Robust Faber--Schauder approximation based on discrete observations of an antiderivative

Publication

Metrics

AI Quick Summary

This paper reconstructs Faber-Schauder coefficients of a continuous function from discrete observations of its antiderivative using piecewise quadratic spline interpolation. It reveals that instabilities in the estimation are confined to the final-generation coefficients, which are non-local and sensitive to initial values, while other coefficients are locally data-dependent and uniformly bounded.

Paper Preview

Abstract

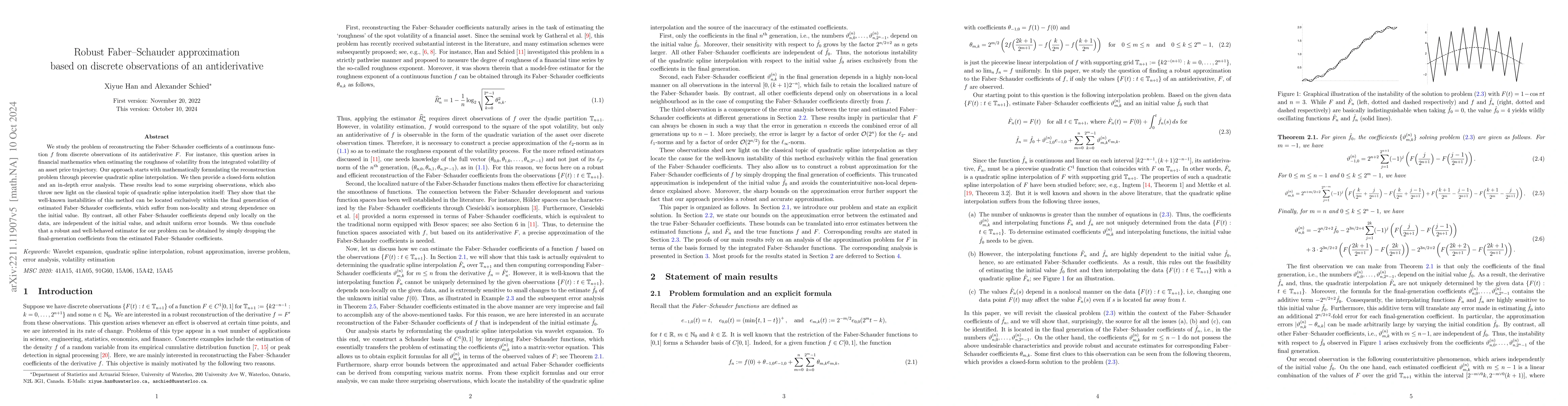

We study the problem of reconstructing the Faber--Schauder coefficients of a continuous function $f$ from discrete observations of its antiderivative $F$. Our approach starts with formulating this problem through piecewise quadratic spline interpolation. We then provide a closed-form solution and an in-depth error analysis. These results lead to some surprising observations, which also throw new light on the classical topic of quadratic spline interpolation itself: They show that the well-known instabilities of this method can be located exclusively within the final generation of estimated Faber--Schauder coefficients, which suffer from non-locality and strong dependence on the initial value and the given data. By contrast, all other Faber--Schauder coefficients depend only locally on the data, are independent of the initial value, and admit uniform error bounds. We thus conclude that a robust and well-behaved estimator for our problem can be obtained by simply dropping the final-generation coefficients from the estimated Faber--Schauder coefficients.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0