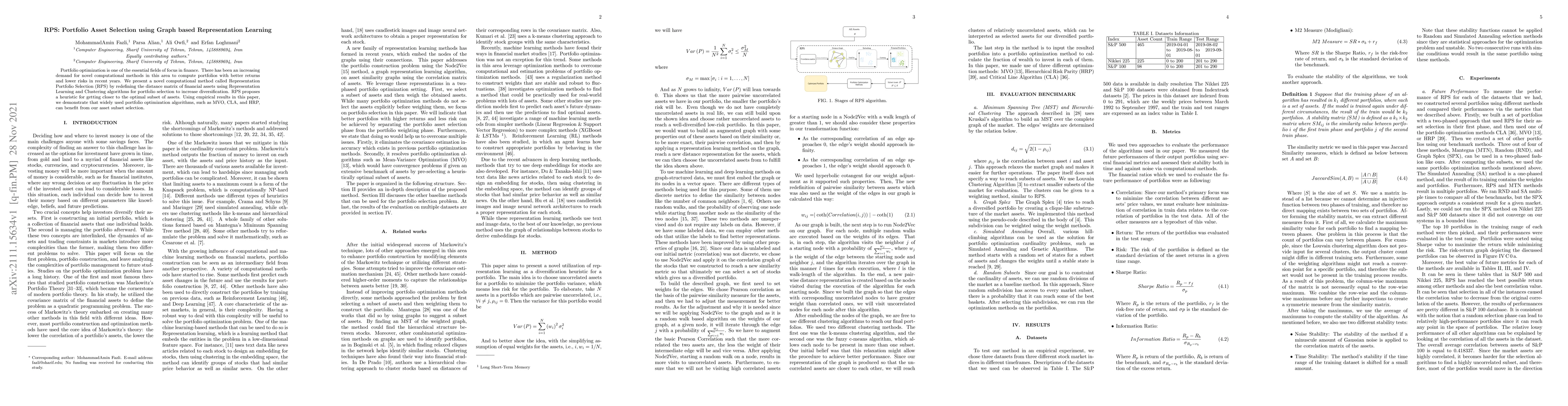

RPS: Portfolio Asset Selection using Graph based Representation Learning

Publication

Metrics

AI Quick Summary

This paper introduces RPS, a novel computational method for portfolio asset selection that leverages graph-based representation learning and clustering to redefine asset distances, enhancing diversification. Empirical results show that traditional optimization algorithms like MVO, CLA, and HRP can improve their performance using RPS's asset subset selection.

Paper Preview

Abstract

Portfolio optimization is one of the essential fields of focus in finance. There has been an increasing demand for novel computational methods in this area to compute portfolios with better returns and lower risks in recent years. We present a novel computational method called Representation Portfolio Selection (RPS) by redefining the distance matrix of financial assets using Representation Learning and Clustering algorithms for portfolio selection to increase diversification. RPS proposes a heuristic for getting closer to the optimal subset of assets. Using empirical results in this paper, we demonstrate that widely used portfolio optimization algorithms, such as MVO, CLA, and HRP, can benefit from our asset subset selection.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0