Academic Profile

Statistics

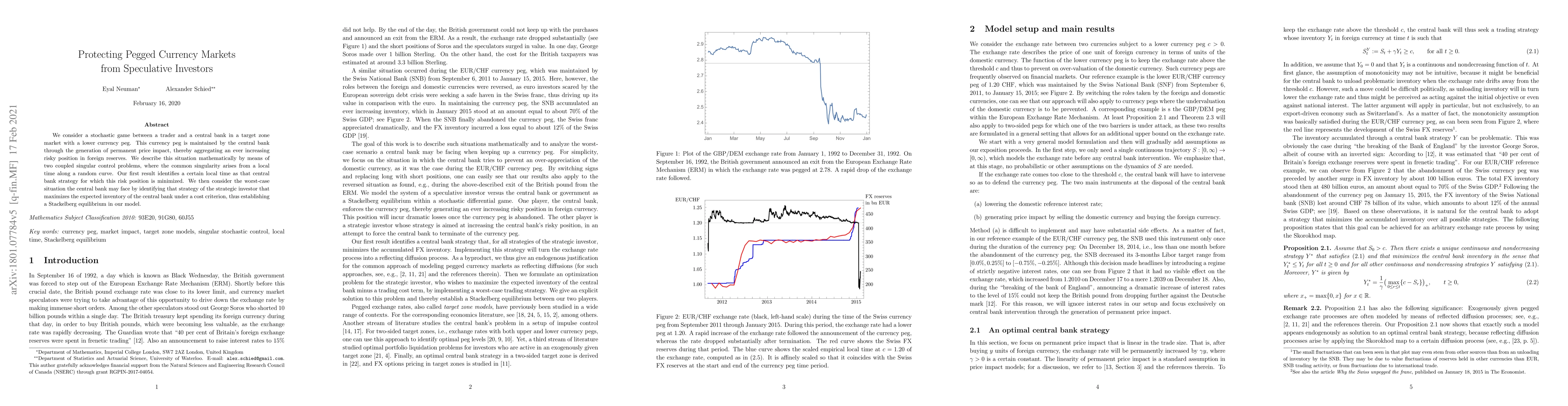

Similar Authors

Papers on arXiv

We construct rich vector spaces of continuous functions with prescribed curved or linear pathwise quadratic variations. We also construct a class of functions whose quadratic variation may depend in...

The present paper studies a kind of robust optimization problems with constraint. The problem is formulated through Backward Stochastic Differential Equations (BSDEs) with quadratic generators. A ne...

We introduce a new class of stochastic processes called fractional Wiener-Weierstrass bridges. They arise by applying the convolution from the construction of the classical, fractal Weierstrass func...

The classical multi-armed bandit (MAB) problem involves a learner and a collection of K independent arms, each with its own ex ante unknown independent reward distribution. At each one of a finite n...

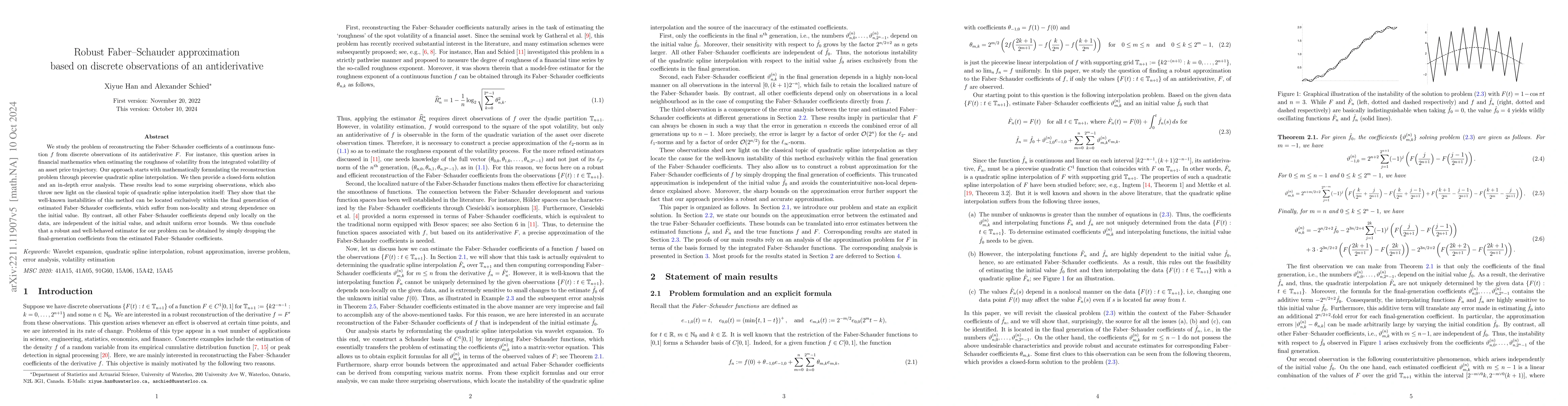

We study the problem of reconstructing the Faber--Schauder coefficients of a continuous function $f$ from discrete observations of its antiderivative $F$. Our approach starts with formulating this p...

Motivated by pathwise stochastic calculus, we say that a continuous real-valued function $x$ admits the roughness exponent $R$ if the $p^{\text{th}}$ variation of $x$ converges to zero if $p>1/R$ an...

We consider Weierstra\ss\ and Takagi-van der Waerden functions with critical degree of roughness. In this case, the functions have vanishing $p^{\text{th}}$ variation for all $p>1$ but are also nowh...

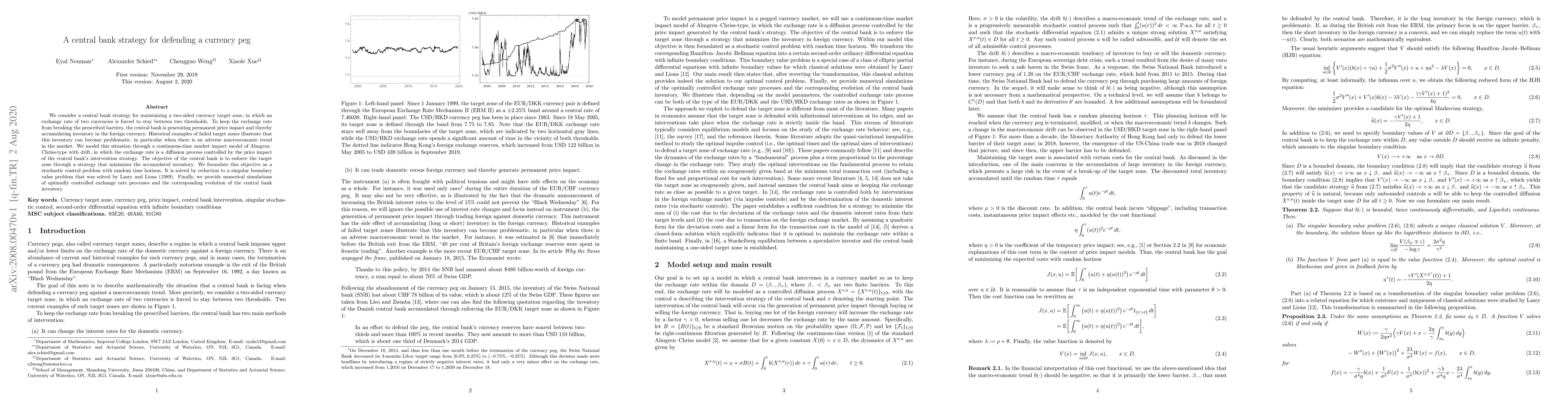

We consider a central bank strategy for maintaining a two-sided currency target zone, in which an exchange rate of two currencies is forced to stay between two thresholds. To keep the exchange rate ...

We analyze a market impact game between $n$ risk averse agents who compete for liquidity in a market impact model with permanent price impact and additional slippage. Most market parameters, includi...

The concept of the $p^{\text{th}}$ variation of a continuous function $f$ along a refining sequence of partitions is the key to a pathwise It\^o integration theory with integrator $f$. Here, we anal...

We study issues of robustness in the context of Quantitative Risk Management and Optimization. We develop a general methodology for determining whether a given risk measurement related optimization ...

We consider a stochastic game between a trader and a central bank in a target zone market with a lower currency peg. This currency peg is maintained by the central bank through the generation of per...

Fractional Wiener--Weierstrass bridges are a class of Gaussian processes that arise from replacing the trigonometric function in the construction of classical Weierstrass functions by a fractional Bro...

We provide a simple and straightforward approach to a continuous-time version of Cover's universal portfolio strategies within the model-free context of F\"ollmer's pathwise It\^o calculus. We establi...

In [8], easily computable scale-invariant estimator $\widehat{\mathscr{R}}^s_n$ was constructed to estimate the Hurst parameter of the drifted fractional Brownian motion $X$ from its antiderivative. T...

In this paper, we investigate the Lambda Value-at-Risk ($Λ$VaR) under ambiguity, where the ambiguity is represented by a family of probability measures. We establish that for increasing Lambda functio...

In continuous-time portfolio selection for non-concave utility functions, the martingale duality approach is widely adopted in complete markets, while the dynamic programming approach may sometimes le...

Fractional Wiener--Weierstrass bridges are a class of Gaussian processes obtained by replacing trigonometric functions in the construction of classical Weierstrass functions by fractional Brownian bri...