Academic Profile

Statistics

Similar Authors

Papers on arXiv

We quantify the amount of information filtered by different hierarchical clustering methods on correlations between stock returns comparing it with the underlying industrial activity structure. Spec...

We introduce a novel large-scale deep learning model for Limit Order Book mid-price changes forecasting, and we name it `HLOB'. This architecture (i) exploits the information encoded by an Informati...

We exploit cutting-edge deep learning methodologies to explore the predictability of high-frequency Limit Order Book mid-price changes for a heterogeneous set of stocks traded on the NASDAQ exchange...

Nations around the world are conducting research into the design of central bank digital currency (CBDC), a new, digital form of money that would be issued by central banks alongside cash and centra...

Modern portfolio optimization is centered around creating a low-risk portfolio with extensive asset diversification. Following the seminal work of Markowitz, optimal asset allocation can be computed...

Double descent presents a counter-intuitive aspect within the machine learning domain, and researchers have observed its manifestation in various models and tasks. While some theoretical explanation...

Deep learning methods have demonstrated outstanding performances on classification and regression tasks on homogeneous data types (e.g., image, audio, and text data). However, tabular data still pos...

We investigate the response of shareholders to Environmental, Social, and Governance-related reputational risk (ESG-risk), focusing exclusively on the impact of social media. Using a dataset of 114 ...

The rapid progress of Artificial Intelligence research came with the development of increasingly complex deep learning models, leading to growing challenges in terms of computational complexity, ene...

This paper investigates the causes of the FTX digital currency exchange's failure in November 2022. We identify the collapse of the Terra-Luna ecosystem as the pivotal event that triggered a signifi...

In this paper, we introduce a novel unsupervised, graph-based filter feature selection technique which exploits the power of topologically constrained network representations. We model dependency st...

The increasing adoption of Digital Assets (DAs), such as Bitcoin (BTC), rises the need for accurate option pricing models. Yet, existing methodologies fail to cope with the volatile nature of the em...

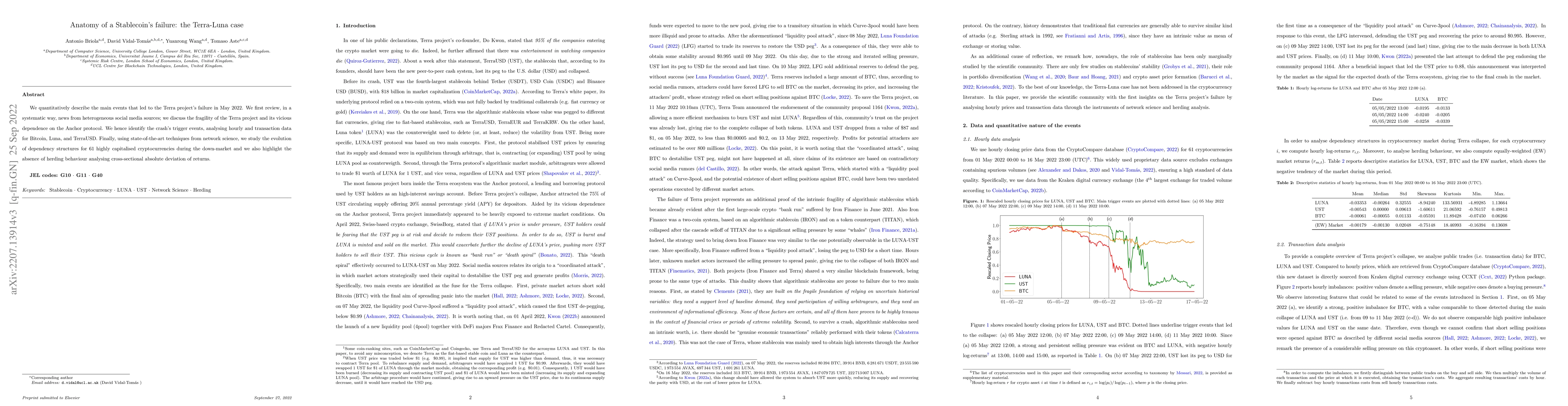

We quantitatively describe the main events that led to the Terra project's failure in May 2022. We first review, in a systematic way, news from heterogeneous social media sources; we discuss the fra...

We investigate logarithmic price returns cross-correlations at different time horizons for a set of 25 liquid cryptocurrencies traded on the FTX digital currency exchange. We study how the structure...

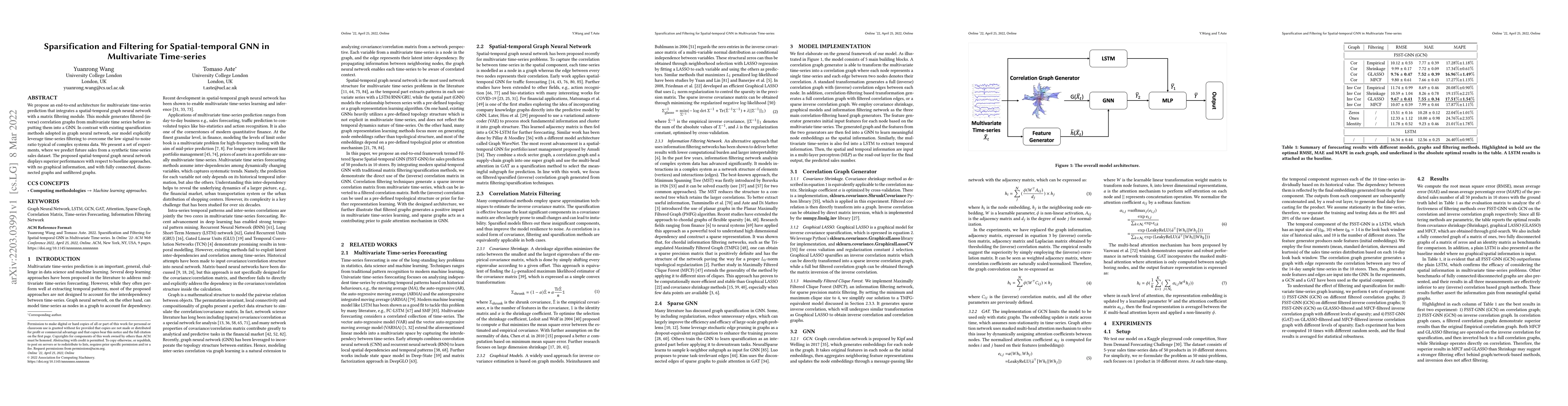

We propose an end-to-end architecture for multivariate time-series prediction that integrates a spatial-temporal graph neural network with a matrix filtering module. This module generates filtered (...

Market conditions change continuously. However, in portfolio's investment strategies, it is hard to account for this intrinsic non-stationarity. In this paper, we propose to address this issue by us...

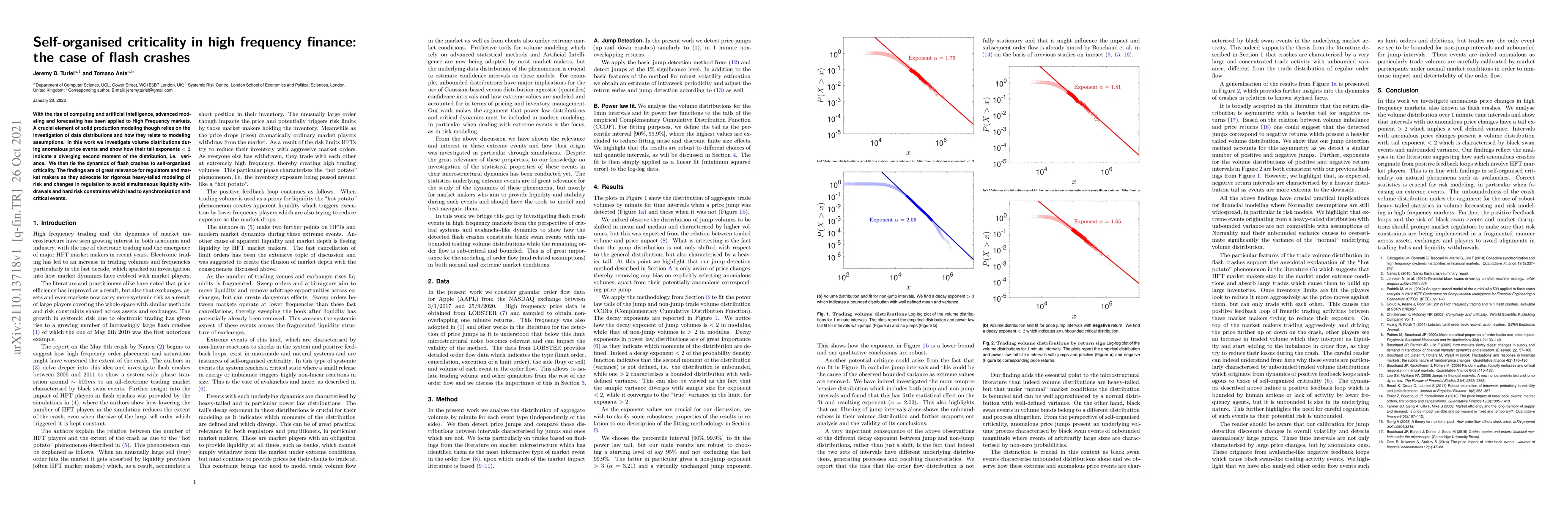

With the rise of computing and artificial intelligence, advanced modeling and forecasting has been applied to High Frequency markets. A crucial element of solid production modeling though relies on ...

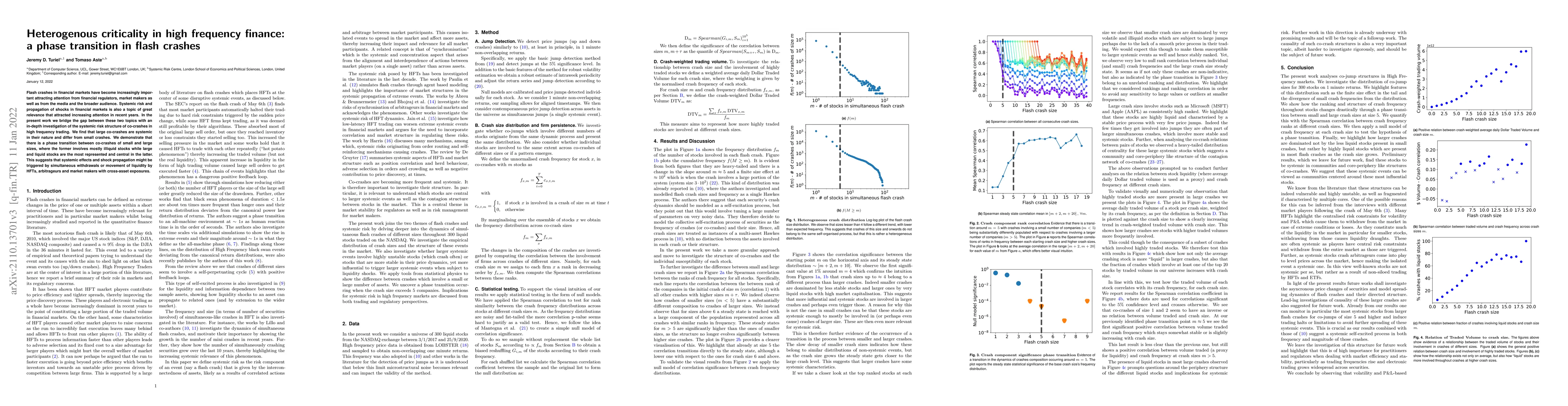

Flash crashes in financial markets have become increasingly important attracting attention from financial regulators, market makers as well as from the media and the broader audience. Systemic risk ...

We present a novel methodology to quantify the "impact" of and "response" to market shocks. We apply shocks to a group of stocks in a part of the market, and we quantify the effects in terms of aver...

Portfolio optimization approaches inevitably rely on multivariate modeling of markets and the economy. In this paper, we address three sources of error related to the modeling of these complex syste...

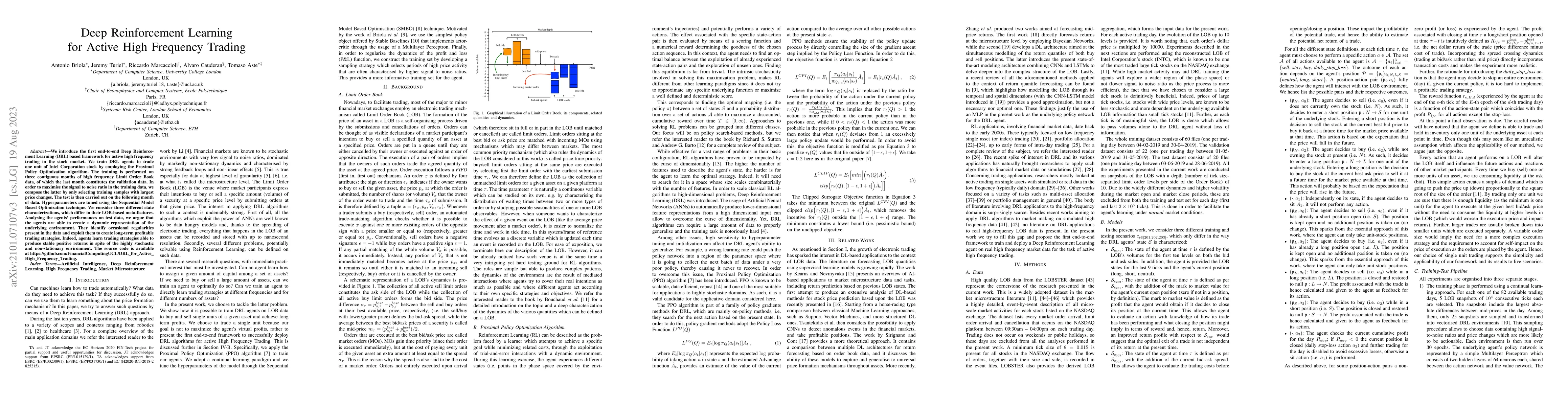

We introduce the first end-to-end Deep Reinforcement Learning (DRL) based framework for active high frequency trading in the stock market. We train DRL agents to trade one unit of Intel Corporation ...

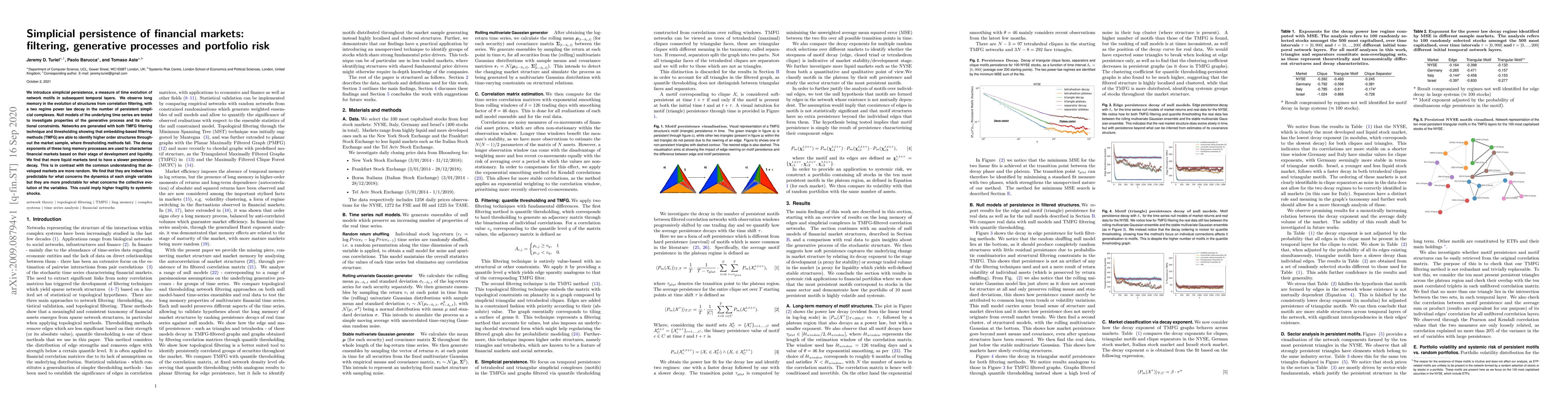

We introduce simplicial persistence, a measure of time evolution of network motifs in subsequent temporal layers. We observe long memory in the evolution of structures from correlation filtering, wi...

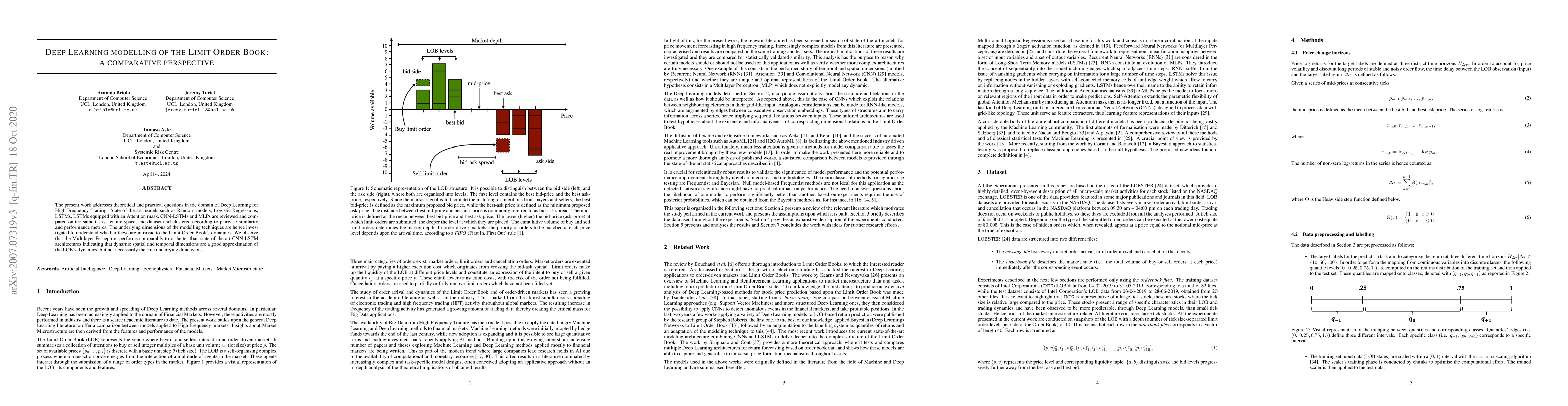

The present work addresses theoretical and practical questions in the domain of Deep Learning for High Frequency Trading. State-of-the-art models such as Random models, Logistic Regressions, LSTMs, ...

A methodology to perform topological regularization via information filtering network is introduced. This methodology can be directly applied to covariance selection problem providing an instrument ...

The Bitcoin network is burning a large amount of energy for mining. In this paper we estimate the lower bound for the global energy cost for a period of ten years from 2010, taking into account chan...

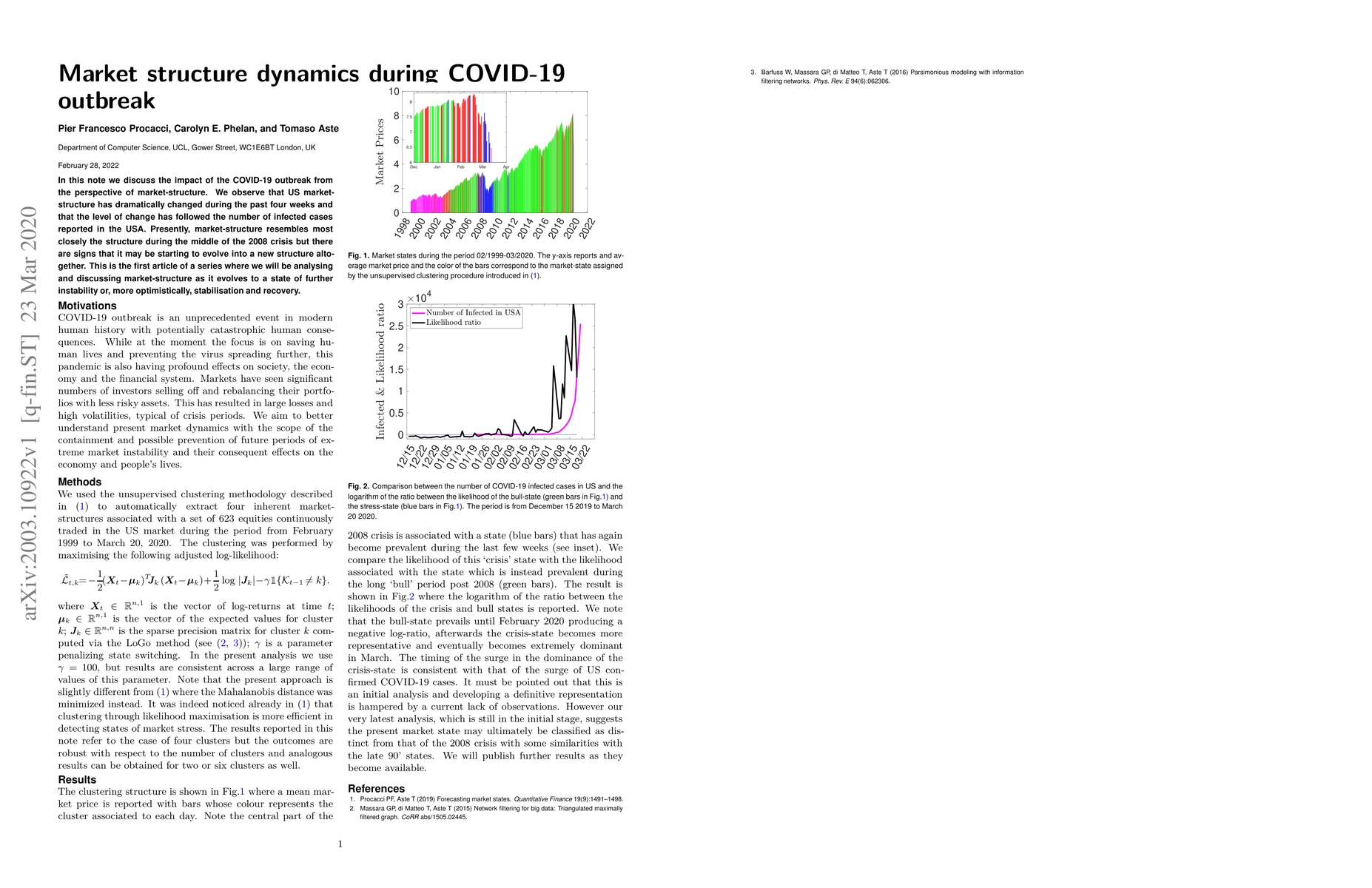

In this note, we discuss the impact of the COVID-19 outbreak from the perspective of the market-structure. We observe that the US market-structure has dramatically changed during the past four weeks...

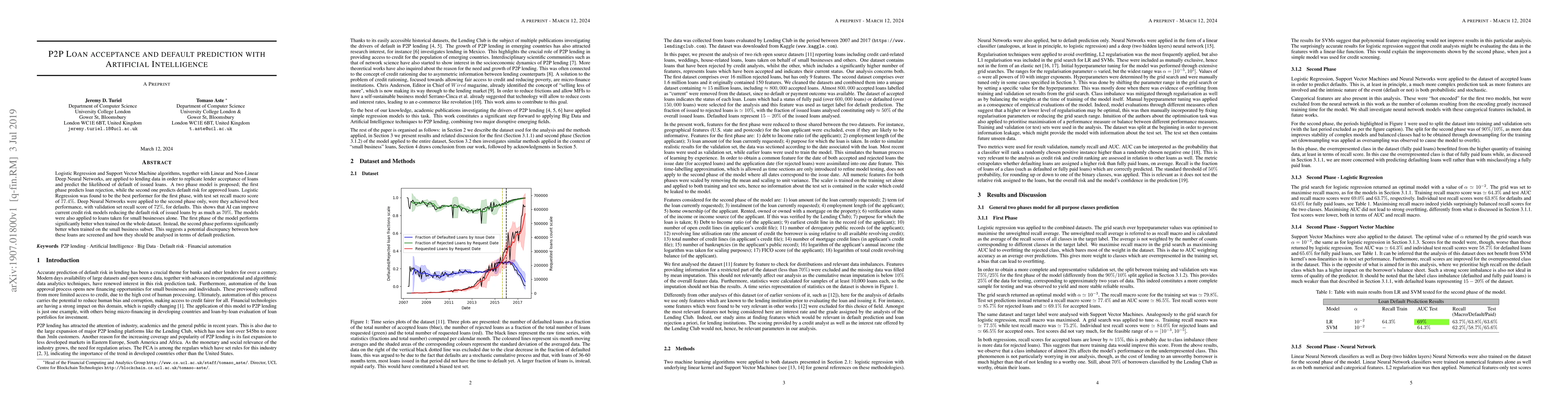

Logistic Regression and Support Vector Machine algorithms, together with Linear and Non-Linear Deep Neural Networks, are applied to lending data in order to replicate lender acceptance of loans and ...

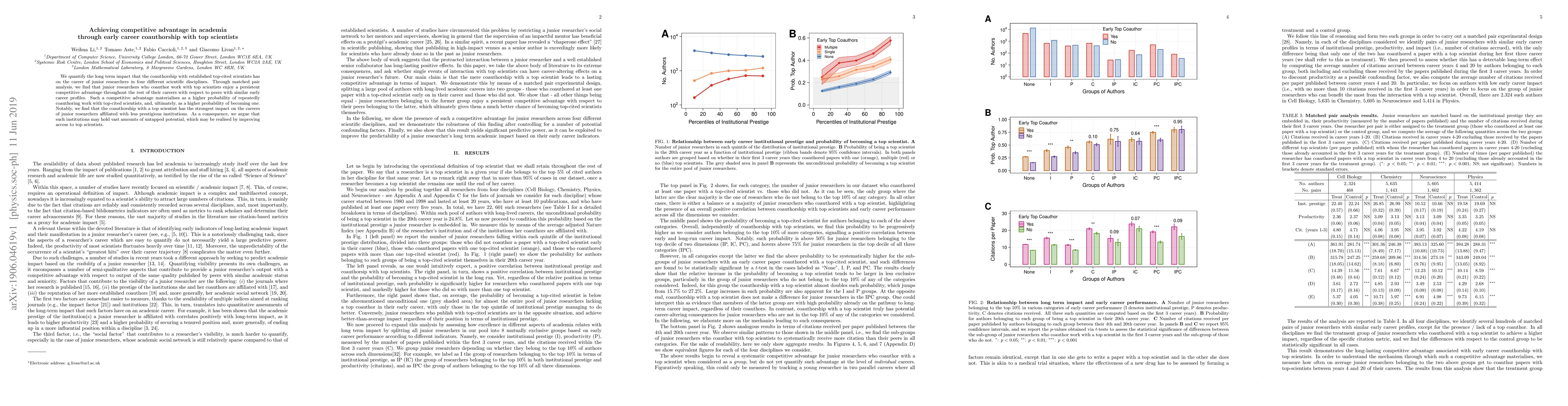

We quantify the long term impact that the coauthorship with established top-cited scientists has on the career of junior researchers in four different scientific disciplines. Through matched pair an...

We propose a topological learning algorithm for the estimation of the conditional dependency structure of large sets of random variables from sparse and noisy data. The algorithm, named Maximally Fi...

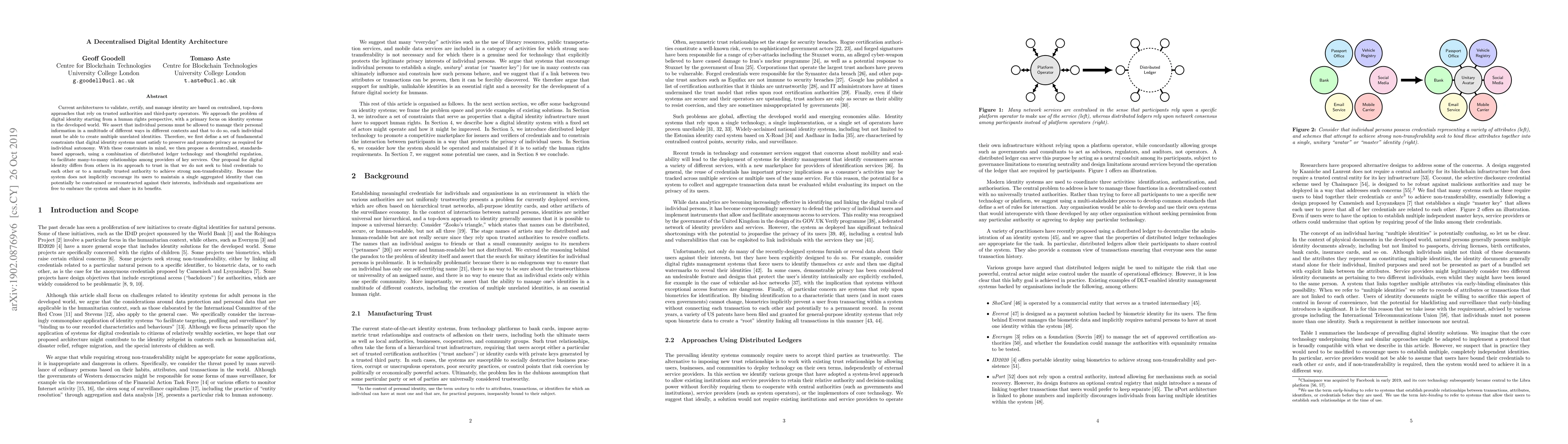

Current architectures to validate, certify, and manage identity are based on centralised, top-down approaches that rely on trusted authorities and third-party operators. We approach the problem of d...

We demonstrate that future market correlation structure can be predicted with high out-of-sample accuracy using a multiplex network approach that combines information from social media and financial...

Cryptocurrencies offer an alternative to traditional methods of electronic value exchange, promising anonymous, cash-like electronic transfers, but in practice they fall short for several key reason...

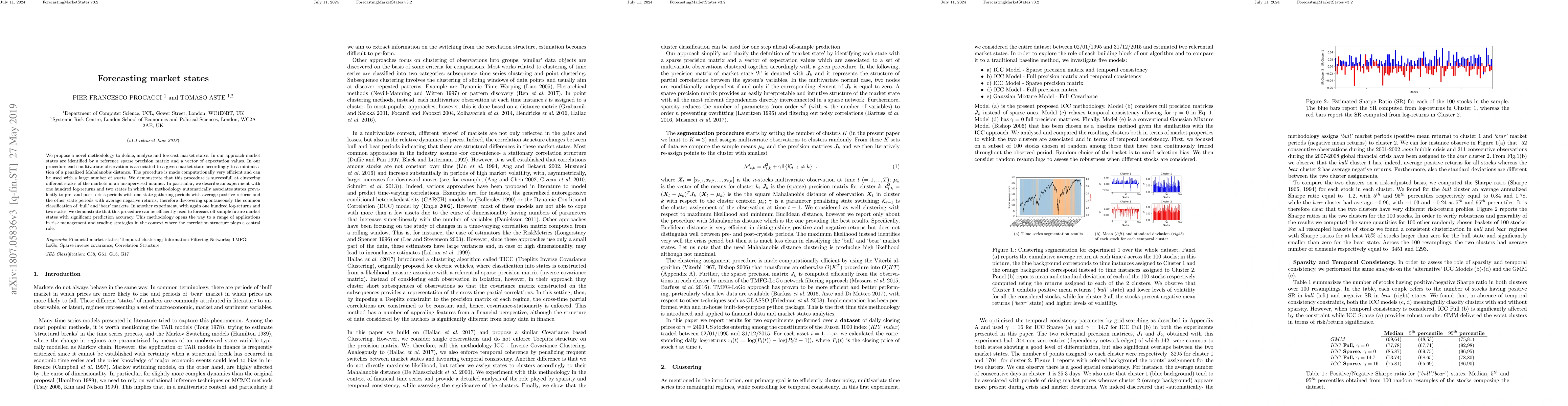

We propose a novel methodology to define, analyze and forecast market states. In our approach market states are identified by a reference sparse precision matrix and a vector of expectation values. ...

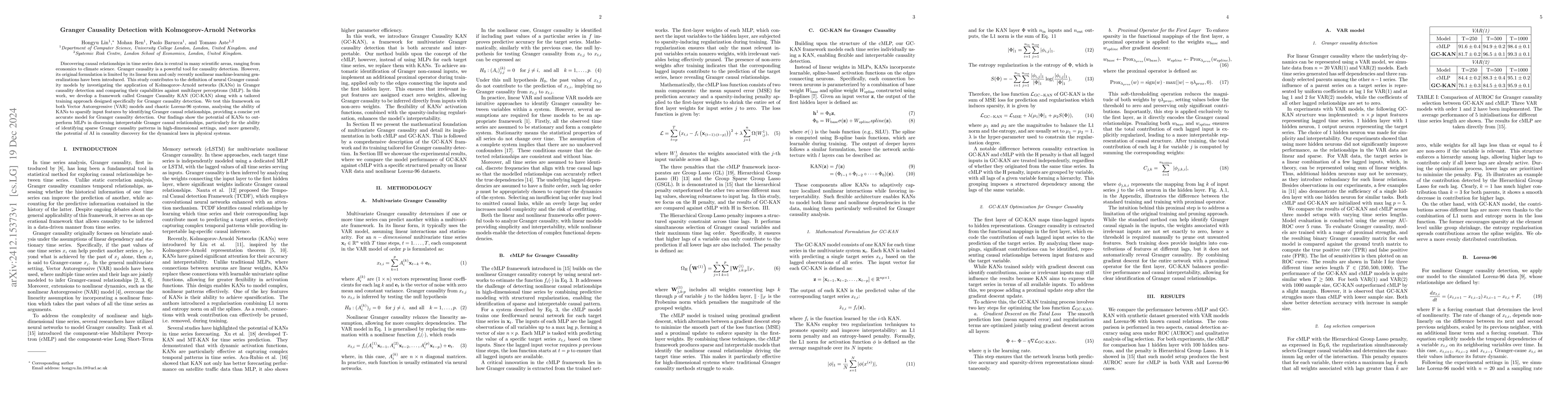

Discovering causal relationships in time series data is central in many scientific areas, ranging from economics to climate science. Granger causality is a powerful tool for causality detection. Howev...

Information Filtering Networks (IFNs) provide a powerful framework for modeling complex systems through globally sparse yet locally dense and interpretable structures that capture multivariate depende...

This paper investigates the evolving link between cryptocurrency and equity markets in the context of the recent wave of corporate Bitcoin (BTC) treasury strategies. We assemble a dataset of 39 public...

High-dimensional data often exhibit dependencies among variables that violate the isotropic-noise assumption under which principal component analysis (PCA) is optimal. For cases where the noise is not...

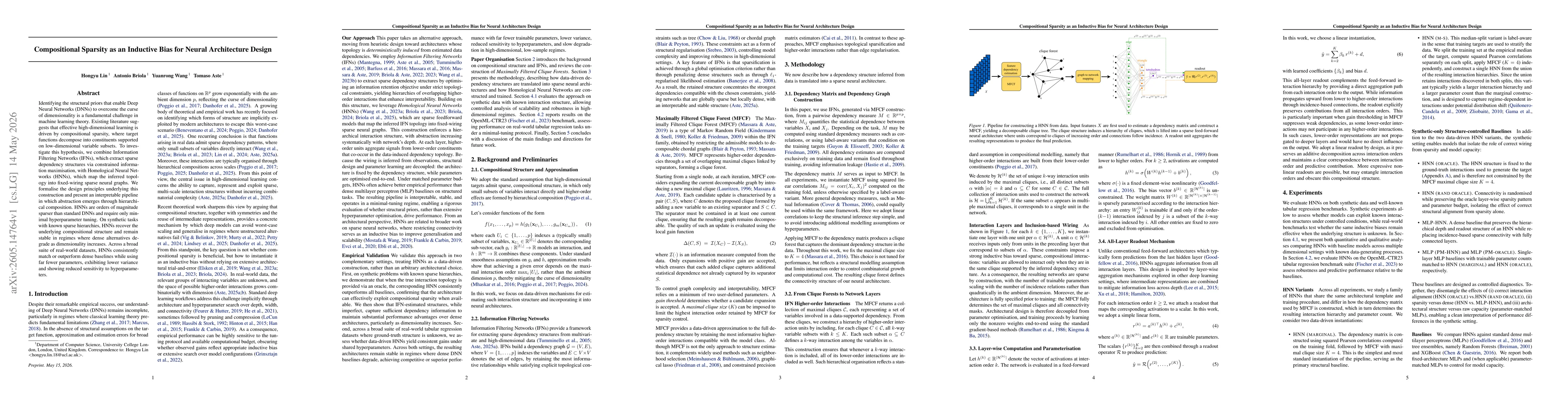

Identifying the structural priors that enable Deep Neural Networks (DNNs) to overcome the curse of dimensionality is a fundamental challenge in machine learning theory. Existing literature suggests th...