Riccardo Marcaccioli

4 papers on arXiv

Academic Profile

Statistics

Similar Authors

Papers on arXiv

Exogenous and Endogenous Price Jumps Belong to Different Dynamical Classes

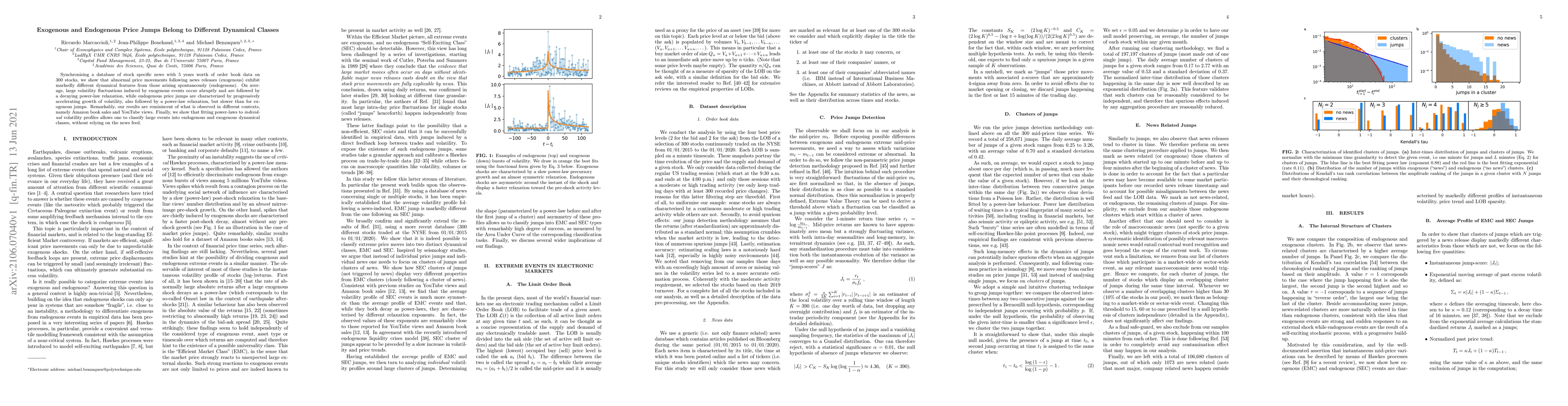

Synchronising a database of stock specific news with 5 years worth of order book data on 300 stocks, we show that abnormal price movements following news releases (exogenous) exhibit markedly differ...

Deep Reinforcement Learning for Active High Frequency Trading

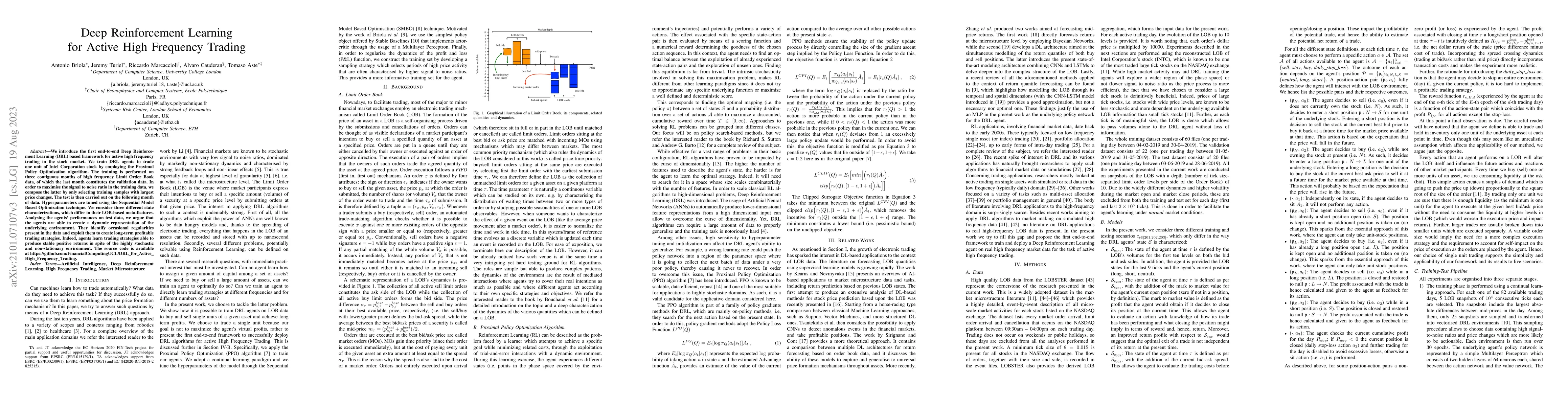

We introduce the first end-to-end Deep Reinforcement Learning (DRL) based framework for active high frequency trading in the stock market. We train DRL agents to trade one unit of Intel Corporation ...

Maximum Entropy approach to multivariate time series randomization

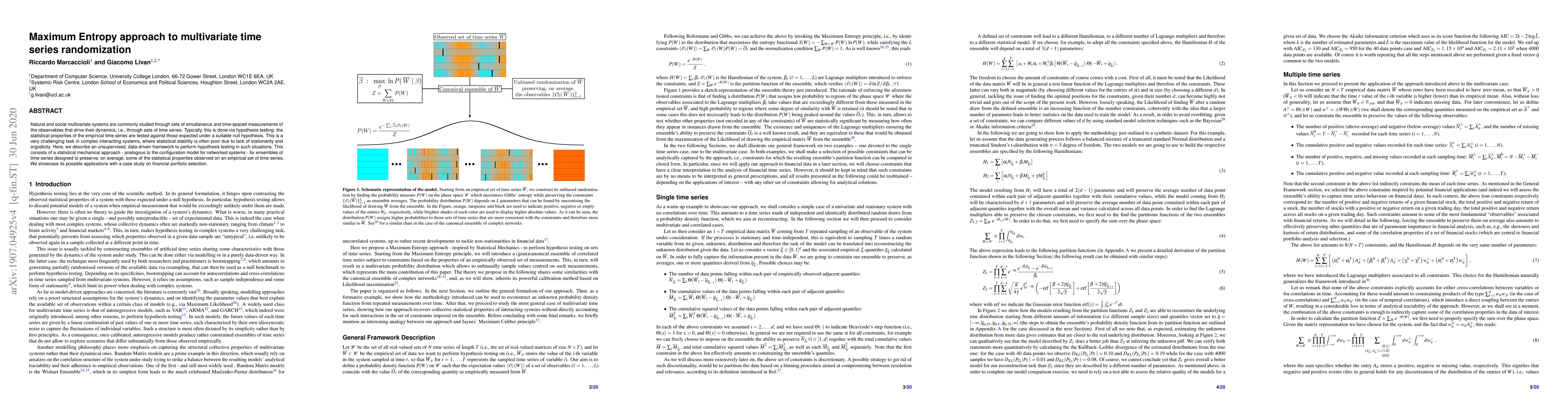

Natural and social multivariate systems are commonly studied through sets of simultaneous and time-spaced measurements of the observables that drive their dynamics, i.e., through sets of time series...

A Random-Matrix Criterion for Initializing Gated Recurrent Neural Networks

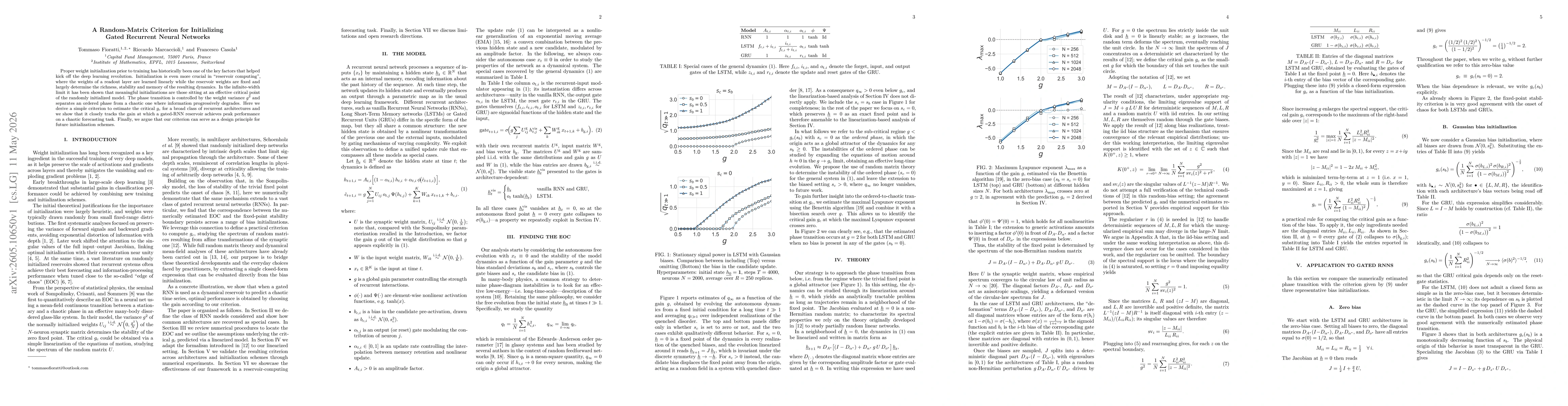

Proper weight initialization prior to training has historically been one of the key factors that helped kick off the deep learning revolution. Initialization is even more crucial in "reservoir computi...