Publication

Metrics

AI Quick Summary

This study synchronizes stock news and order book data to reveal that exogenous price jumps following news differ dynamically from endogenous jumps. Exogenous jumps show abrupt volatility spikes followed by a decaying power-law relaxation, while endogenous jumps feature accelerating volatility growth followed by a slower power-law relaxation. This classification method, based on power-law fits, can categorize events without relying on news feeds.

Paper Preview

Abstract

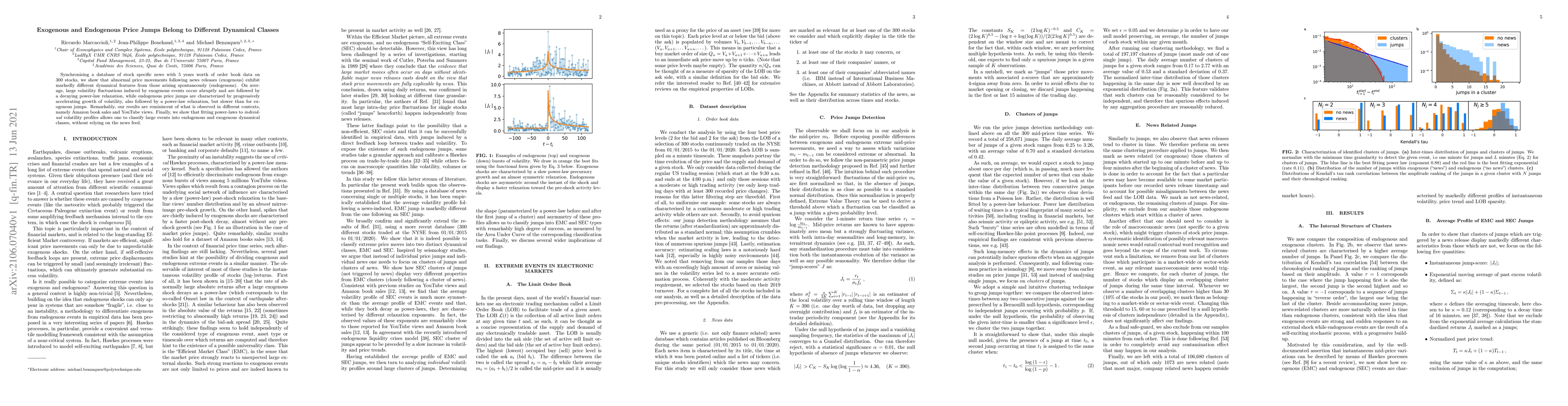

Synchronising a database of stock specific news with 5 years worth of order book data on 300 stocks, we show that abnormal price movements following news releases (exogenous) exhibit markedly different dynamical features from those arising spontaneously (endogenous). On average, large volatility fluctuations induced by exogenous events occur abruptly and are followed by a decaying power-law relaxation, while endogenous price jumps are characterized by progressively accelerating growth of volatility, also followed by a power-law relaxation, but slower than for exogenous jumps. Remarkably, our results are reminiscent of what is observed in different contexts, namely Amazon book sales and YouTube views. Finally, we show that fitting power-laws to {\it individual} volatility profiles allows one to classify large events into endogenous and exogenous dynamical classes, without relying on the news feed.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0