Academic Profile

Statistics

Similar Authors

Papers on arXiv

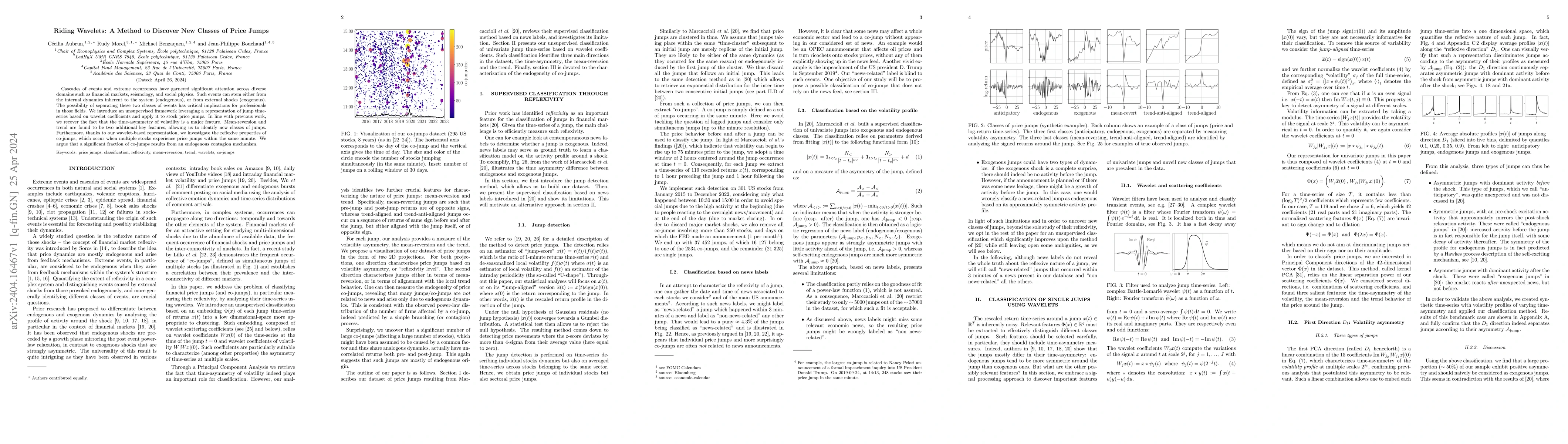

Cascades of events and extreme occurrences have garnered significant attention across diverse domains such as financial markets, seismology, and social physics. Such events can stem either from the ...

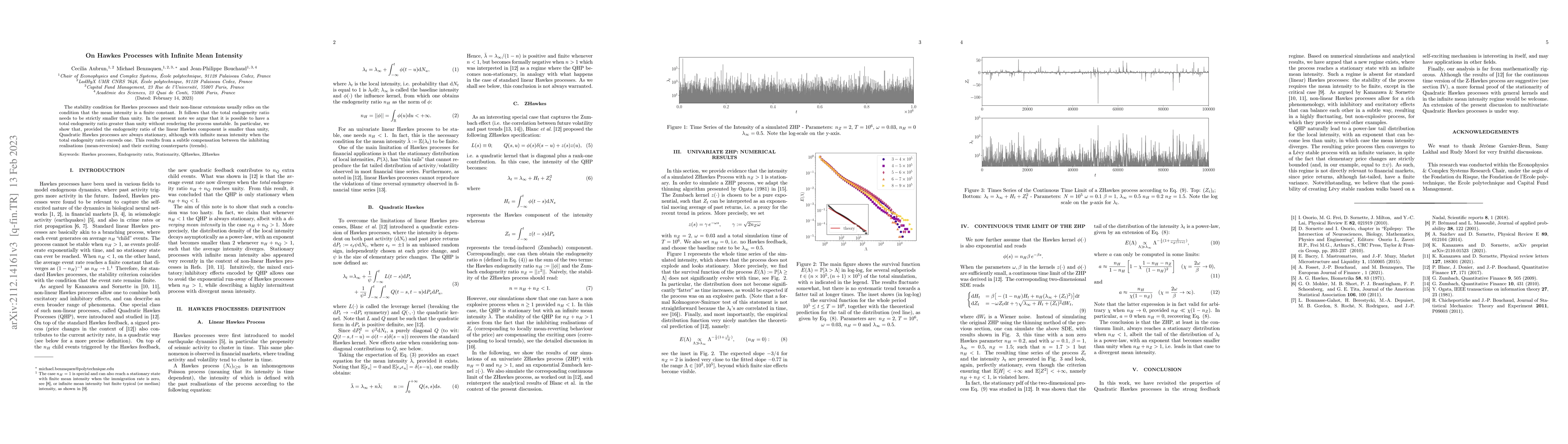

The stability condition for Hawkes processes and their non-linear extensions usually relies on the condition that the mean intensity is a finite constant. It follows that the total endogeneity ratio...

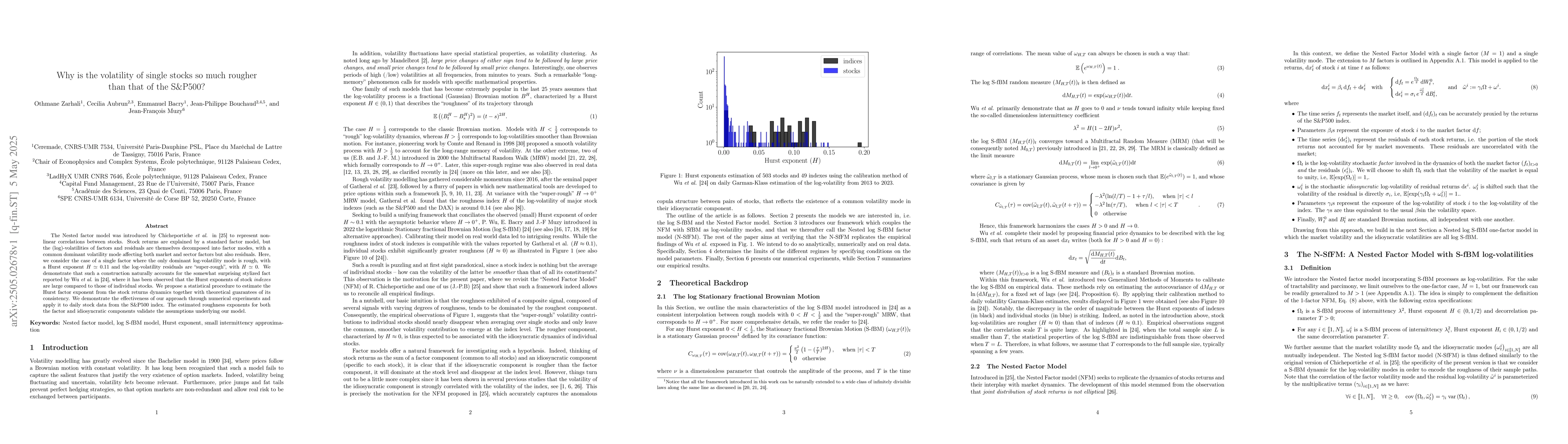

The Nested factor model was introduced by Chicheportiche et al. to represent non-linear correlations between stocks. Stock returns are explained by a standard factor model, but the (log)-volatilities ...

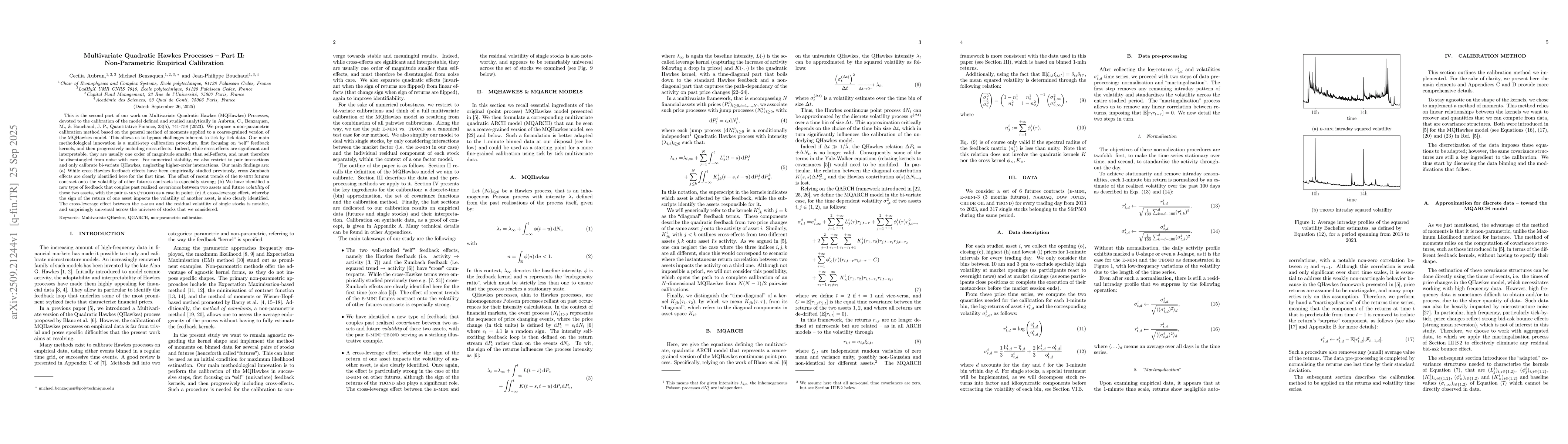

This is the second part of our work on Multivariate Quadratic Hawkes (MQHawkes) Processes, devoted to the calibration of the model defined and studied analytically in Aubrun, C., Benzaquen, M., & Bouc...