Academic Profile

Statistics

Similar Authors

Papers on arXiv

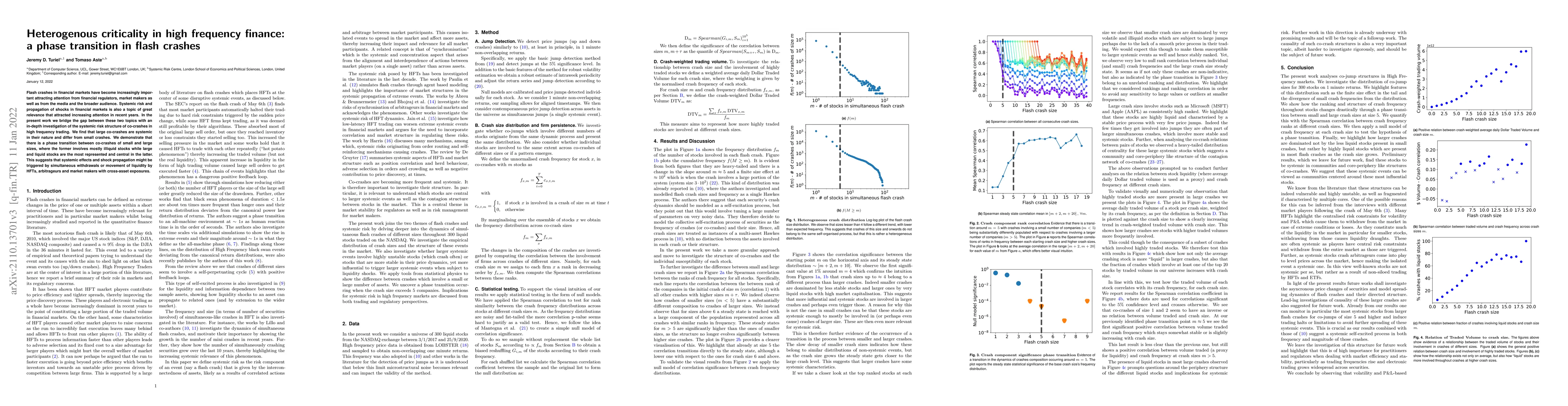

Flash crashes in financial markets have become increasingly important attracting attention from financial regulators, market makers as well as from the media and the broader audience. Systemic risk ...

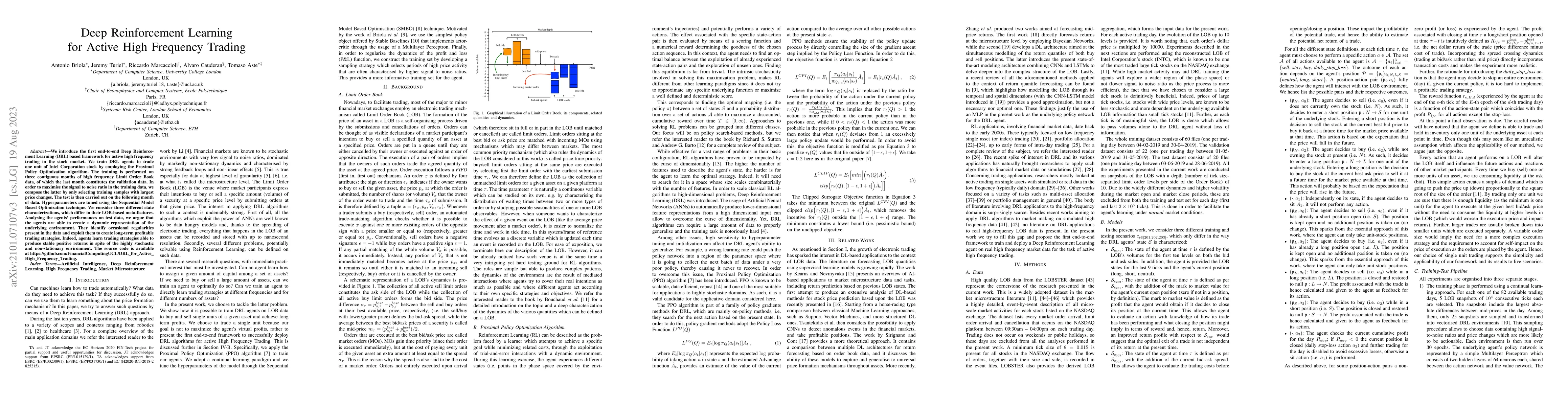

We introduce the first end-to-end Deep Reinforcement Learning (DRL) based framework for active high frequency trading in the stock market. We train DRL agents to trade one unit of Intel Corporation ...

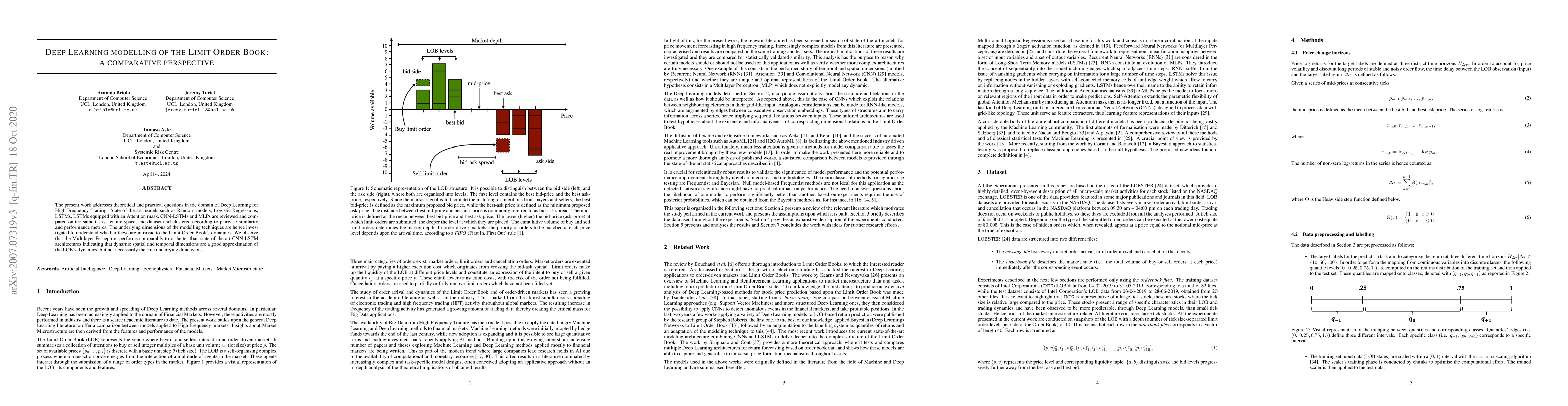

The present work addresses theoretical and practical questions in the domain of Deep Learning for High Frequency Trading. State-of-the-art models such as Random models, Logistic Regressions, LSTMs, ...