01

MethodologyHow they did it

Brief description of the research methodology used

This paper explores pricing-hedging duality for American options in discrete time financial markets, demonstrating that by dynamically extending the market to include all assets, duality can be recovered even when it fails in the original formulation. The authors show that this duality holds in robust frameworks, specifically in the setups of Bouchard and Nutz (2015) and Beiglböck et al. (2013).

This paper explores pricing-hedging duality for American options in discrete time financial markets, demonstrating that by dynamically extending the market to include all assets, duality can be recovered even when it fails in the original formulation. The authors show that this duality holds in robust frameworks, specifically in the setups of Bouchard and Nutz (2015) and Beiglböck et al. (2013).

Brief description of the research methodology used More in Methodology →

Main finding 1 — Main finding 2 More in Key Results →

Why this research is important and its potential impact More in Significance →

Limitation 1 — Limitation 2 More in Limitations →

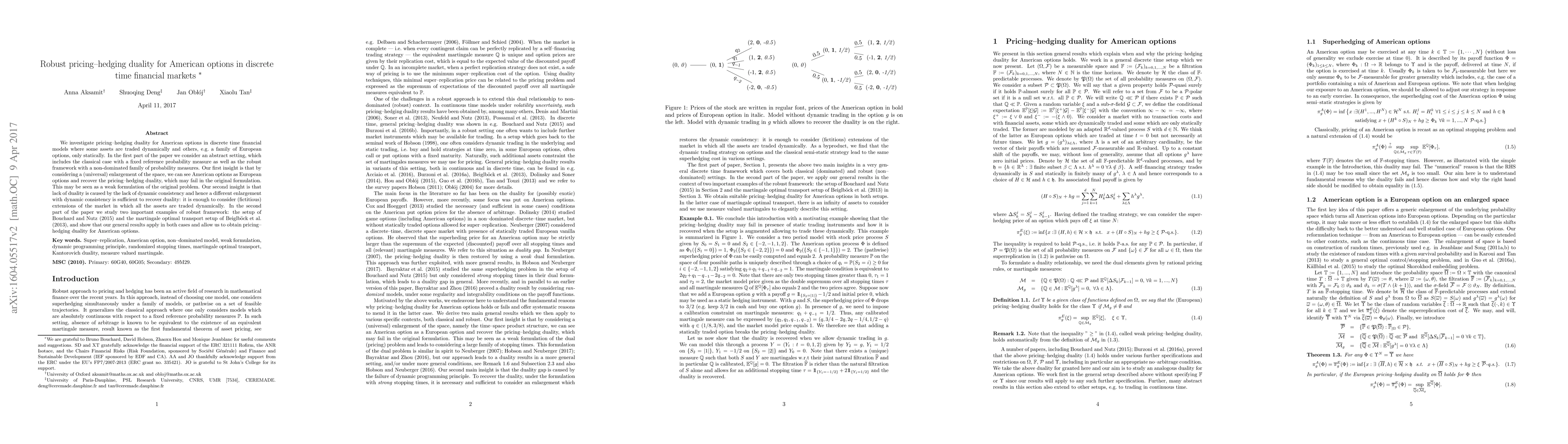

We investigate pricing-hedging duality for American options in discrete time financial models where some assets are traded dynamically and others, e.g. a family of European options, only statically. In the first part of the paper we consider an abstract setting, which includes the classical case with a fixed reference probability measure as well as the robust framework with a non-dominated family of probability measures. Our first insight is that by considering a (universal) enlargement of the space, we can see American options as European options and recover the pricing-hedging duality, which may fail in the original formulation. This may be seen as a weak formulation of the original problem. Our second insight is that lack of duality is caused by the lack of dynamic consistency and hence a different enlargement with dynamic consistency is sufficient to recover duality: it is enough to consider (fictitious) extensions of the market in which all the assets are traded dynamically. In the second part of the paper we study two important examples of robust framework: the setup of Bouchard and Nutz (2015) and the martingale optimal transport setup of Beiglb\"ock et al. (2013), and show that our general results apply in both cases and allow us to obtain pricing-hedging duality for American options.

Seven facets of this paper, analysed and brought into focus by AI.

Why this research is important and its potential impact

Brief description of the research methodology used

Why this research is important and its potential impact

Main technical or theoretical contribution

What makes this work novel or different from existing research

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0