Risk-Aware Multi-Armed Bandit Problem with Application to Portfolio Selection

Publication

Metrics

AI Quick Summary

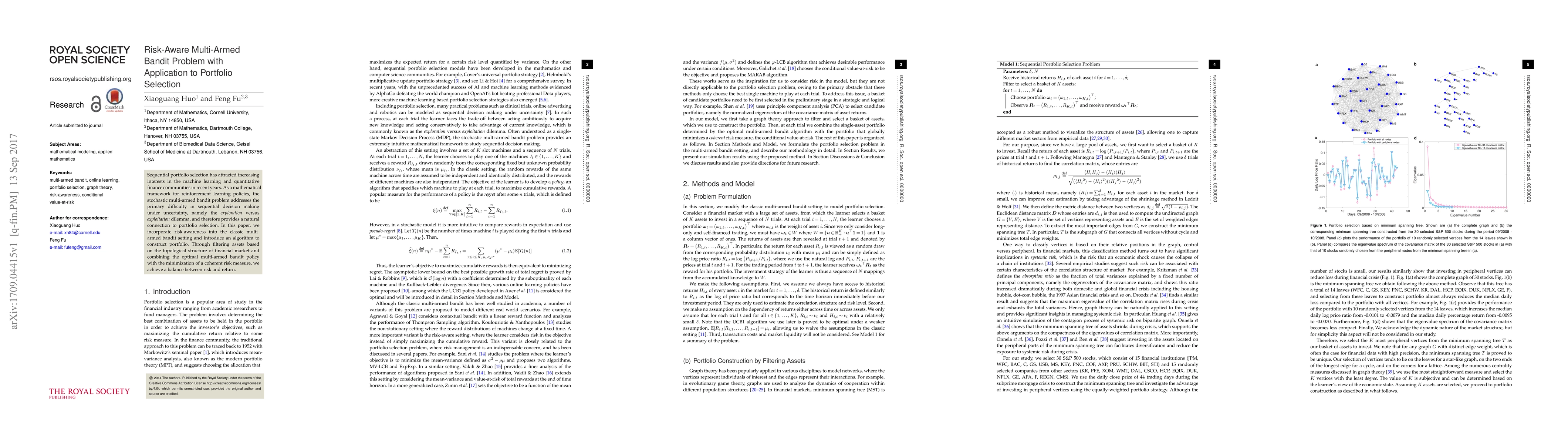

This paper proposes a risk-aware multi-armed bandit algorithm for portfolio selection, addressing the exploration-exploitation dilemma in sequential decision making. It integrates financial market topology and coherent risk minimization to achieve a balance between risk and return.

Paper Preview

Abstract

Sequential portfolio selection has attracted increasing interests in the machine learning and quantitative finance communities in recent years. As a mathematical framework for reinforcement learning policies, the stochastic multi-armed bandit problem addresses the primary difficulty in sequential decision making under uncertainty, namely the exploration versus exploitation dilemma, and therefore provides a natural connection to portfolio selection. In this paper, we incorporate risk-awareness into the classic multi-armed bandit setting and introduce an algorithm to construct portfolio. Through filtering assets based on the topological structure of financial market and combining the optimal multi-armed bandit policy with the minimization of a coherent risk measure, we achieve a balance between risk and return.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0