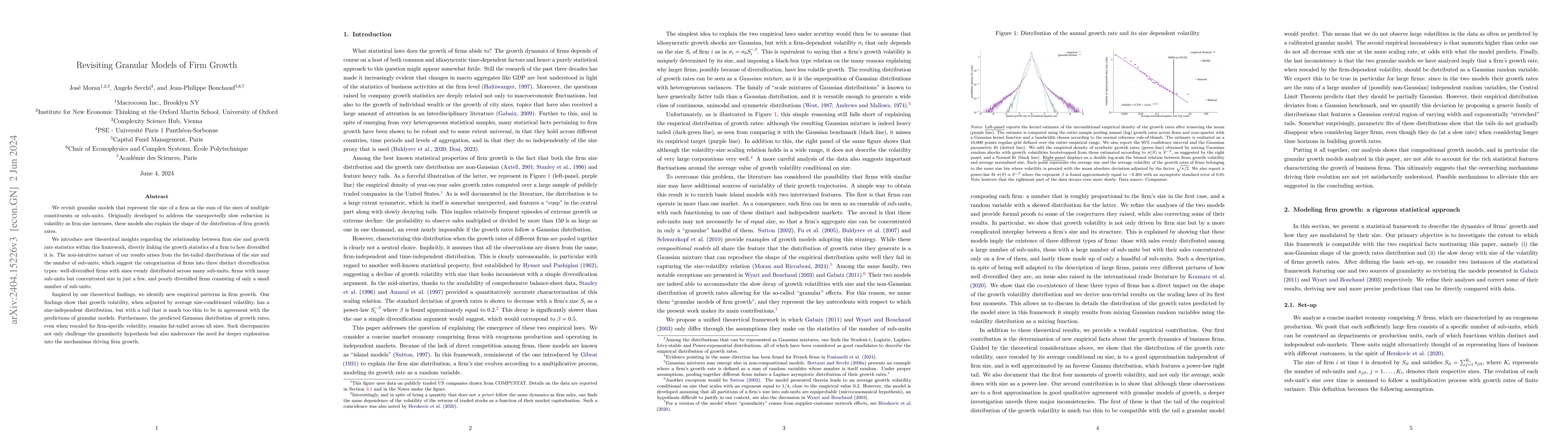

We revisit granular models that represent the size of a firm as the sum of the sizes of multiple constituents or sub-units. Originally developed to address the unexpectedly slow reduction in volatil...

Twenty five years ago, several authors proposed to model the forward interest rate curve (FRC) as an elastic string along which idiosyncratic shocks propagate, accounting for the peculiar structure ...

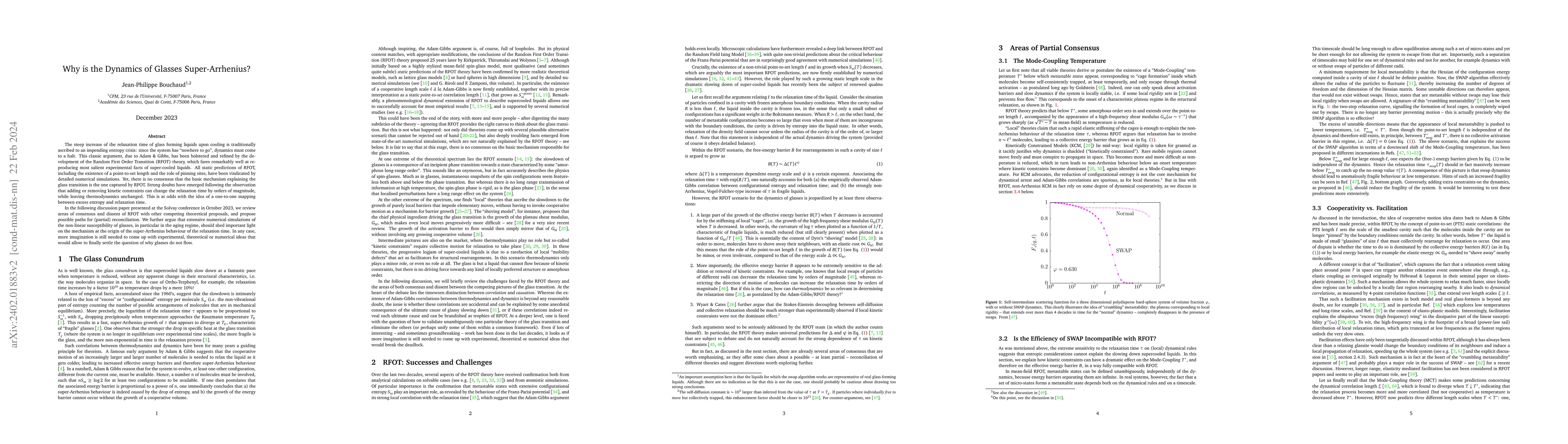

The steep increase of the relaxation time of glass forming liquids upon cooling is traditionally ascribed to an impending entropy crisis: since the system has "nowhere to go", dynamics must come to ...

As a schematic model of the complexity economic agents are confronted with, we introduce the ``SK-game'', a discrete time binary choice model inspired from mean-field spin-glasses. We show that even...

Economic and ecological models can be extremely complex, with a large number of agents/species each featuring multiple interacting dynamical quantities. In an attempt to understand the generic stabi...

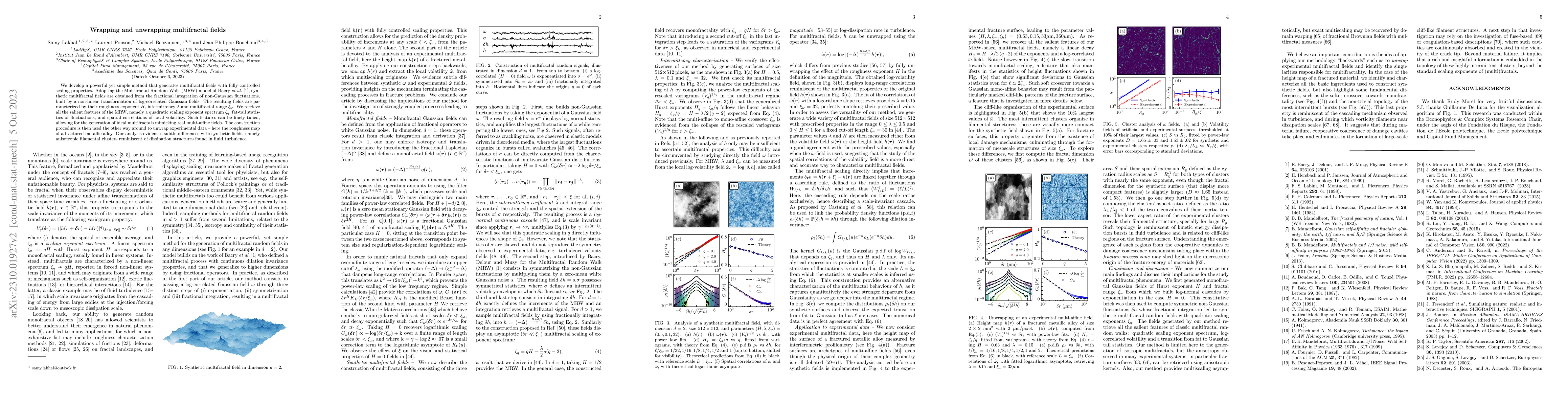

We develop a powerful yet simple method that generates multifractal fields with fully controlled scaling properties. Adopting the Multifractal Random Walk (MRW) model of Bacry et al. (2001), synthet...

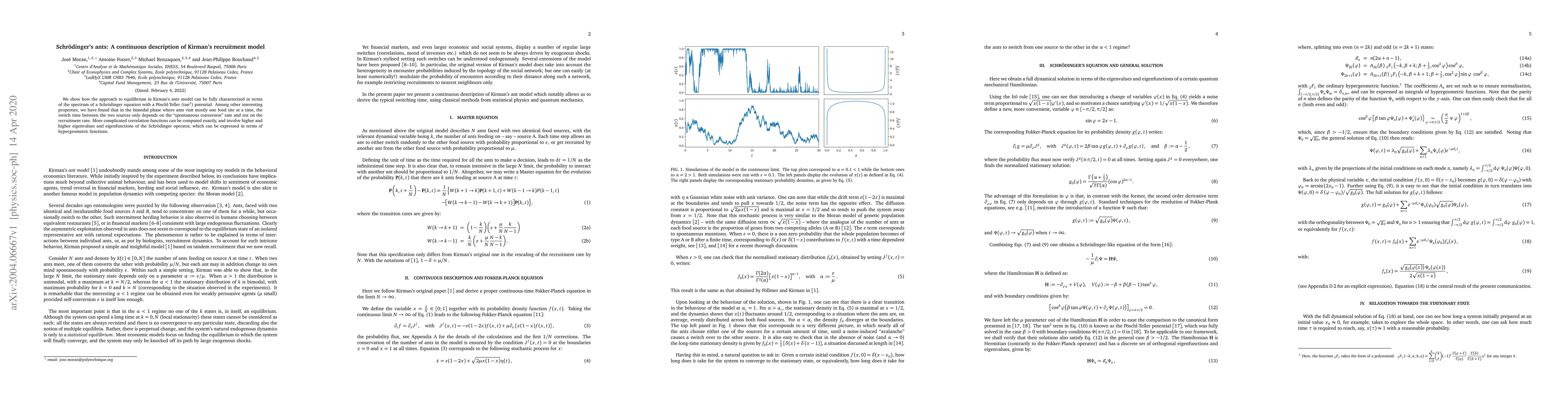

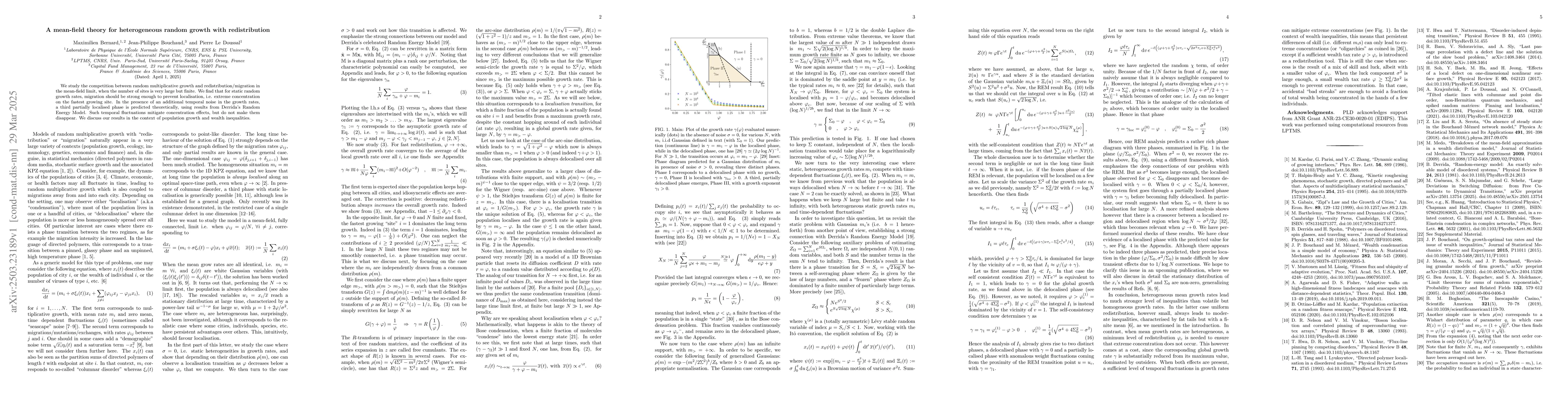

In complex systems, external parameters often determine the phase in which the system operates, i.e., its macroscopic behavior. For nearly a century, statistical physics has extensively studied syst...

This is the English version of my inaugural lecture at Coll\`ege de France in 2021, available at https://www.youtube.com/watch?v=bxktplKMhKU. I reflect on the difficulty of multi-disciplinary resear...

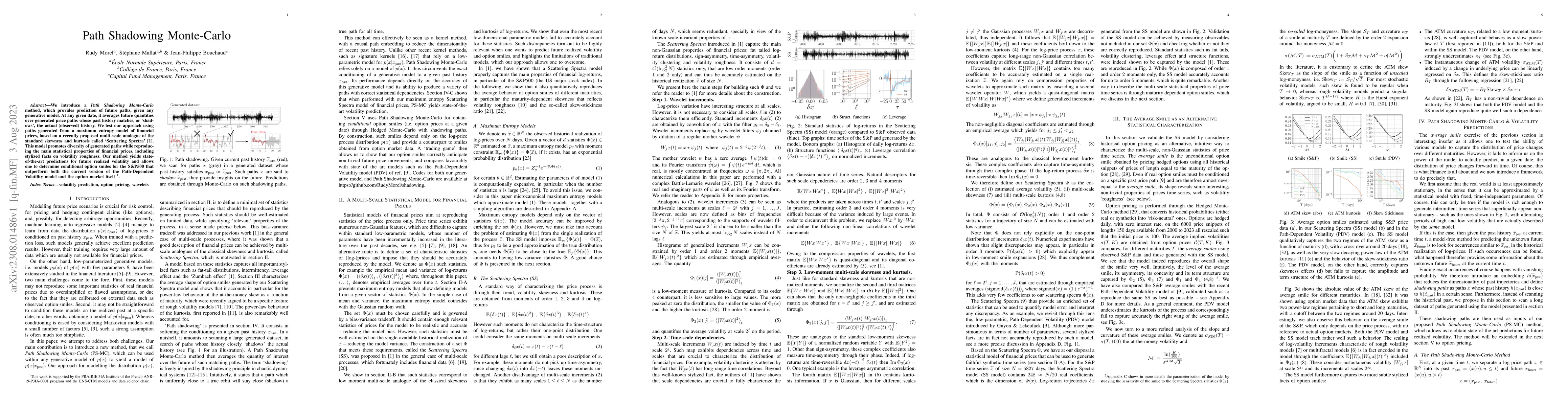

We introduce a Path Shadowing Monte-Carlo method, which provides prediction of future paths, given any generative model. At any given date, it averages future quantities over generated price paths w...

Classical economics has developed an arsenal of methods, based on the idea of representative agents, to come up with precise numbers for next year's GDP, inflation and exchange rates, among (many) o...

The economic shocks that followed the COVID-19 pandemic have brought to light the difficulty, both for academics and policy makers, of describing and predicting the dynamics of inflation. This paper...

Portfolio managers' orders trade off return and trading cost predictions. Return predictions rely on alpha models, whereas price impact models quantify trading costs. This paper studies what happens...

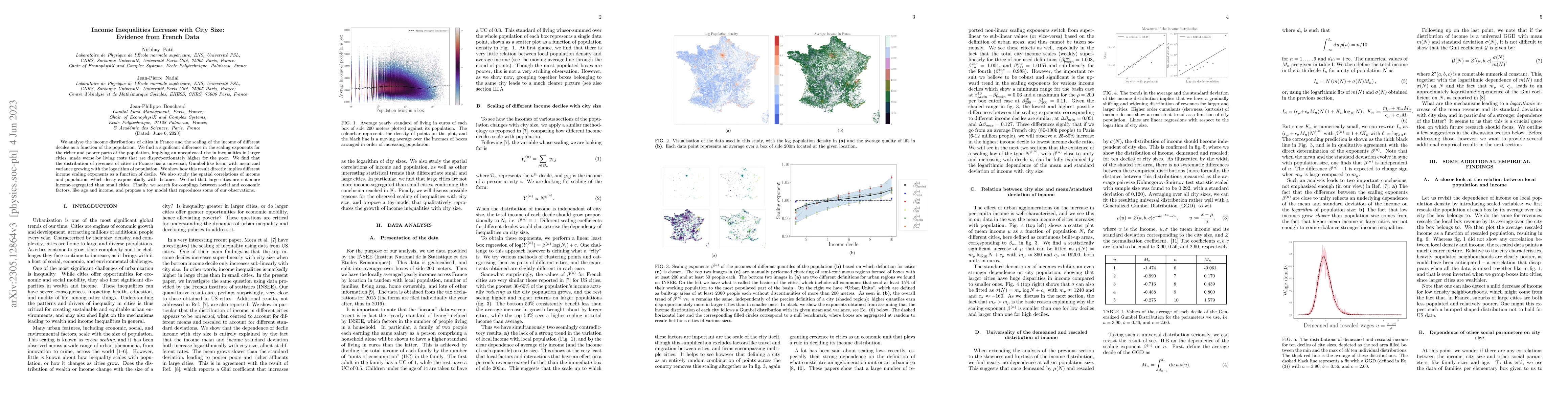

We analyse the income distributions of cities in France and the scaling of the income of different deciles as a function of the population. We find a significant difference in the scaling exponents ...

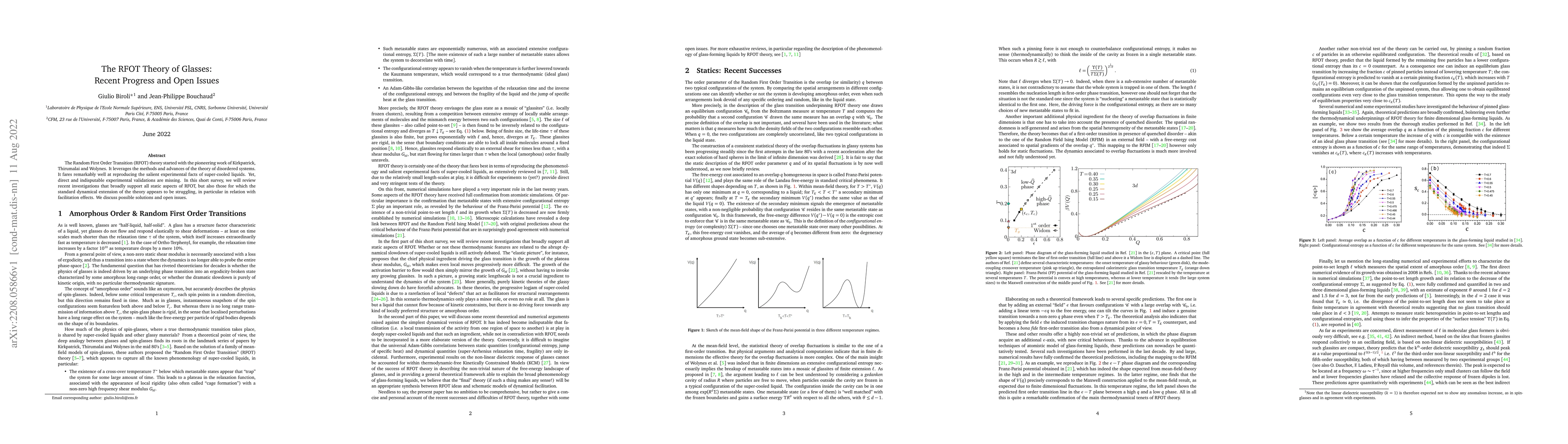

The Random First Order Transition (RFOT) theory started with the pioneering work of Kirkpatrick, Thirumalai and Wolynes. It leverages the methods and advances of the theory of disordered systems. It...

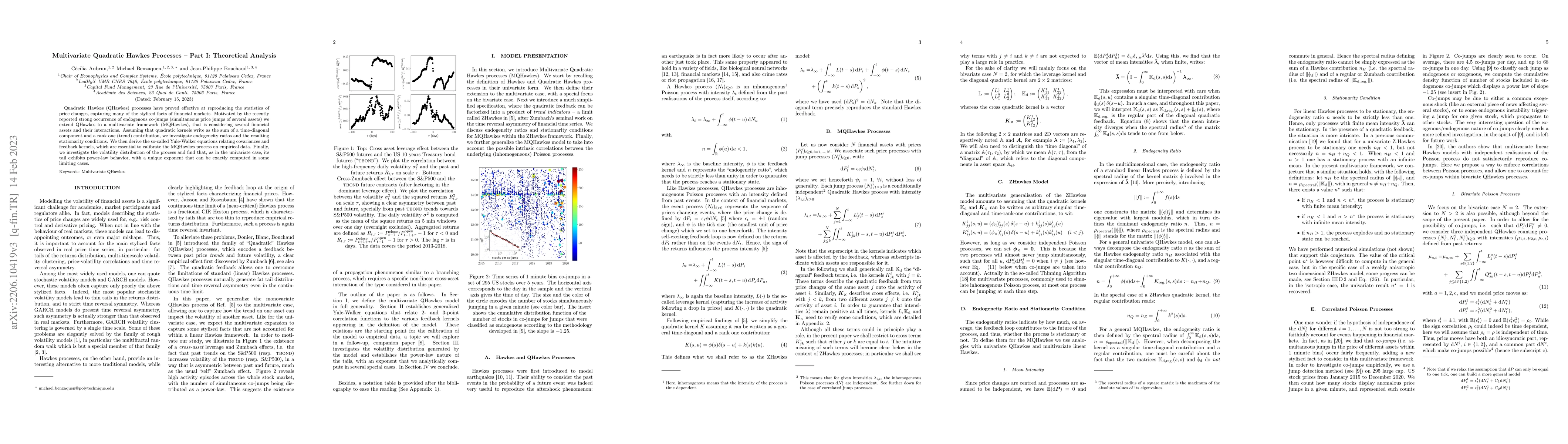

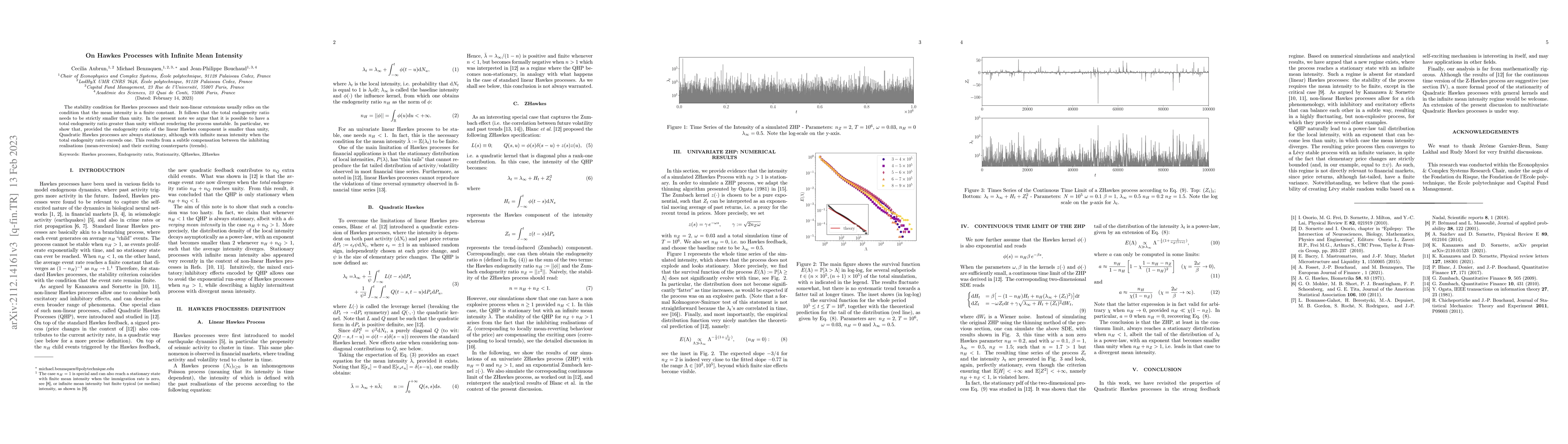

Quadratic Hawkes (QHawkes) processes have proved effective at reproducing the statistics of price changes, capturing many of the stylised facts of financial markets. Motivated by the recently report...

The Slutsky equation, central in consumer choice theory, is derived from the usual hypotheses underlying most standard models in Economics, such as full rationality, homogeneity, and absence of inte...

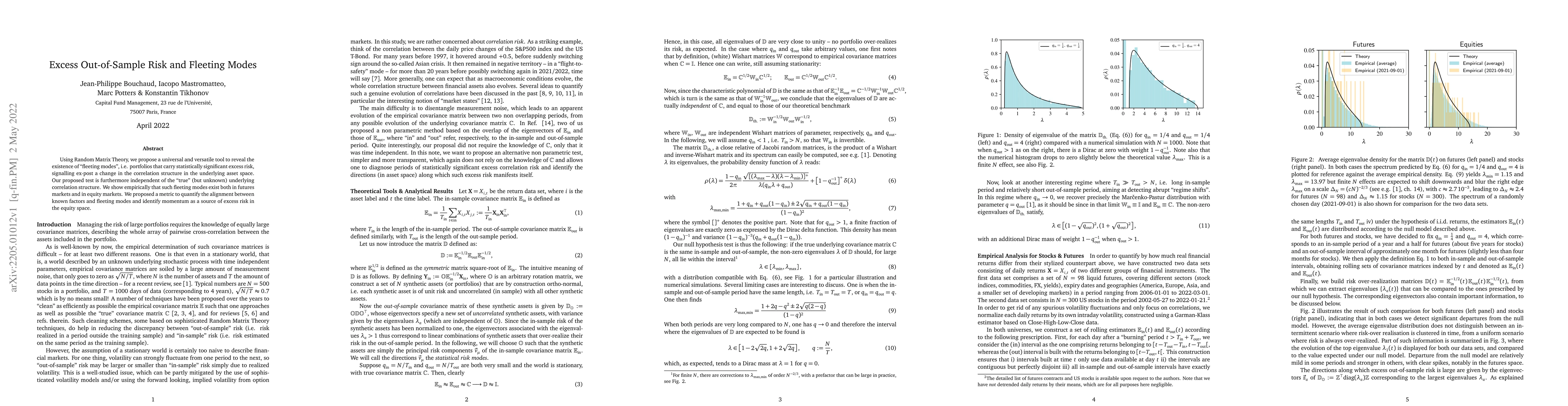

Using Random Matrix Theory, we propose a universal and versatile tool to reveal the existence of "fleeting modes", i.e. portfolios that carry statistically significant excess risk, signalling ex-pos...

A semi-Markov process is one that changes states in accordance with a Markov chain but takes a random amount of time between changes. We consider the generalisation to semi-Markov processes of the c...

We introduce the wavelet scattering spectra which provide non-Gaussian models of time-series having stationary increments. A complex wavelet transform computes signal variations at each scale. Depen...

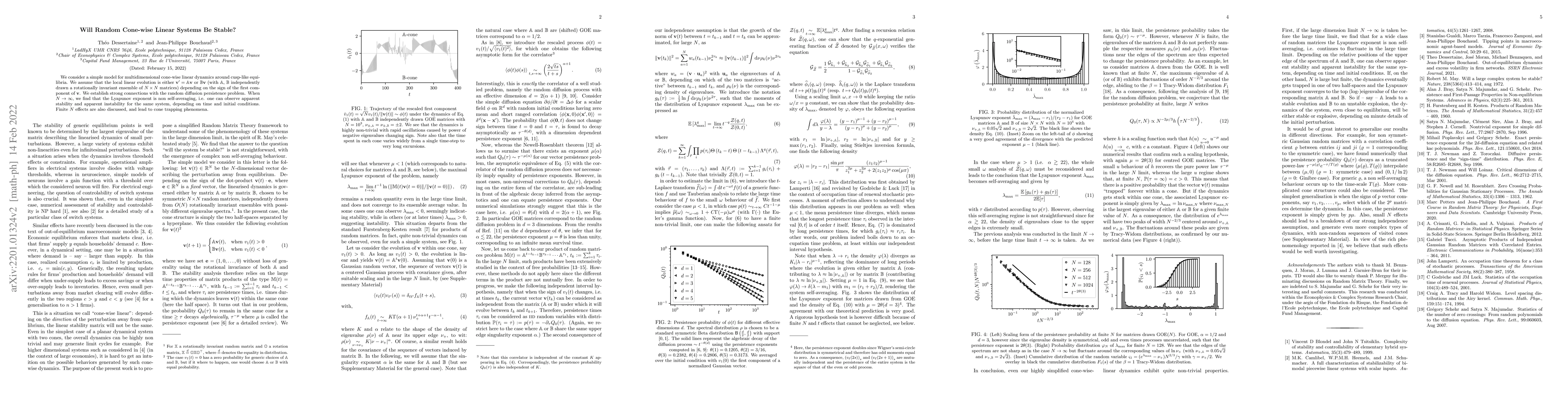

We consider a simple model for multidimensional cone-wise linear dynamics around cusp-like equilibria. We assume that the local linear evolution is either $\mathbf{v}^\prime=\mathbb{A}\mathbf{v}$ or...

The stability condition for Hawkes processes and their non-linear extensions usually relies on the condition that the mean intensity is a finite constant. It follows that the total endogeneity ratio...

Agent-Based Models (ABM) are computational scenario-generators, which can be used to predict the possible future outcomes of the complex system they represent. To better understand the robustness of...

In the General Theory, Keynes remarked that the economy's state depends on expectations, and that these expectations can be subject to sudden swings. In this work, we develop a multiple equilibria b...

We attempt to reconcile Gabaix and Koijen's (GK) recent Inelastic Market Hypothesis (IMH) with the order-driven view of markets that emerged within the microstructure literature in the past 20 years...

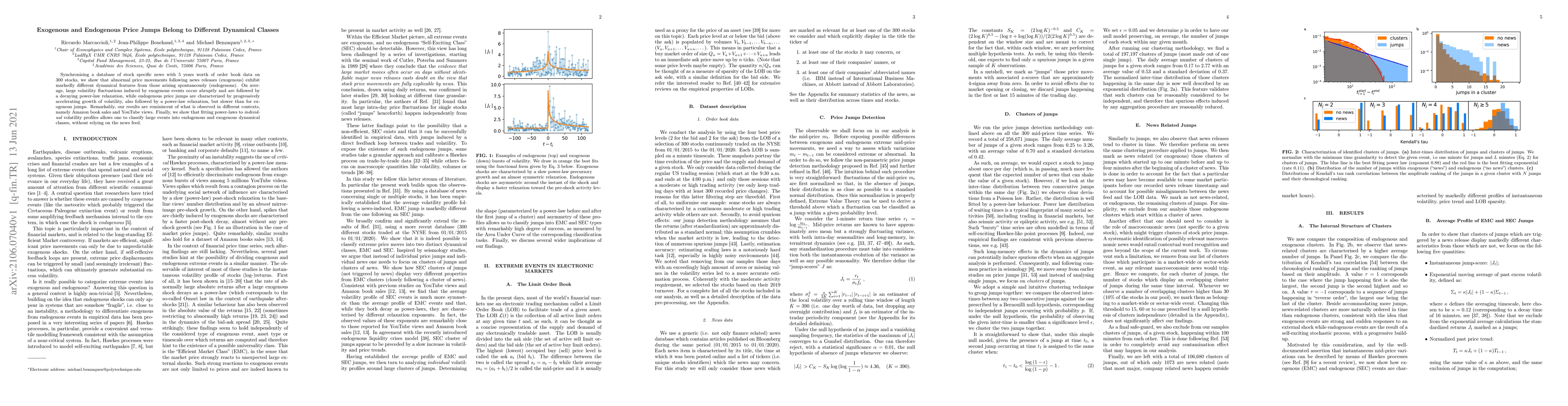

Synchronising a database of stock specific news with 5 years worth of order book data on 300 stocks, we show that abnormal price movements following news releases (exogenous) exhibit markedly differ...

We consider the classical problem of optimal portfolio construction with the constraint that no short position is allowed, or equivalently the valid equilibria of multispecies Lotka-Volterra equatio...

This is an informal and sketchy review of six topical, somewhat unrelated subjects in quantitative finance: rough volatility models; random covariance matrix theory; copulas; crowded trades; high-fr...

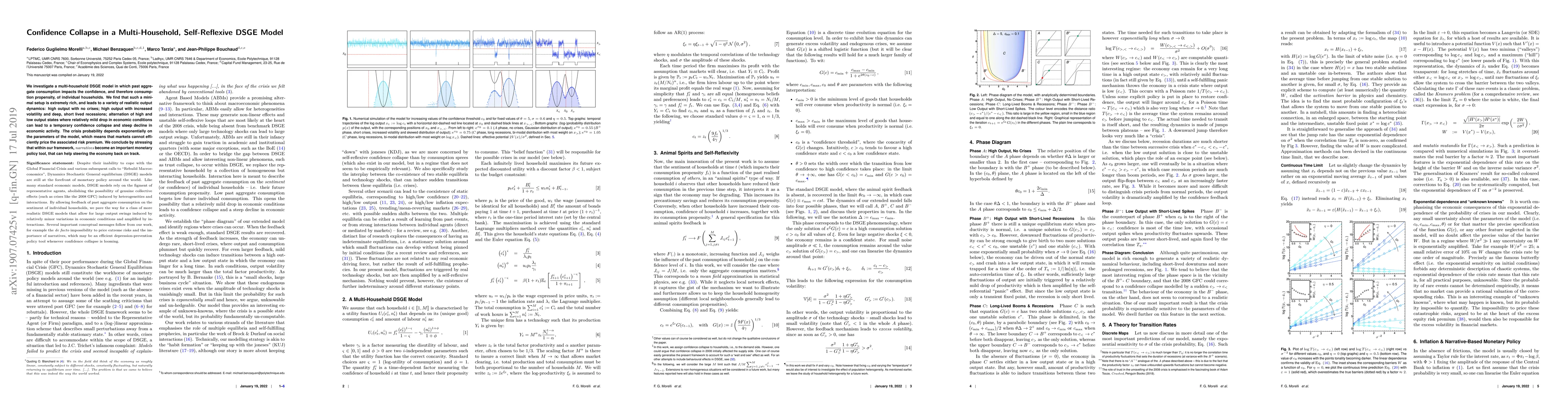

We study a self-reflexive DSGE model with heterogeneous households, aimed at characterising the impact of economic recessions on the different strata of the society. Our framework allows to analyse ...

We review 15 years of theoretical and experimental work on the non-linear response of glassy systems. We argue that an anomalous growth of the peak value of non-linear susceptibilities is a signatur...

The ability to learn from others (social learning) is often deemed a cause of human species success. But if social learning is indeed more efficient (whether less costly or more accurate) than indiv...

We construct a model of an exchange economy in which agents trade assets contingent on an observable signal, the probability of which depends on public opinion. The agents in our model are replaced ...

We study the conditions under which input-output networks can dynamically attain a competitive equilibrium, where markets clear and profits are zero. We endow a classical firm network model with min...

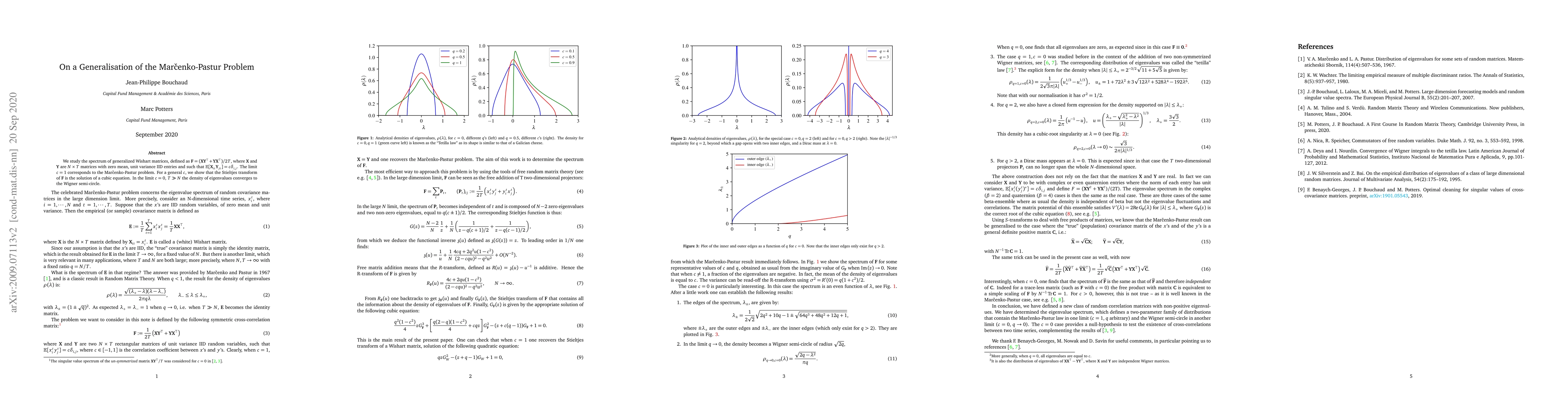

We study the spectrum of generalized Wishart matrices, defined as $\mathbf{F}=( X Y^\top + Y X^\top)/2T$, where $X$ and $Y$ are $N \times T$ matrices with zero mean, unit variance IID entries and su...

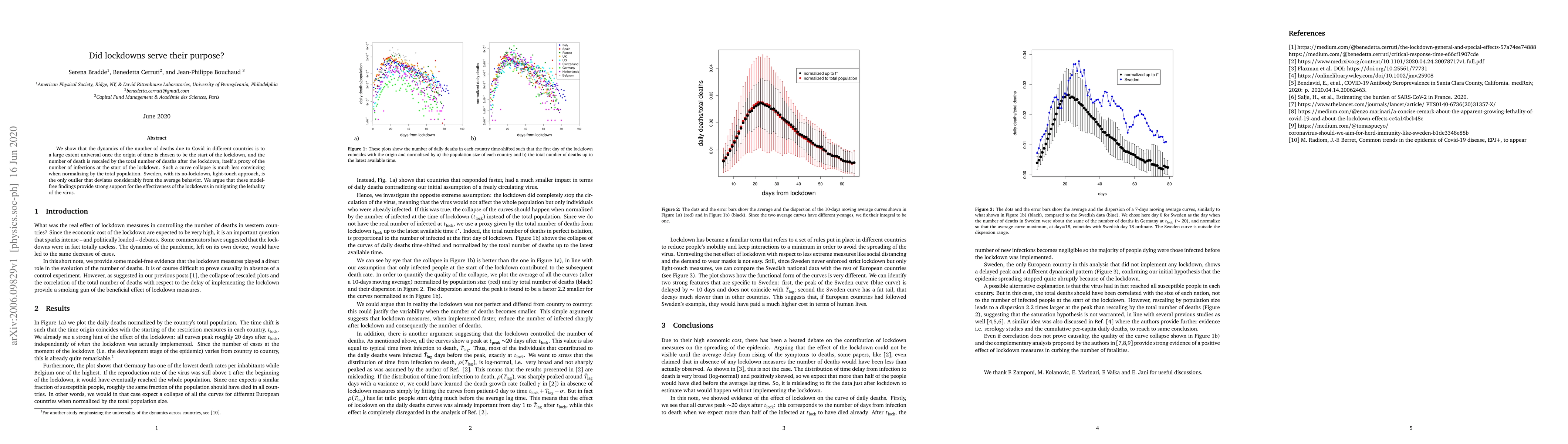

We show that the dynamics of the number of deaths due to Covid in different countries is to a large extent universal once the origin of time is chosen to be the start of the lockdown, and the number...

We propose an actionable calibration procedure for general Quadratic Hawkes models of order book events (market orders, limit orders, cancellations). One of the main features of such models is to en...

We propose a highly schematic economic model in which, in some cases, wage inequalities lead to higher overall social welfare. This is due to the fact that high earners can consume low productivity,...

We show how the approach to equilibrium in Kirman's ants model can be fully characterized in terms of the spectrum of a Schr\"odinger equation with a P\"oschl-Teller ($\tan^2$) potential. Among othe...

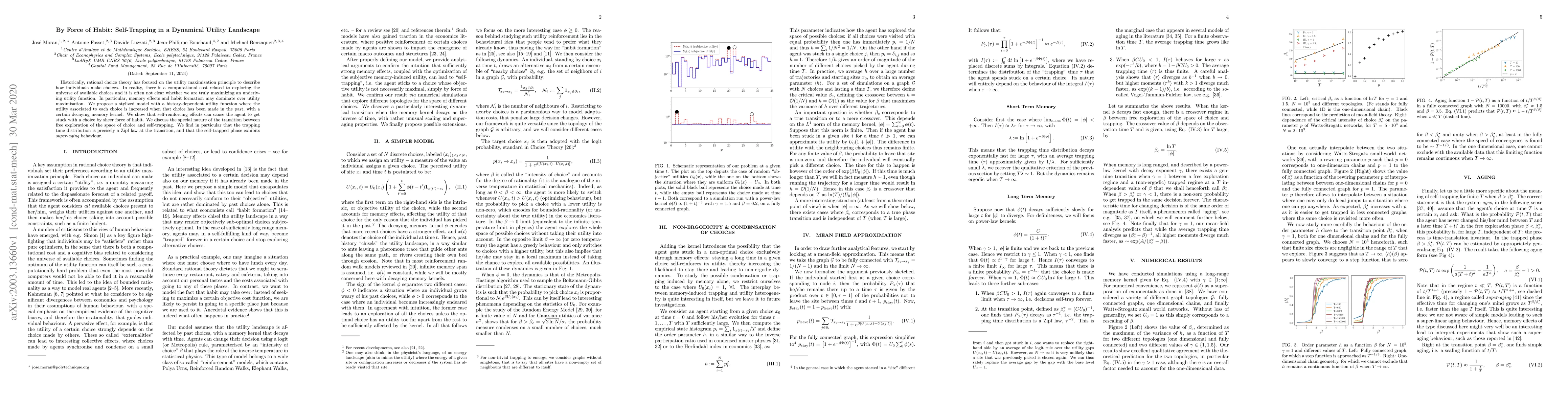

Historically, rational choice theory has focused on the utility maximization principle to describe how individuals make choices. In reality, there is a computational cost related to exploring the un...

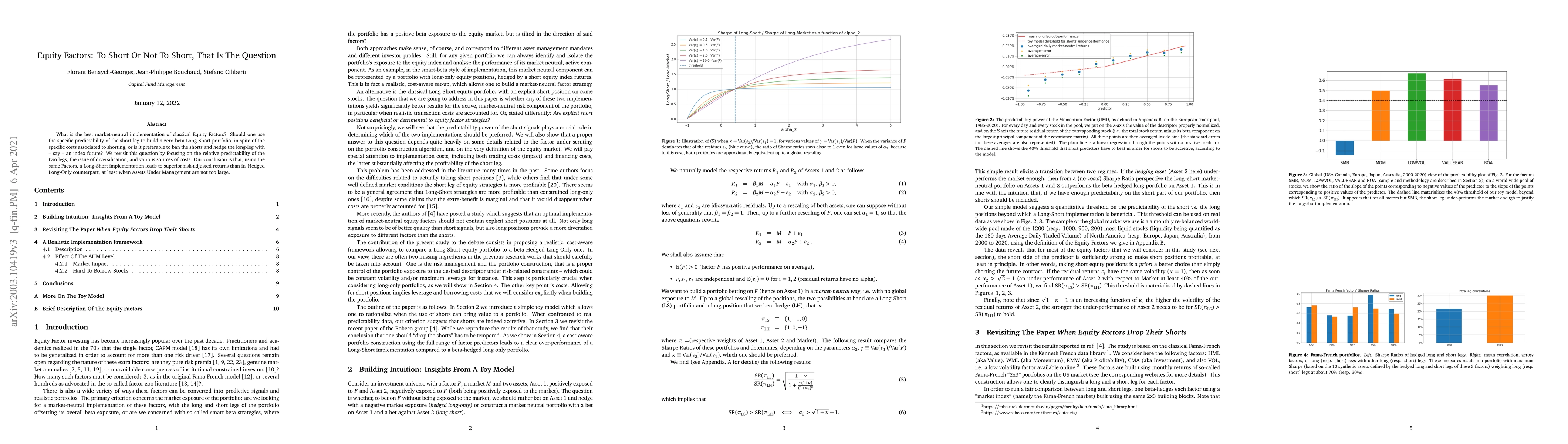

What is the best market-neutral implementation of classical Equity Factors? Should one use the specific predictability of the short-leg to build a zero beta Long-Short portfolio, in spite of the spe...

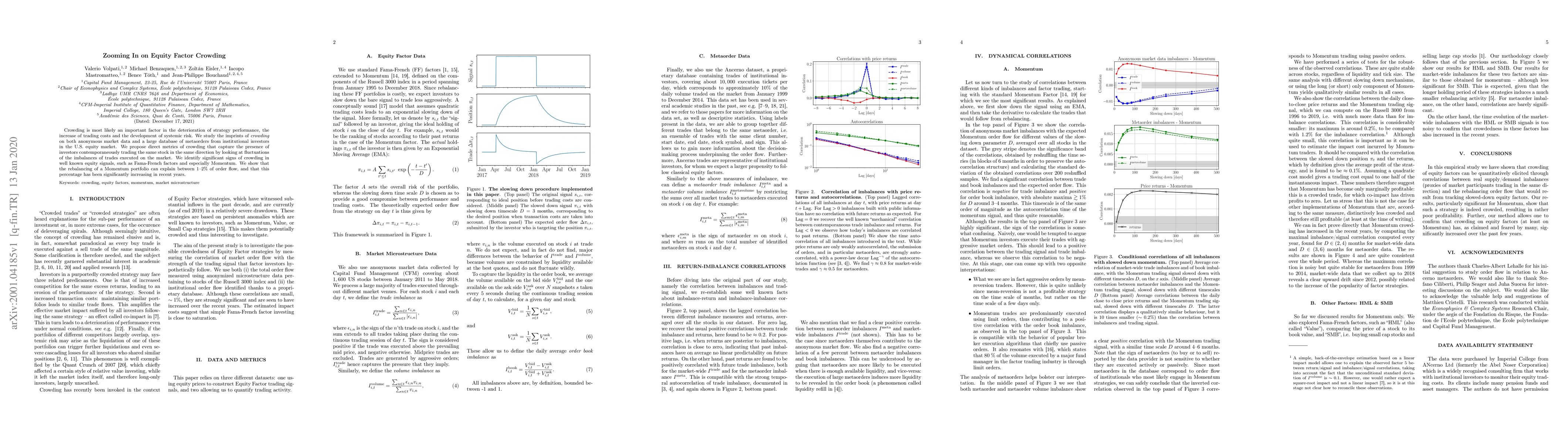

Crowding is most likely an important factor in the deterioration of strategy performance, the increase of trading costs and the development of systemic risk. We study the imprints of \emph{crowding}...

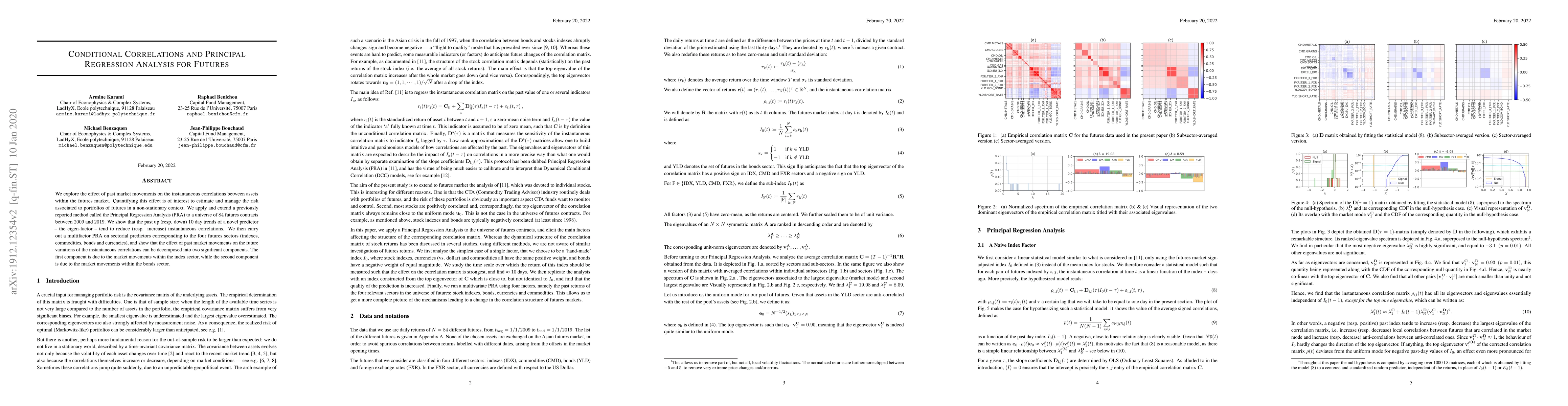

We explore the effect of past market movements on the instantaneous correlations between assets within the futures market. Quantifying this effect is of interest to estimate and manage the risk asso...

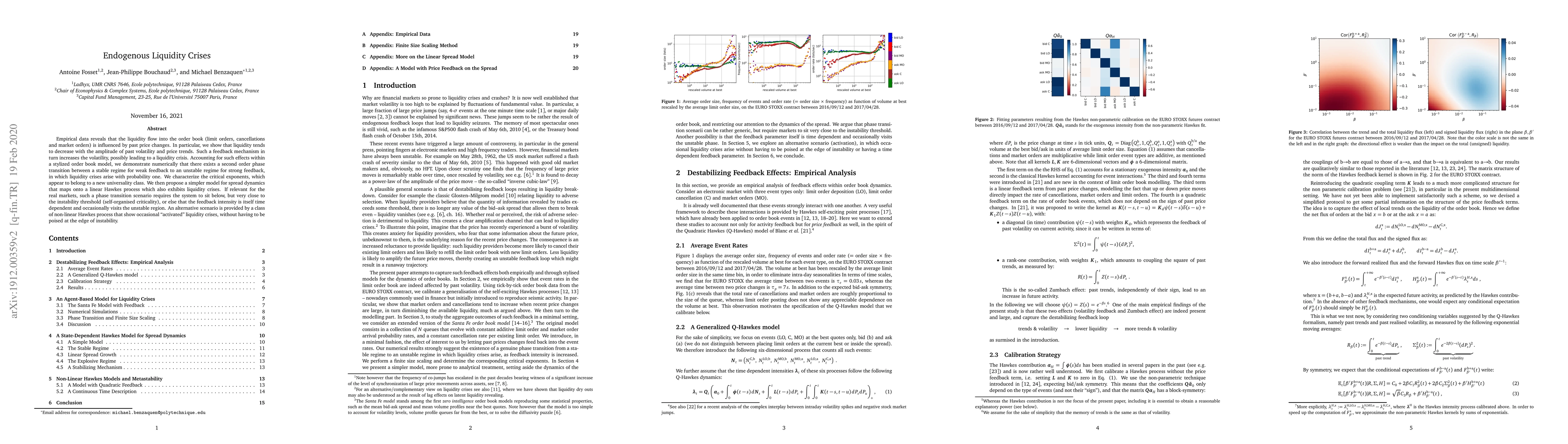

Empirical data reveals that the liquidity flow into the order book (depositions, cancellations andmarket orders) is influenced by past price changes. In particular, we show that liquidity tends tode...

We revisit the long-standing question of the relation between image appreciation and its statistical properties. We generate two different sets of random images well distributed along three measures...

We investigate a multi-household DSGE model in which past aggregate consumption impacts the confidence, and therefore consumption propensity, of individual households. We find that such a minimal se...

We advocate the use of Agnostic Allocation for the construction of long-only portfolios of stocks. We show that Agnostic Allocation Portfolios (AAPs) are a special member of a family of risk-based p...

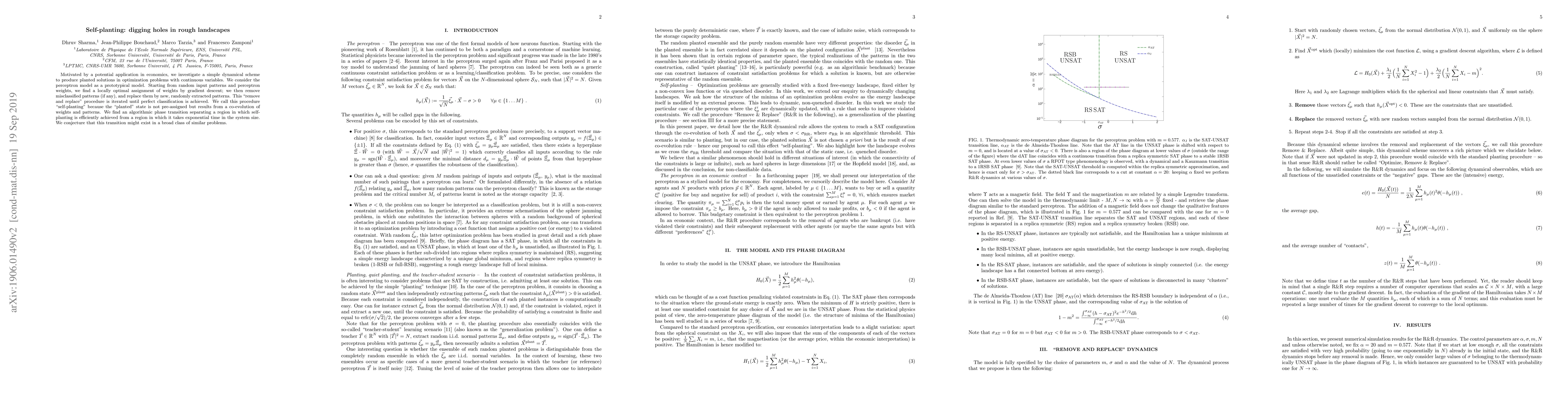

Motivated by a potential application in economics, we investigate a simple dynamical scheme to produce planted solutions in optimization problems with continuous variables. We consider the perceptro...

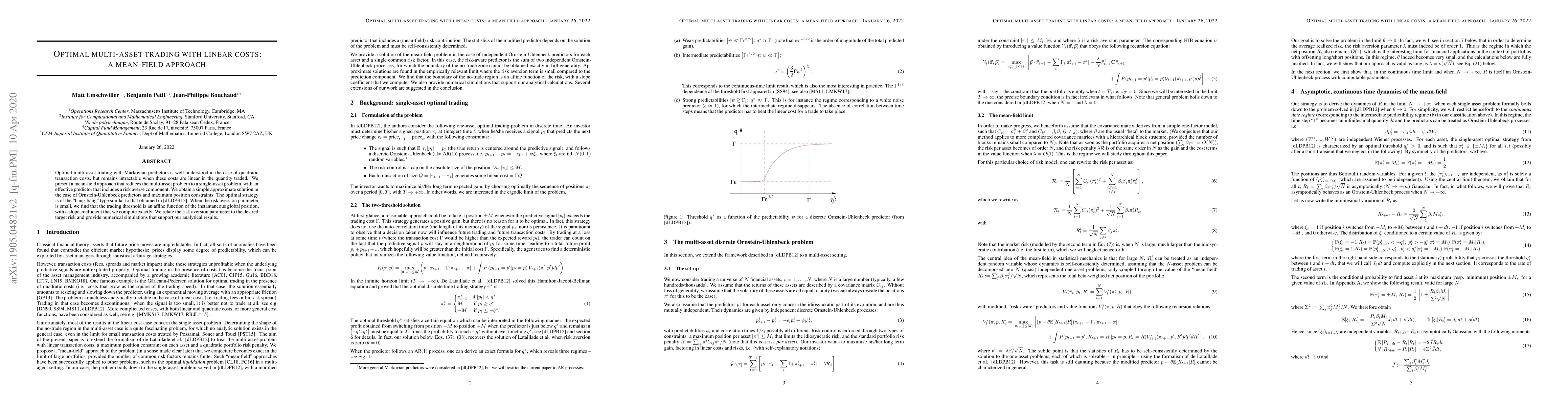

Optimal multi-asset trading with Markovian predictors is well understood in the case of quadratic transaction costs, but remains intractable when these costs are $L_1$. We present a mean-field appro...

Will a large economy be stable? Building on Robert May's original argument for large ecosystems, we conjecture that evolutionary and behavioural forces conspire to drive the economy towards marginal...

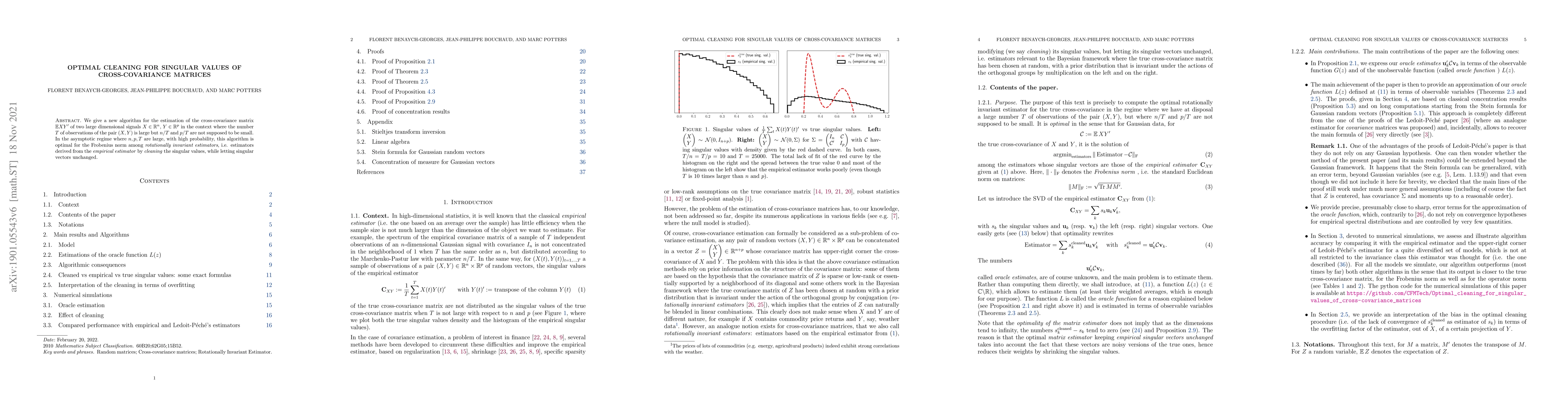

We give a new algorithm for the estimation of the cross-covariance matrix $\mathbb{E} XY'$ of two large dimensional signals $X\in\mathbb{R}^n$, $Y\in \mathbb{R}^p$ in the context where the number $T...

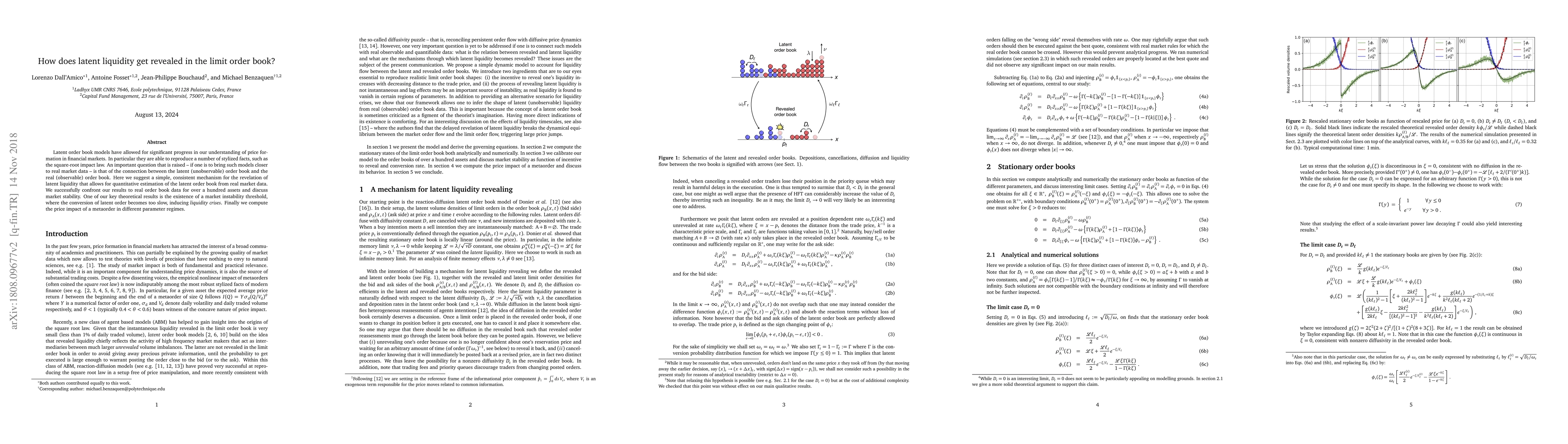

Latent order book models have allowed for significant progress in our understanding of price formation in financial markets. In particular they are able to reproduce a number of stylized facts, such...

``Self-Organised Criticality'' (SOC) is the mechanism by which complex systems spontaneously settle close to a *critical point*, at the edge between stability and chaos, and characterized by fat-taile...

The eigenvalue spectrum of the sum of large random matrices that are mutually "free", i.e. randomly rotated, can be obtained using the formalism of R-transforms, with many applications in different fi...

The study of eigenvalue distributions in random matrix theory is often conducted by analyzing the resolvent matrix $ \mathbf{G}_{\mathbf{M}}^N(z) = (z \mathbf{1} - \mathbf{M})^{-1} $. The normalized t...

We analyze the French housing market prices in the period 1970-2022, with high-resolution data from 2018 to 2022. The spatial correlation of the observed price field exhibits logarithmic decay charact...

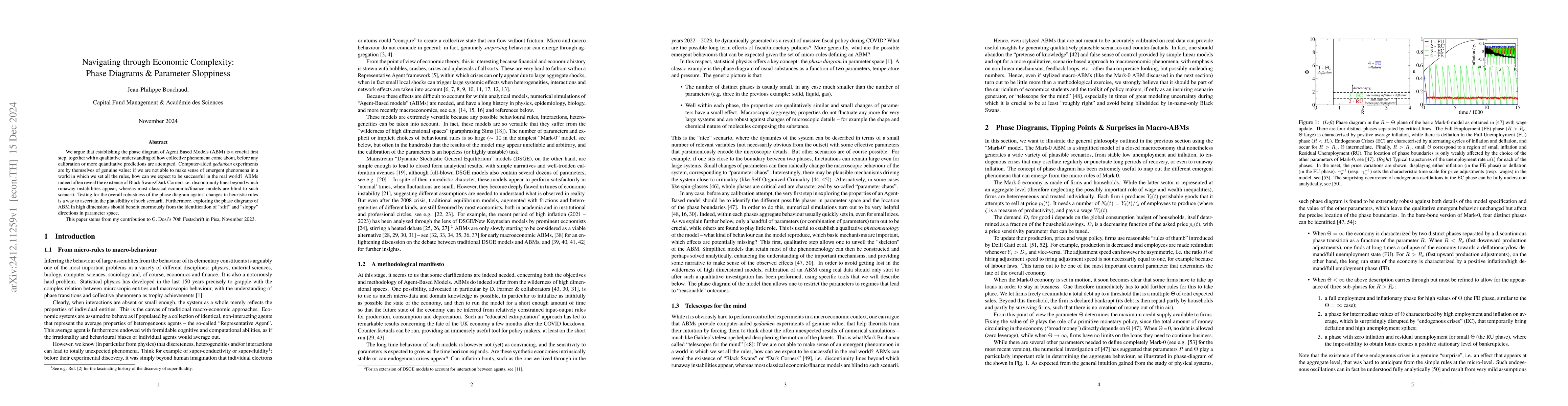

We argue that establishing the phase diagram of Agent Based Models (ABM) is a crucial first step, together with a qualitative understanding of how collective phenomena come about, before any calibrati...

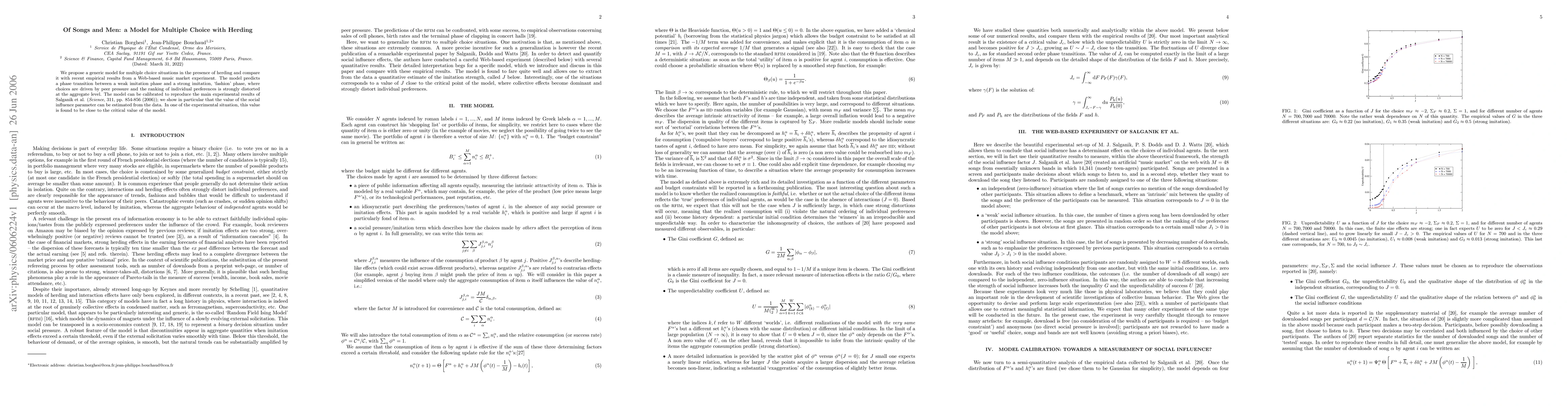

We propose a generic model for multiple choice situations in the presence of herding and compare it with recent empirical results from a Web-based music market experiment. The model predicts a phase t...

The simplest field theory description of the multivariate statistics of forward rate variations over time and maturities, involves a quadratic action containing a gradient squared rigidity term. Howev...

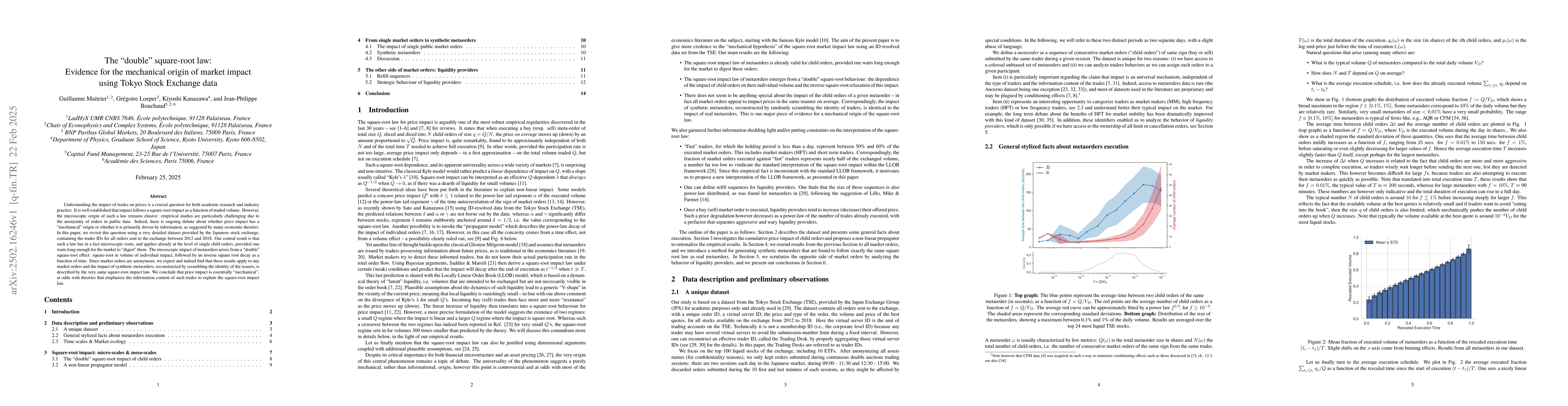

Understanding the impact of trades on prices is a crucial question for both academic research and industry practice. It is well established that impact follows a square-root impact as a function of tr...

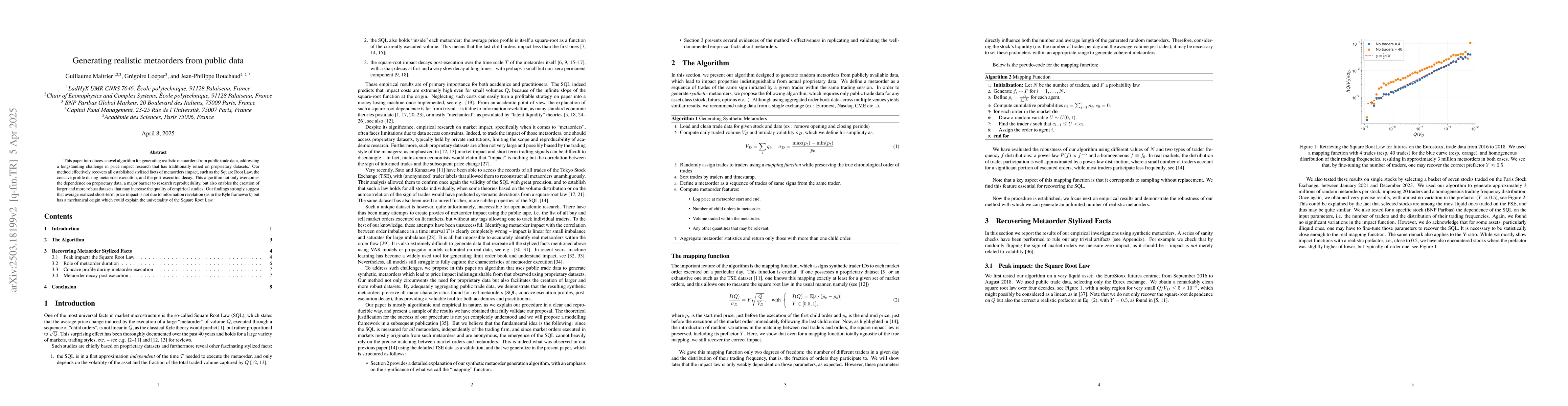

This paper introduces a novel algorithm for generating realistic metaorders from public trade data, addressing a longstanding challenge in price impact research that has traditionally relied on propri...

We study the competition between random multiplicative growth and redistribution/migration in the mean-field limit, when the number of sites is very large but finite. We find that for static random gr...

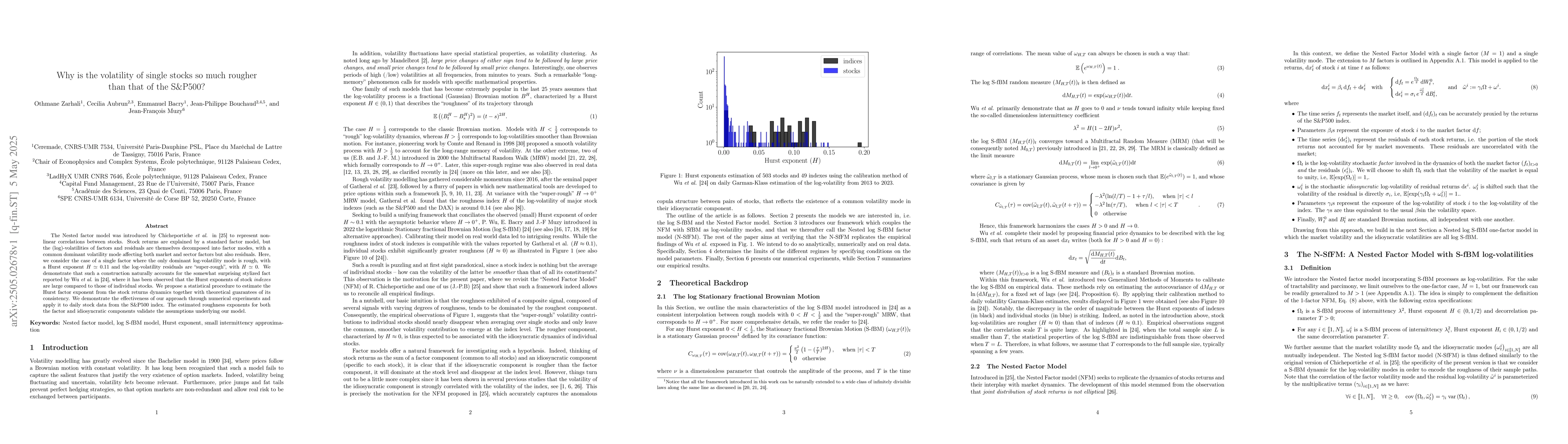

The Nested factor model was introduced by Chicheportiche et al. to represent non-linear correlations between stocks. Stock returns are explained by a standard factor model, but the (log)-volatilities ...

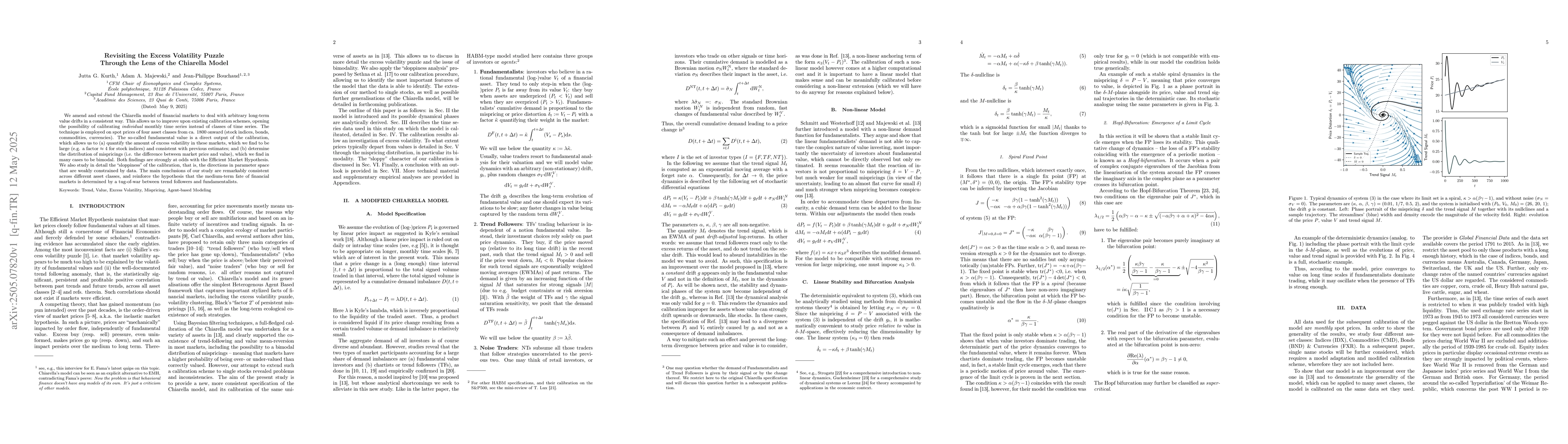

We amend and extend the Chiarella model of financial markets to deal with arbitrary long-term value drifts in a consistent way. This allows us to improve upon existing calibration schemes, opening the...

In this work, we aim to reconcile several apparently contradictory observations in market microstructure: is the famous ''square-root law'' of metaorder impact that decays with time compatible with th...

This work extends and complements our previous theoretical paper on the subtle interplay between impact, order flow and volatility. In the present paper, we generate synthetic market data following th...

Cross-validation is one of the most widely used methods for model selection and evaluation; its efficiency for large covariance matrix estimation appears robust in practice, but little is known about ...

This is the second part of our work on Multivariate Quadratic Hawkes (MQHawkes) Processes, devoted to the calibration of the model defined and studied analytically in Aubrun, C., Benzaquen, M., & Bouc...

We compute exactly the overlap between the eigenvectors of two large empirical covariance matrices computed over intersecting time intervals, generalizing the results obtained previously for non-inter...

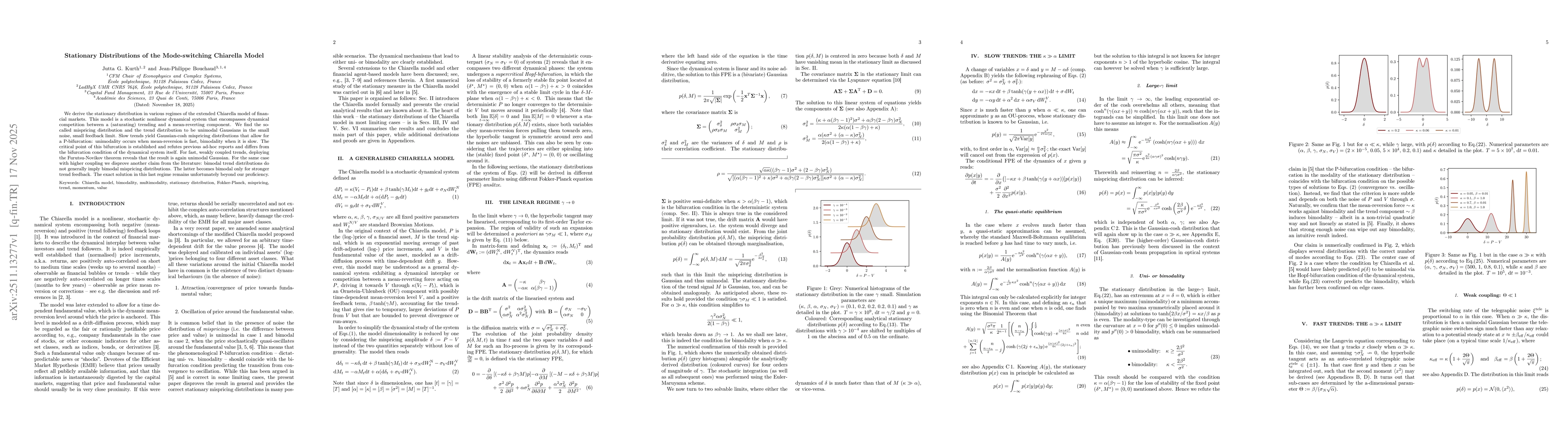

We derive the stationary distribution in various regimes of the extended Chiarella model of financial markets. This model is a stochastic nonlinear dynamical system that encompasses dynamical competit...

We propose a generic model for multiple choice situations in the presence of herding and compare it with recent empirical results from a Web-based music market experiment. The model predicts a phase t...

The simplest field theory description of the multivariate statistics of forward rate variations over time and maturities, involves a quadratic action containing a gradient squared rigidity term. Howev...

We study the disequilibrium dynamics of a stylised model of production networks in which firms use perishable and non-substitutable intermediate inputs, so that adverse idiosyncratic productivity shoc...

This text revisits the origins of econophysics through the figure of Benoît Mandelbrot, not as the father of fractals, but as the instigator of a distinctive scientific posture. The guiding thread is ...

Empirical studies of trained models often report a transient regime in which signal is detectable in a finite gradient descent time window before overfitting dominates. We provide an analytically trac...

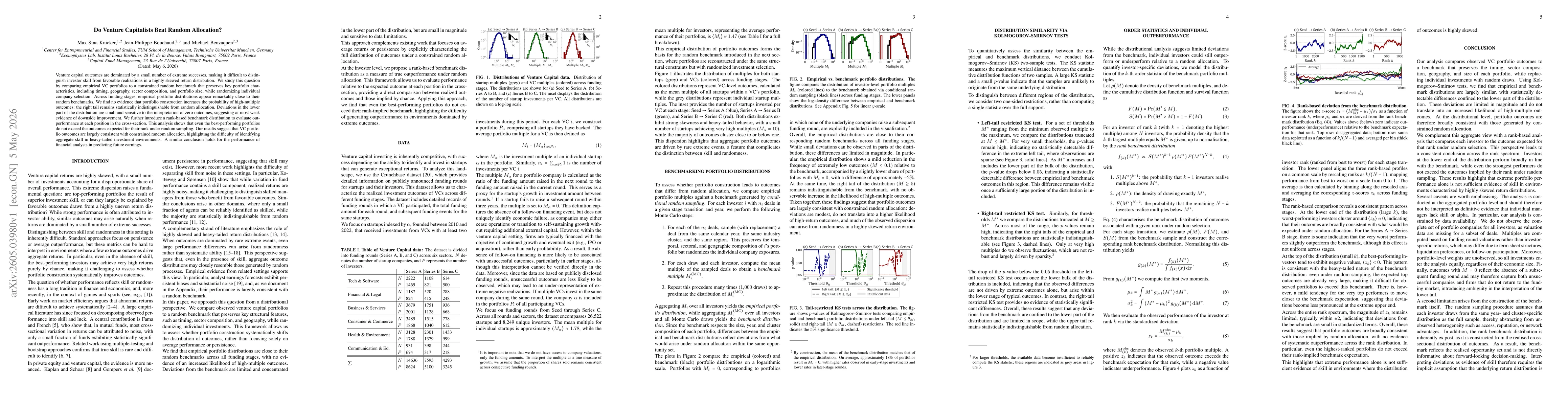

Venture capital outcomes are dominated by a small number of extreme successes, making it difficult to distinguish investor skill from favorable realizations in a highly skewed return distribution. We ...

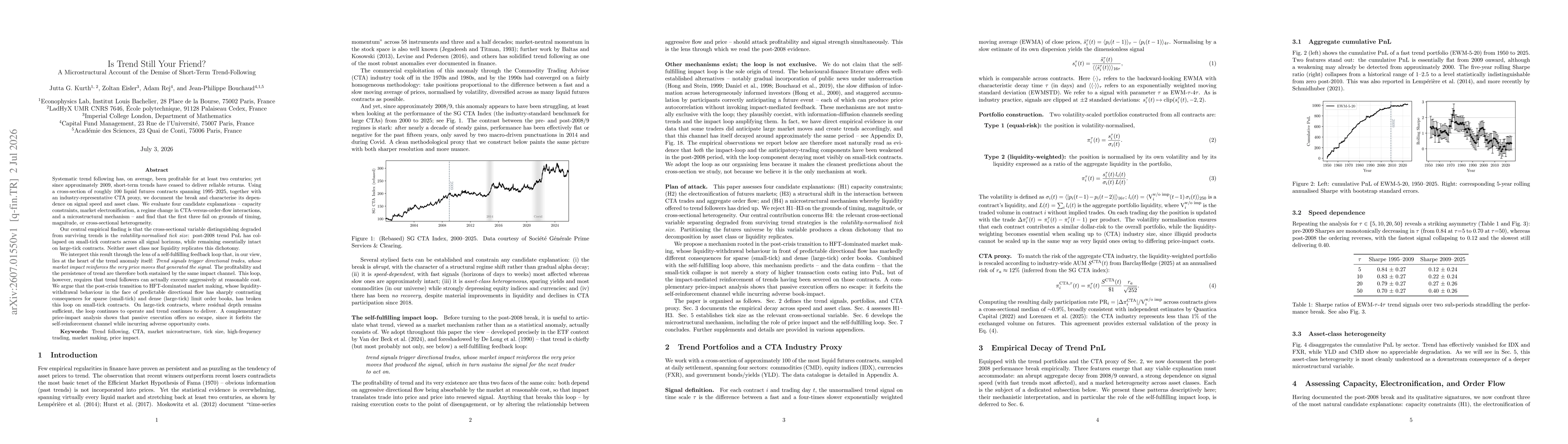

Systematic trend following has, on average, been profitable for at least two centuries; yet since approximately 2009, short-term trends have ceased to deliver reliable returns. Using a cross-section o...