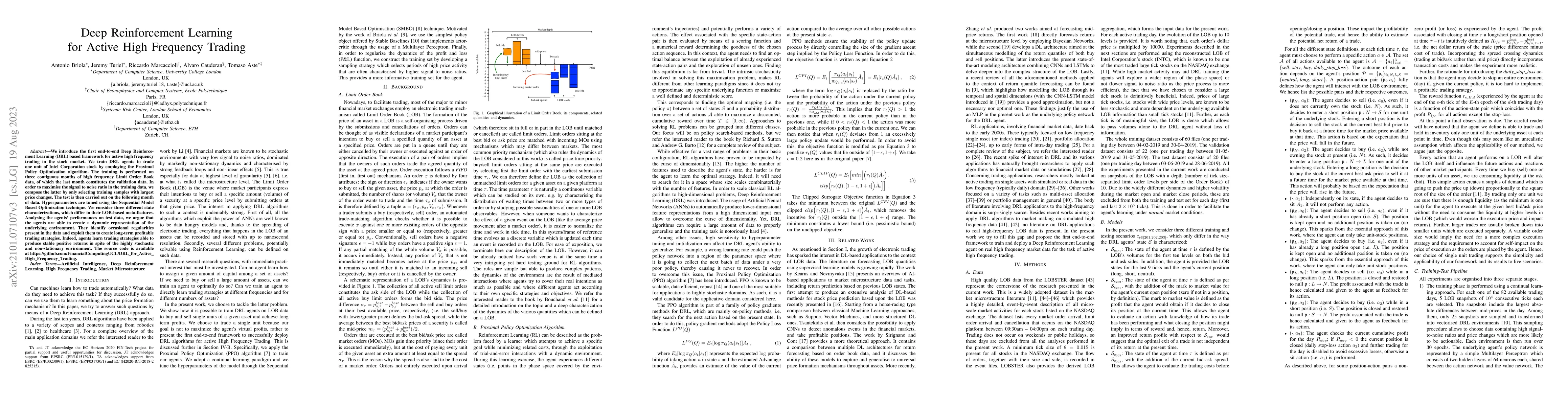

Deep Reinforcement Learning for Active High Frequency Trading

Publication

Metrics

AI Quick Summary

This paper presents a Deep Reinforcement Learning framework for active high frequency trading, specifically training DRL agents to trade Intel stock using the Proximal Policy Optimization algorithm. The agents demonstrate the ability to generate profitable trading strategies by learning and exploiting occasional market regularities despite the stochastic nature of the trading environment.

Paper Preview

Abstract

We introduce the first end-to-end Deep Reinforcement Learning (DRL) based framework for active high frequency trading in the stock market. We train DRL agents to trade one unit of Intel Corporation stock by employing the Proximal Policy Optimization algorithm. The training is performed on three contiguous months of high frequency Limit Order Book data, of which the last month constitutes the validation data. In order to maximise the signal to noise ratio in the training data, we compose the latter by only selecting training samples with largest price changes. The test is then carried out on the following month of data. Hyperparameters are tuned using the Sequential Model Based Optimization technique. We consider three different state characterizations, which differ in their LOB-based meta-features. Analysing the agents' performances on test data, we argue that the agents are able to create a dynamic representation of the underlying environment. They identify occasional regularities present in the data and exploit them to create long-term profitable trading strategies. Indeed, agents learn trading strategies able to produce stable positive returns in spite of the highly stochastic and non-stationary environment.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0