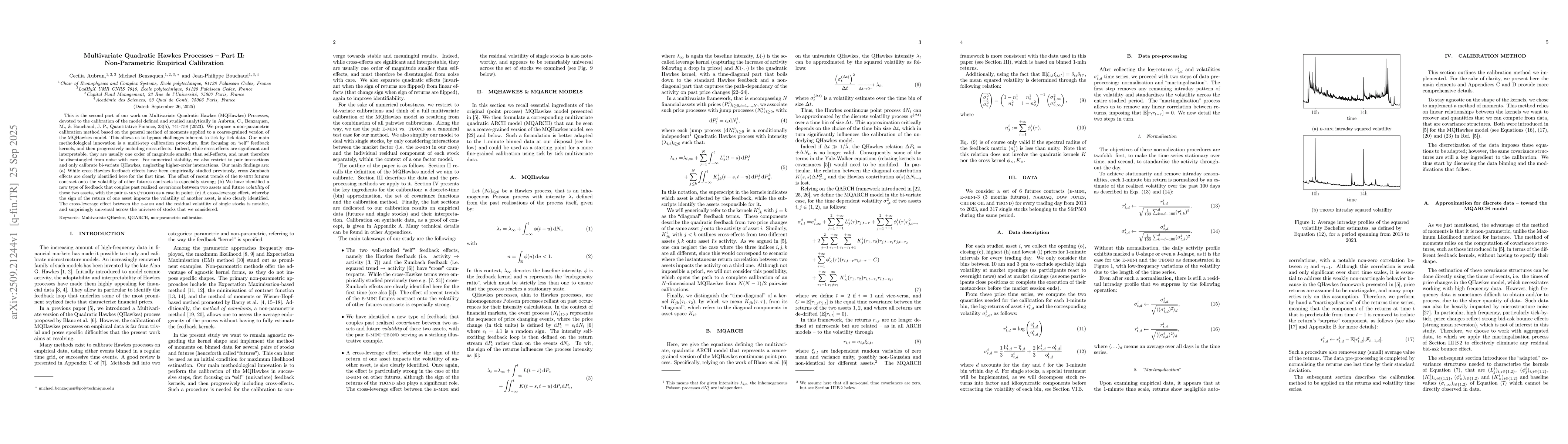

This is the second part of our work on Multivariate Quadratic Hawkes

(MQHawkes) Processes, devoted to the calibration of the model defined and

studied analytically in Aubrun, C., Benzaquen, M., & Bouchaud, J. P.,

Quantitative Finance, 23(5), 741-758 (2023). We propose a non-parametric

calibration method based on the general method of moments applied to a

coarse-grained version of the MQHawkes model. This allows us to bypass

challenges inherent to tick by tick data. Our main methodological innovation is

a multi-step calibration procedure, first focusing on ''self'' feedback

kernels, and then progressively including cross-effects. Indeed, while

cross-effects are significant and interpretable, they are usually one order of

magnitude smaller than self-effects, and must therefore be disentangled from

noise with care. For numerical stability, we also restrict to pair interactions

and only calibrate bi-variate QHawkes, neglecting higher-order interactions.

Our main findings are: (a) While cross-Hawkes feedback effects have been

empirically studied previously, cross-Zumbach effects are clearly identified

here for the first time. The effect of recent trends of the E-Mini futures

contract onto the volatility of other futures contracts is especially strong;

(b) We have identified a new type of feedback that couples past realized

covariance between two assets and future volatility of these two assets, with

the pair E-Mini vs TBOND as a case in point; (c) A cross-leverage effect,

whereby the sign of the return of one asset impacts the volatility of another

asset, is also clearly identified. The cross-leverage effect between the E-Mini

and the residual volatility of single stocks is notable, and surprisingly

universal across the universe of stocks that we considered.

Discussion 0